MNI US Macro Weekly: Not A Bad Economy

Sep-19 19:21By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download Full Report Here

[This is a two-week edition of the US Macro Weekly, capturing the FOMC decision as well CPI, PPI and retail sales reports ahead of next week’s August PCE release]

- The Fed restarted its easing cycle with a “risk management cut” at its September meeting, cutting 25bp to a range of 4.00-4.25%. That was expected, but the lack of conviction on the FOMC about the rate path forward was a key theme of the meeting’s release materials, as well as Chair Powell’s press conference.

- Despite a lower rate path signalled in the new Dot Plot including a further 2 cuts this year, a seeming lack of clarity on delivering those future rate cuts saw an early dovish market reaction subsequently reverse.

- From a macro perspective, while the latest Fed statement pointing to increased downside risks to employment and Powell’s comment that he no longer saw the labor market as “solid” conveyed concerns about economic weakness, the FOMC’s latest projections didn’t quite square with that perspective.

- Inflation is seen as a little more stubborn than had been expected in the prior set of projections, with upgrades to growth across the forecast horizon, and the unemployment actually seen steady/lower than had been previously expected. As Powell put it, “it's not a bad economy or anything like that.”

- Post-meeting FOMC speakers Miran, Kashkari and Daly all supported a September cut (Miran of course voting for 50bp), each citing potential labor market weakness. Kashkari’s reasoning sounded a lot like Powell’s: “it's not a bad labor market, but it's one that I think we need to pay a lot of attention to”.

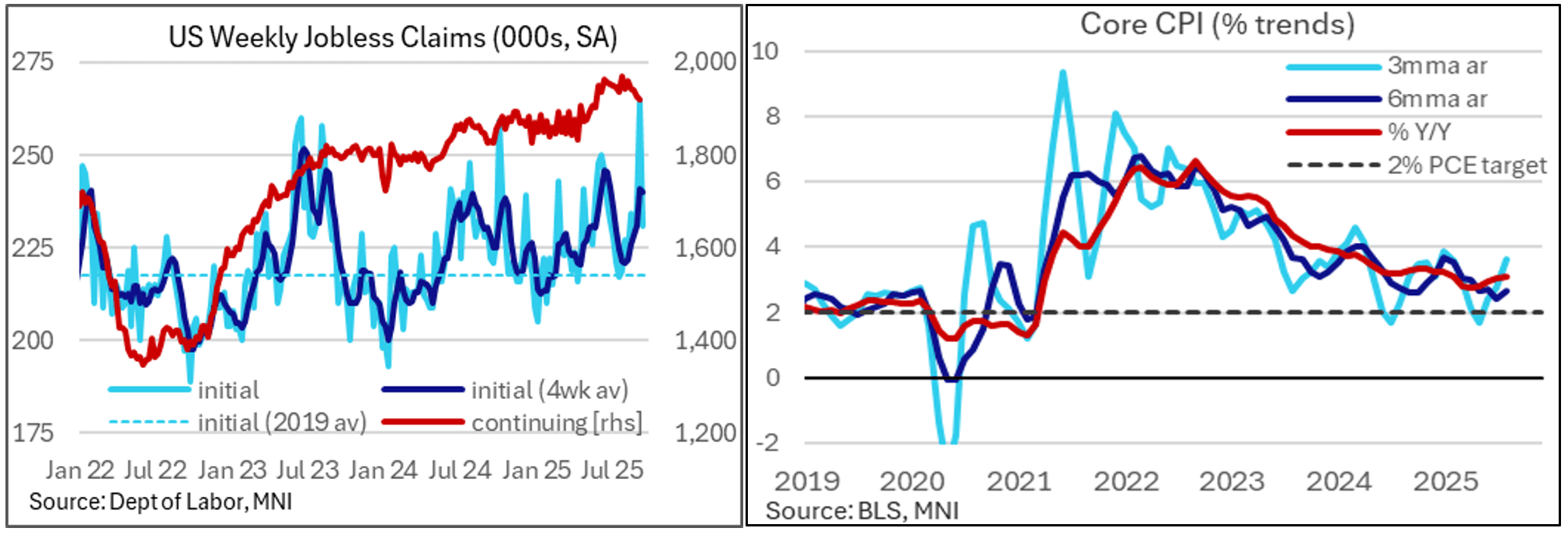

- In data: the downward benchmark revision to payrolls was on the high end of expectations. Jobless claims data fired a warning shot a week ago, although much of the spike in initial was linked to ID fraud in Texas. Latest data then surprised lower, while continuing claims saw a fourth consecutive weekly decline.

- August retail sales beat expectations in all departments, with higher revisions adding to the positive takeaways triggering upgrades to Q3 personal consumption expenditures estimates. Indeed, the Atlanta Fed’s GDPNow is tracking quarterly annualized growth of well over 3%, driven by domestic demand.

- PPI started last week’s inflation releases with a report that relieved concerns about tariff-related price pressures whilst highlighting the volatile and revision-prone nature of the trade services category.

- CPI then followed and was marginally stronger than expected on a M/M basis for both headline and core, with the latter at a robust 0.35% M/M but with a more benign readthrough to core PCE. The MNI median of unrounded analyst estimates for core PCE is 0.21% M/M with potential skew to the upside.

- Data aside, analysts have made dovish changes to their rate views in the wake of the Fed meeting, with the most common change being a more front-loaded easing cycle. Analysts' views for further cuts this year range from zero to 50bp, with the median seeing Oct and Dec cuts aligning with the latest Dot Plot.

- The analyst median has also tipped toward seeing slightly more 2026 cuts: now 75bp (albeit almost an even split between the number seeing 50 and those seeing 75bp), vs 50bp median pre-meeting.

- Next week sees annual updates to national accounts data going back to 1Q20, the August PCE release and heavy post-FOMC Fedspeak.