MACRO ANALYSIS: MNI US Macro Weekly: Hawkish December Cut Prospects Firm

- We have published and e-mailed to subscribers the MNI US Macro Weekly offering succinct MNI analysis across the range of macro developments over the past week.

- Please find the full report here: https://media.marketnews.com/US_macro_weekly_251128_d27ba2f6b9.pdf

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

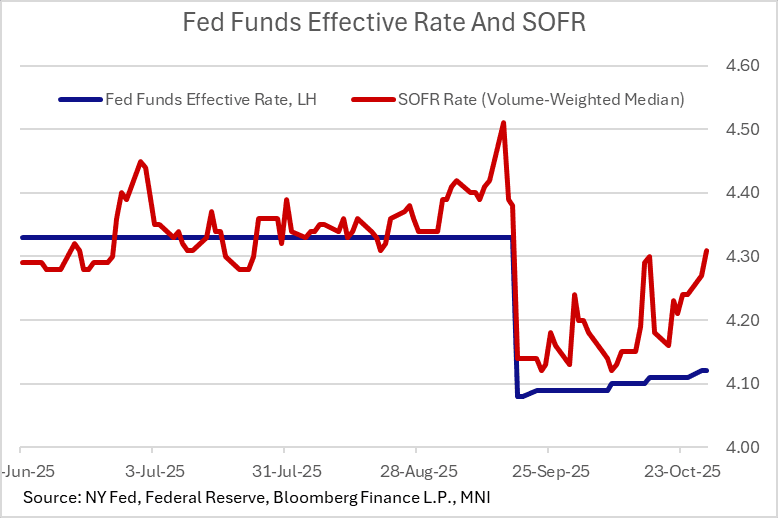

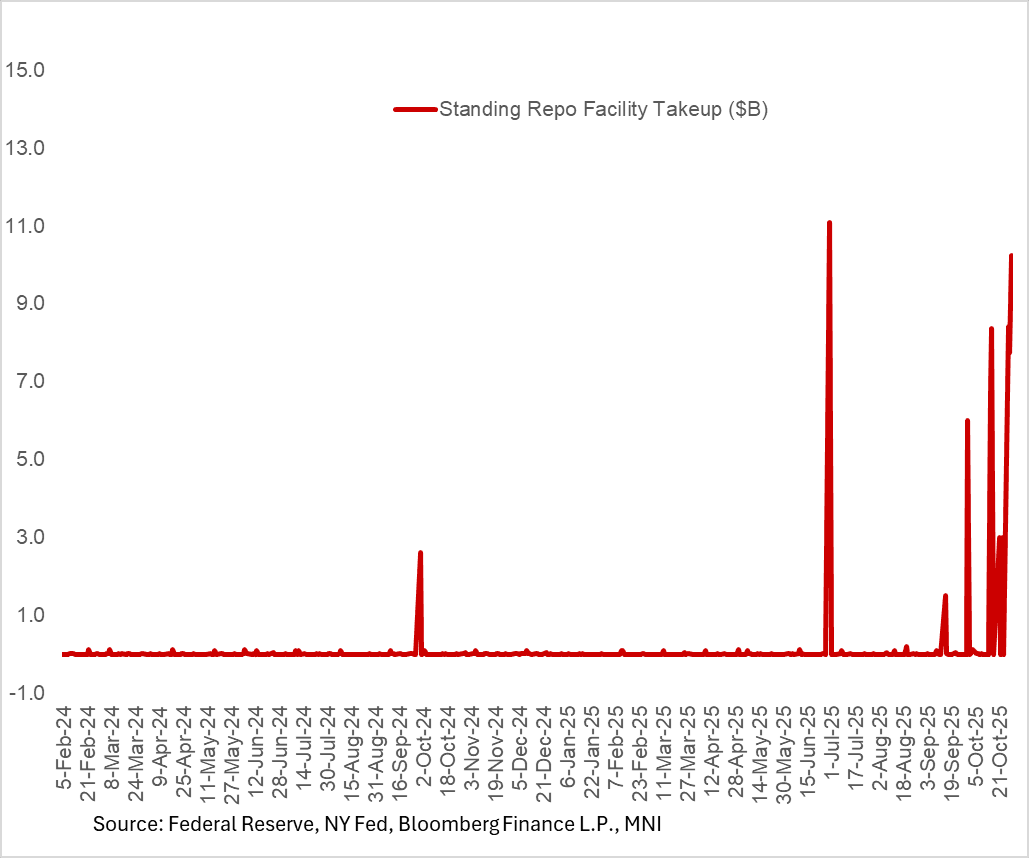

STIR: Effective Fed Funds Steady, But Standing Repo Takeup Rises Again

There was no further upward shift in the effective Fed funds rate Tuesday after Monday's 1bp increase: it printed 4.12%.

- However that comes after 4 increases since the September FOMC meeting (was 4.08%), and Standing Repo Facility takeup rose this morning to a fresh post-June high of $10.2B.

