MACRO ANALYSIS: MNI US Macro Weekly: Data Takes Backseat To Fed Chair Intrigue

Our latest US Macro Weekly has been published - Download Full Report Here

- Inflation data this week did little to change market participants’ minds over the future path of Fed rates, taking a backseat to non-economic developments.

- December’s CPI data was softer than expected in most respects, with relatively limited “payback” from the unusually soft (and heavily distorted) October/November report.

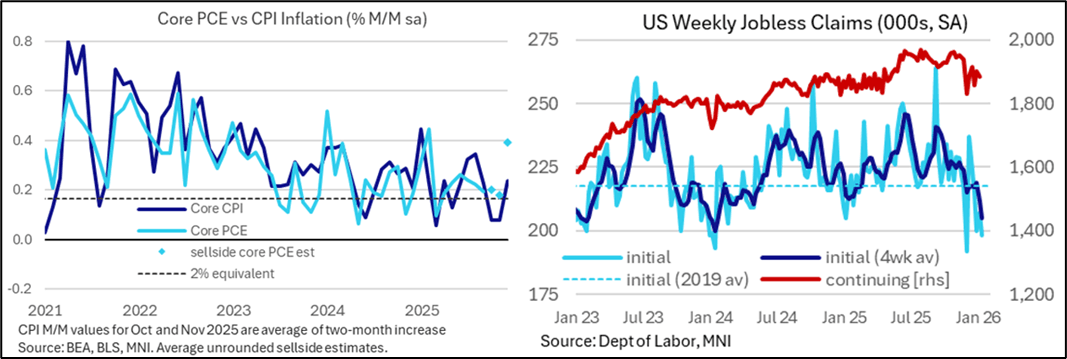

- Subsequently-released (and delayed) producer price data for October and November pushed up core PCE forecasts for Q4 – and there will be a positive spread for core PCE over its CPI counterpart - but the FOMC’s December projection of 3.0% Y/Y still looks to have downside risks.

- Even so, there is overwhelming support among Fed speakers for a rate hold at the upcoming meeting.

- The Fed’s Beige Book for January portrayed a slightly stronger take on economic activity compared with the prior release (November), with a slight improvement in labor market conditions and steady inflationary pressures – likely reinforcing conviction on the FOMC that there is no hurry to cut rates.

- The week’s main moves in rates markets didn’t come from CPI or PPI, but rather a hawkish shift from another surprisingly low jobless claims print before President Trump hinted he’d like Kevin Hassett to stay at the NEC (amid a furore over the DOJ’s just-announced investigation into current chair Powell.)

- Trump is expected to select his candidate for the next Fed Chair soon, and rates jumped alongside the implied probability that former Fed Governor Kevin Warsh will get the nod given speculation that he won't be as ardent a supporter of lower policy rates as Hassett.

- The terminal implied yield of 3.26% has now more clearly exceeded levels seen shortly before the Dec FOMC and last closed higher in July. Increases in 2026 rate expectations are unsurprisingly backloaded with Fed Powell's term expiring in May. The 20bp of cumulative cuts for Jun is little changed since the start of the US session but year-end cuts have been trimmed 3bps to a cumulative 45bp.

- The coming holiday-shortened week (Monday is MLK Day) will be highlighted by legal intrigue on Tuesday and Thursday, with the US Supreme Court potentially releasing its ruling on the legality of the White House's IEEPA tariffs on its next scheduled opinion day on Tuesday, and oral arguments on Wednesday over whether President Trump is allowed to fire Fed Governor Lisa Cook.

- Thursday’s monthly personal income and outlays report headlines the weekly US data calendar with another unusual two-month combined release for October and November.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA: Coming Up In Asia Pac Markets On Thursday

| 2145BST | 0545HKT | 0845AEDT | New Zealand Q3 GDP |

| 2350BST | 0750HKT | 1050AEDT | Japan Weekly Investment Flows |

| 0000BST | 0800HKT | 1100AEDT | Australia Dec Consumer Inflation Expectation |

| 0100BST | 0900HKT | 1200AEDT | China Nov Swift Global Payments CNY |

| 0330BST | 1130HKT | 1430AEDT | Japan 3mth Bill Sale |

Source: Bloomberg Finance L.P./MNI

US OUTLOOK/OPINION: Data Quality Top Of Mind Ahead Of Unusual US CPI Release

- With data quality concerns and data dissemination uncertainty particularly elevated for this week’s CPI release (complicated by the missing October values), it’s important to remember that we’re starting from a poor base for data quality in particular.

