MNI US Macro Weekly: Payrolls Drives Rates Recalibration

Jul-04 16:24By: Chris Harrison and 1 more...

Federal Reserve+ 2

Download Full Report Here

Executive Summary

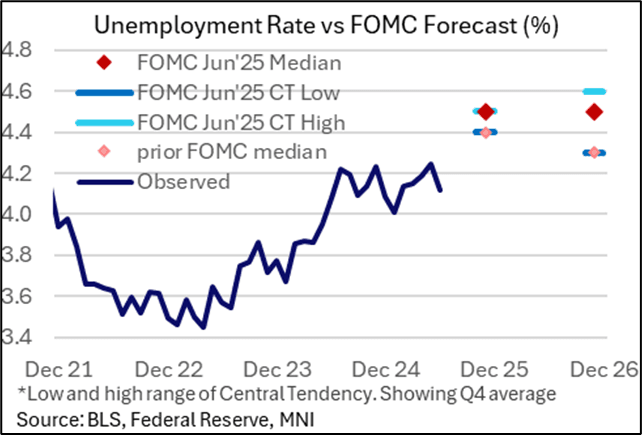

- Nonfarm payrolls growth comfortably beat expectations in June with 147k (cons 106k) along with small upward revisions of +16k. An arguably bigger surprise was the pullback in the unemployment rate, which at 4.12% is the lowest since Jan after 4.24% prior and well below the rounded 4.3% consensus.

- But it was far from an unambiguously strong report. Private payroll gains missed expectations at 74k (cons 100k), leaving government payrolls surging by 73k for the largest increase since Mar 2024, whilst wages and hours worked underwhelmed along with other caveats.

- It followed ADP private employment surprisingly contracting in an escalation of its recent moderation trend, which helped explain the magnitude of the hawkish reaction to NFPs.

- Elsewhere, ISM services didn’t move the needle, almost in line for the headline index whilst prices paid and employment were softer than expected but new orders at least recovered back into expansionary territory.

- In political and fiscal news, President Trump saw his One Big Beautiful Bill approved by both the Senate and then House after reversals from Republican holdouts, meeting his self-imposed deadline of July 4.

- Payrolls saw July Fed cut odds slashed, having built up to almost the most dovish in a month ahead of it. The next cut is back to fully priced for October and with two rather than two and a half cuts priced for 2H25.

- Payrolls landing on Thursday before Independence Day on Friday has limited Fed reaction to the report.

- FOMC minutes headline the regular calendar next week, potentially of note with a highly divided committee (seven members saw no cuts this year through to two members eyeing three cuts in last month’s SEP).

- Tariffs are also back in focus for markets with the 90-day reciprocal tariff deadline set to expire with July 9. Although US officials signalled that a record number of trade deals would be signed between April 8 and now, at the time of writing only agreements with the UK, Indonesia, Vietnam and China have been announced - all with differing degrees of comprehensiveness. Trump has announced that a series of letters will be sent out to trading partners (10-12 on Friday, more in the coming days) detailing what tariff rates will be imposed on imports, with countries starting to pay levies on August 1. Somewhat concerningly, the President has said that these rates will "range in value from maybe 60 or 70% tariffs to 10 and 20%".