MNI US Macro Weekly: December Cut Far From A Done Deal

Oct-31 18:46By: Chris Harrison and 1 more...

US+ 5

Download Full Report Here

Executive Summary

- The Fed’s October 29 policy decisions were more or less as expected, with the Fed funds rate range cut by 25bp for a 2nd consecutive meeting to 3.75-4.00%, and an announcement that QT would end imminently.

- However, there was a significant hawkish surprise as Chair Powell began the press conference by highlighting the FOMC’s divisions on the way forward: "in the Committee's discussions at this meeting, there were strongly differing views about how to proceed in December. A further reduction in the policy rate at the December meeting is not a foregone conclusion, far from it. Policy is not on a preset course."

- Friday then saw a hawkish start to post-blackout communications, albeit from the typically more hawkish members which limited the market impact. Hammack and Logan (’26 voters) both would have preferred not to cut this week and Logan will likely find a December cut difficult, Schmid (’25 voter) explained his dissent by seeing an interest cut rate as not supporting the labor market amidst structural factors and Bostic (non-voter) supported the rate cut but was glad that Powell said a Dec cut was “far from” a foregone conclusion.

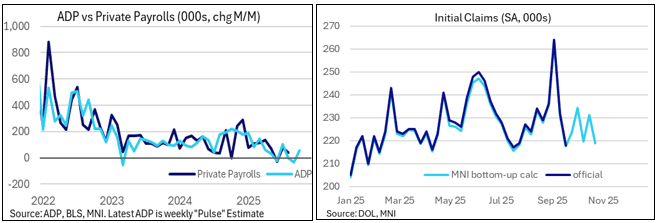

- Turning to data, ADP surprisingly started to publish a weekly series, hinting at a 57k increase in private payrolls over a rough monthly equivalent but with the actual monthly report for October due next week.

- We estimate initial jobless claims fell to a 5-week low of just 219k, a day after Powell drew “some comfort” from claims and vacancies data suggesting “maybe continued gradual cooling, but nothing more than that”.

- Alternative retail sales indicators continue their solid tracking although broader GDP metrics slowed.

- Business sentiment meanwhile improved for manufacturing firms across a variety of indicators but with regional Fed surveys painting a more mixed picture for services firms.

- The Fed rate path has surged higher this week on Powell’s press conference, ending the week with ~14bp of cuts priced for the next meeting in December vs 22.5bp before Powell took to the podium. The SOFR implied terminal yield is at its highest since August although after some notably dovish ranges.

- Looking ahead to next week, data focus will be on the various alternate labor indicators as the government shutdown almost certainly sees a second BLS nonfarm payrolls report not be released (at least for now). Business surveys will also be watched closely, in particular the ISM manufacturing and services.

- We are also set for Fedspeak from members across the FOMC, with possibly notably contrasting messaging expected after Powell’s press conference remarks.