MNI US Macro Weekly: Growth Sours Before “Liberation Day”

Mar-28 18:37By: Chris Harrison and 1 more...

Federal Reserve+ 4

Download Full Report Here

Executive Summary

- Consumer spending in February unambiguously pointed to signs that declining consumer confidence is feeding through to the hard data.

- This consumer confidence decline has continued in March surveys, with the U.Mich question on government policy’s ability to tackle inflation or unemployment at its joint lowest since 2013. Business surveys have been more mixed though, including the flash services PMI at its highest since December.

- The trade deficit was again larger than expected in February, with the advance release pointing to a three-month deficit running at 5.7% GDP. There were clues of further distortion from monetary gold transfers but we must wait until next week’s full release for a better idea.

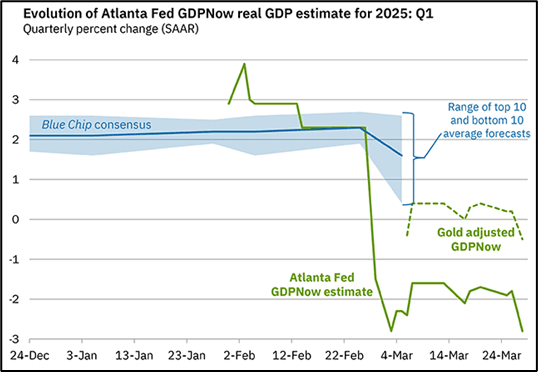

- The combination has seen the latest Atlanta Fed’s GDPNow point to real GDP growth at -2.8% or a gold-adjusted -0.5% for an abrupt slowdown from the 2.45% in Q4 and 3.1% in Q3.

- Detailed national account data suggest that businesses were increasingly uncertain prior to Trump’s inauguration, with net lending in Q4 at its highest since mid-2021 although high profit shares can help offset adverse growth surprises.

- Back to the nearer-term, there are widespread signs of inflationary pressures accelerating. That includes core PCE running at 2.8% Y/Y in February but the three-month at 3.6% annualized (from 2.5% in Jan) and the six-month at 3.1% (from 2.7%) for their highest since Mar and Jun 2024.

- This week’s post-FOMC Fedspeak was characterized by the need for caution amidst inflationary risks.

- Next week can be particularly impactful, with President Trump’s tariff announcements due Apr 2 plus data including ISM surveys before nonfarm payrolls and then Fed Chair Powell rounding the week off.