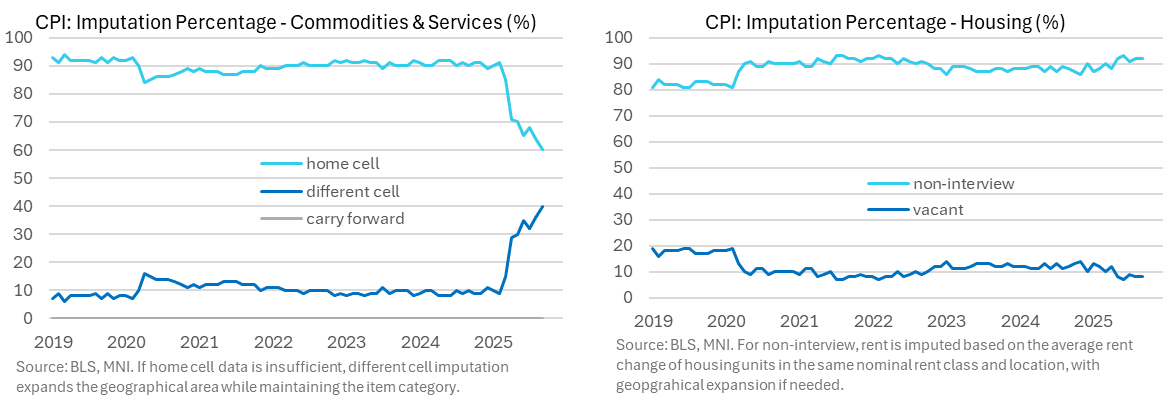

- 40% of the commodities and services price survey source data for the September CPI report was based on a “different cell” rather than its “home cell” in September, a new high after 36% in August. That September CPI report shouldn’t have been affected by the government shutdown, with its collection period coming earlier enough, and it instead extended what had already been a marked increase in different cell imputation since the start of this year reportedly owing in large part to budget and staff cuts.

- A historical average is closer to 10%, although it jumped to circa 30% from April where it then saw a range of 29-36% until August before the latest push higher to 40% in latest data. For context, it peaked at 15% in the pandemic when in-person surveys weren’t possible.

- On top of this, some are concerned that the collection period for this week’s report, covering the second half of November and therefore Black Friday promotions, could have biased some core goods readings lower in particular.

US OUTLOOK/OPINION: Analyst Expectations Of Key Sequential Drivers For Nov CPI

Core Goods Acceleration vs Steady Core Services

Broadly keeping to our usual format, we look at what analysts expect to see for some of the more important M/M categories or those that typically move most month-to-month. Out of necessity we have to compare expectations over two months with September’s M/M figures, even though the BLS won’t be publishing M/M figures. For clarity: where an analyst provided estimates for October and November individually, we have averaged them; where they provided a % total change over 2 months (Nov vs Sep), MNI has divided by 2 for the monthly average. In broad-brush terms, core goods inflation is expected to have firmed since September, helped by used cars, whilst core services inflation should be similar. Note also two expected sizeable contributions, to both upside and downside, from CPI-specific categories that won’t feed through to core PCE and could further distort market reaction.

- Used cars (+ve): We see an average increase of 0.4% M/M for Oct and Nov across six analysts (range -0.2% to 1.0%) after the -0.4% in September.

- Vehicle insurance* (+ve): We see an average increase of 0.1% M/M for Oct and Nov admittedly across just four analysts (range -0.1% to 0.2%) after a surprisingly weak -0.4% in September.

- Rents (+ve): OER and rent inflation is expected to have modestly accelerated after a surprisingly soft September. We see an average increase of 0.23% M/M for Oct for OER (range 0.12-0.30) in Oct and Nov after 0.13% in September, and 0.21% for rents (range 0.08-0.25) after 0.20% in September.

- Airfares* (large -ve): We see an average increase of 0.1% M/M for Oct and Nov across six analysts (range -0.7 to 1.0) after the 2.7% in September beat already high expectations of 2.0%.

- Lodging away from home (-ve): We see an average increase of 0.95% M/M for Oct and Nov across six analysts (range 0.2% to 2.0%) after a surprisingly strong 1.35% M/M in September.

- Apparel (-ve): We see an average increase of 0.5% M/M for Oct and Nov across six analysts (range 0.0% to 1.1%) after a strong 0.7% in September and 0.5% in August. A third consecutive strong month would mark a break from a pattern that has tended to oscillate from month-to-month.

* denotes a PPI-equivalent feeds into core PCE instead, with any surprises likely to be ultimately downplayed

- Non-core: Food (neutral): Seen with an average increase at a ‘low’ 0.3% M/M in Oct and Nov after 0.25% in September. As always, it’s worth watching food away from home within this after it eased to 0.14% M/M in September for its second lowest since early 2021 (an input that feeds into core PCE but not core CPI).

- Energy (-ve): Seen with a small average increase of around 0.3% M/M in Oct and Nov after a solid 1.5% in September.