MNI US Macro Weekly: Fog Acknowledged Ahead Of Data Backlog

Nov-14 18:40By: Chris Harrison and 1 more...

US+ 4

Download Full Report Here

Executive Summary

- The US government has re-opened after its longest shutdown in history.

- There is still nothing concrete on revised data schedules, or certainly not of any note with some Census releases for August the highlight so far at typing. The BLS said Thursday "it may take time" (with Yahoo reporting it could be “in the comings days”) and the BEA and Census Bureau are still working on it more broadly.

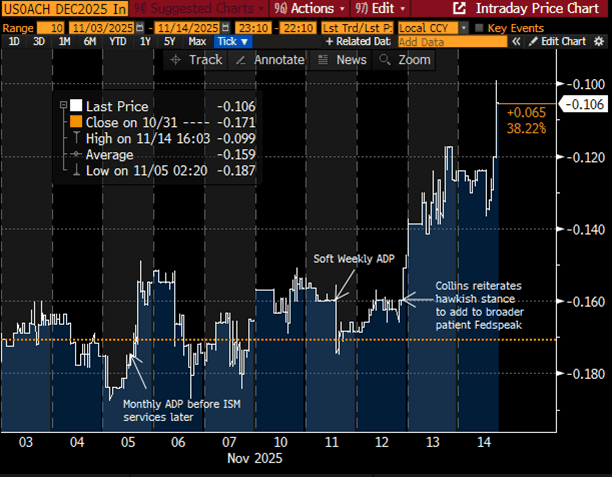

- Indications are that we'll get the September nonfarm payrolls report next week. It also looks unlikely we’ll get the October CPI report whilst NEC’s Hassett implied that the October payrolls report might only see figures from the establishment survey, both of which wouldn’t surprise us.

- This week’s data saw the greatest impact from the weekly ADP series, in its first known-ahead-of-time release in this new weekly format which brought with it some data dissemination issues. At -11k it suggested a return of private sector job losses in data up to Oct 25, on its own pointing to sizeable deterioration in net job creation after some stabilization in the monthly October report but with ADP warning that these data are preliminary and can be revised.

- State-level jobless claims remain steady though, not pointing to any marked deterioration and of note after the sharp increase in job cut announcements in the October Challenger report.

- The Kansas City Fed’s alternative LMCI meanwhile pointed to an unemployment rate nudging up to 4.4% in October, chiming with the 4.36% in the Chicago Fed’s nowcast. Barring any material surprises in the eventually released September BLS report (after 4.32% in August) these indicators could provide useful grounding in lieu of an official October unemployment rate figure.

- Fedspeak meanwhile saw broad support of Fed Chair Powell’s stance from the October FOMC decision when he warned on the need to slow down when driving in the fog. Collins (’25 voter) had the largest impact on STIR markets this week when she confirmed she is not supportive of further rate cuts in the near-term whilst Kashkari (’26 voter) had a marked about turn from a previously more dovish stance.

- Atlanta Fed’s Bostic surprisingly announced he will retire from his position when his term concludes on February 28, 2026. He, and whoever the next Atlanta Fed president is, is a non-FOMC voter in both 2025 and 2026, with the Atlanta Fed next voting in 2027.

- This acknowledgment of growing likelihood of a December pause has seen a large hawkish front-end shift in US rate markets.

- Focus next week will be on any new data scheduling guidelines, the weekly ADP report after notable weakness in the latest release, flash November PMIs and the FOMC Minutes for the degree of expressed opposition to October's rate cut and color on the debate over whether to ease any further.