MNI US Macro Weekly: No Holiday For Tariff Watchers

May-23 20:05By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download Full Report Here

EXECUTIVE SUMMARY

- Market attention on trade matters had appeared to have run its course for the moment, with focus mounting on deteriorating fiscal accounts as Congress made progress on President Trump’s “Big, Beautiful” tax bill.

- But Friday brought a major escalation in trans-Atlantic trade tensions as Trump posted on social media that “I am recommending a straight 50% Tariff on the European Union, starting on June 1”.

- He reiterated that threat in an Oval Office appearance just ahead of the long Memorial Day weekend, leaving just 9 days for Washington and Brussels to reach an agreement.

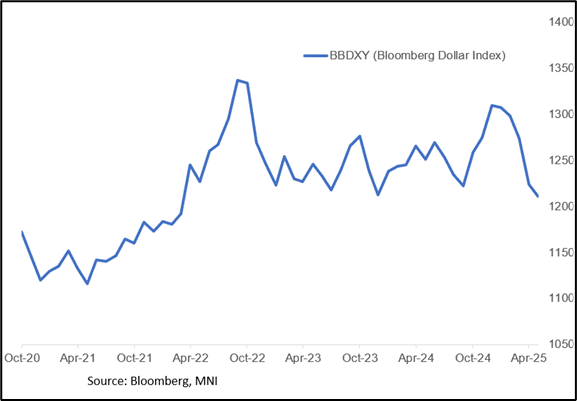

- The most notable reaction in markets was in the US dollar, which fell to its lowest level since 2023.

- On the data side, whilst again looking stale following the latest tariff threat backdrop, firmer than expected flash PMIs were the pick of the week as they better captured the May 12 US-China de-escalation in trade policies compared to previous regional Fed surveys for May.

- That also came with the highest PMI output price inflation for goods & services inflation since Aug 2022.

- Elsewhere, jobless claims extended their trend of a very mild rise whilst home sales data for April were mixed, with existing sales slipping a little further vs new home sales jumping to highs since early 2022.

- Fed speak saw Chicago Fed’s Goolsbee (’25 voter, dove) on Friday describe the EU tariff threat as “really scary” for supply chains whilst reiterating a high bar for rate action amidst uncertainty. Hawks Musalem and Schmid (’25 voters) emphasized a preference for watching hard over soft data.

- After initially spiking lower on Friday’s tariff threats, markets appear to be banking on a deal and are ending the week with end-2025 Fed rates near their most hawkish levels since February. Growth concerns weigh on terminal rate expectations though, at the low end of recent ranges with ~100bp of cuts for the cycle.