- Both are reminders that funding market pressures were building as the Fed's October decision approached.

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.12%, no change, volume: $92B

* Daily Overnight Bank Funding Rate: 4.12%, 0.01%, volume: $178B

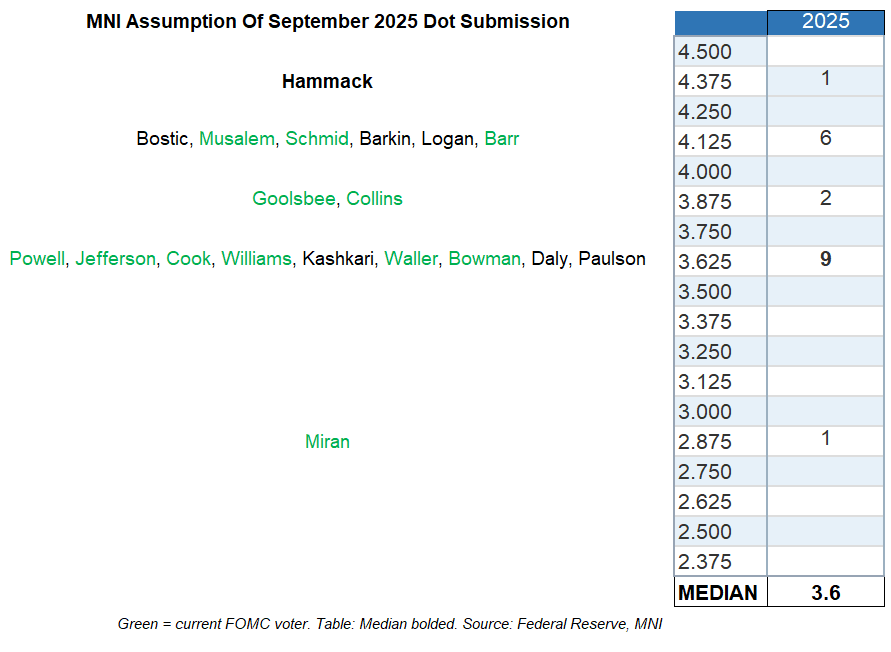

FED: Communications Reforms A Potential Topic Of FOMC Discussion

The Fed has signaled that this fall it would explore changes in the way it communicates policy as part of its framework review. This could be a key topic of conversation at the October FOMC meeting, with a variety of areas under scrutiny. At the very least we expect Chair Powell to be asked about this at the press conference.

- Various FOMC participants have suggested changes including changing the Dot Plot to no longer include the longer-run rate dot, and/or to show rate projections over rolling horizons rather than just for year-end.

- The latest rate policy communications have illustrated the potential utility of rolling horizons, since the September projections are basically a point estimate for Fed moves the remaining 2 meetings of the year).

- Other potential changes include scenario projections and joining-up macro forecasts by participant (instead of potentially disjointed forecasts across different variables).

- While an announcement on conclusions is unlikely at the October meeting, we will be interested in what Powell has to say about it – particularly with the December Dot Plot round looming.

- For what it's worth, here is MNI's assessment of where current FOMC participants placed their end-2025 Funds rate dots as of the September FOMC submission - see our preview for full commentary by all officials since that meeting.

BOC: Canada Bank Analysts Close To Abandoning Future Rate Cut Views Post-BOC

Canadian institutions have all but thrown in the towel on further BOC cuts after today's rate decision. Prior to the October meeting, BMO, Desjardins, and National each saw one further 25bp easing to a 2.00% terminal overnight rate - their post-meeting comments (below) suggest a reconsideration if not outright abandonment. Coming into the meeting, CIBC, RBC, Scotiabank, and TD each had no cuts beyond October as their base case and have retained that view.

- BMO doesn't quite abandon an expectation for further cuts but acknowledges "that’s likely it, for now, for Bank of Canada easing. The Bank appears to believe that the easing to date will offer support; inflation is steadily on its way back to 2%; and the usefulness of monetary policy is somewhat limited in this unique economic environment. That said, we believe that ongoing softness in the job market leaves the door open for some further support, and another 25 bp rate is still on the table for early-2026."

- National concurs: "To us, it’s reasonably likely that the Bank is now done as we share similar outlooks for growth and inflation. At the same time, we still judge economic risks as being skewed to the downside which warrants markets discounting some probability of further easing. Indeed, we wouldn’t close the door on a potential cut at one of the next couple meetings as incoming data—including a couple of jobs reports before December 10th —has the potential to change the outlook. At this point though, it seems a ‘hold’ is the more likely outcome. One naturally wonders how much next week’s federal budget led to the “hawkish cut”. Certainly, looser fiscal policy is supportive of growth and inflation over time, but we don’t expect marginal spending to immediately bring the Canadian economy out of its current malaise."

- Desjardins writes more conclusively: "The bar is high for further monetary policy support. ... We are now of the view that the Bank of Canada will keep interest rates on hold for the foreseeable future."