MNI US Macro Weekly: Board Games

Aug-08 19:10By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download Full Report Here

Executive Summary

- Data took a back seat to Fed leadership developments this week, as President Trump on Thursday nominated CEA Chair Stephen Miran to fill the (temporary) Federal Reserve Board of Governors seat vacated by Adriana Kugler. Earlier that day, Bloomberg reported that Gov Christopher Waller “is emerging as a top candidate” among White House officials to succeed Jerome Powell as Fed Chair next May.

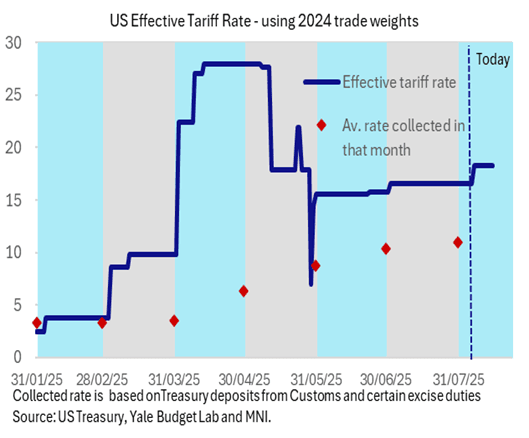

- One area the two have in common is the belief that the current episode of tariff-related inflation will be transitory. And while we are certain that Waller is supportive of near-term rate cuts, given his dissent in July in favor of easing, we and market participants very much assume Miran is as well, despite his relatively upbeat view of economic growth going forward (informed in part no doubt by his current role).

- Even if Miran doesn’t officially get appointed until after the September FOMC, the July payrolls data and revisions and the increasingly dovish composition of Fed leadership have spurred a dovish reconsideration of the near-term rate path, with JPMorgan and ING both bringing forward calls for cuts to resume in September instead their previous view of December.

- While news of Miran’s appointment was met with slightly more Fed easing priced in, on the week it was overall little changed. Although Waller certainly screens as dovish within the current Committee, he is deemed to be less open to Trump’s influence than a fresh appointee would be. Futures markets price 23bp of cuts for September, 38.5bp for Oct and 59bp for Dec.

- Compared with the Fed personnel intrigue, economic data was relatively unexciting, with the week's schedule caught between the July payrolls and CPI releases. The most notable release was ISM Services data coming in more "stagflationary" than anticipated, with a dip in activity amid a pickup in price pressures.

- Latest jobless claims data were relatively stable, while consumer and business credit continued to show evidence of moderation. Unit labor costs pulled back in Q2 alongside an improvement in productivity, though the medium-term trends remained unconvincing from both growth and disinflationary perspectives.

- Overall, measures of broader economic activity (Atlanta Fed's GDPNow, Dallas Fed WEI) continued to point to 2+% growth in Q3, though of course there’s still two months to go in the quarter.

- Tuesday’s CPI report headlines the economic calendar with analysts expecting core inflation to gain momentum in July as the acceleration in core goods inflation continues. We are currently tracking unrounded core CPI estimates at around 0.32% M/M after the 0.23% in June at what would be the strongest M/M print since January. A better idea of latest core PCE implications will have to wait a little longer than usual this month with the July PPI report released on Thursday.

- Friday’s retail sales will also provide an up-to-date look at consumer resilience with Bloomberg consensus currently for a nominal 0.5% M/M in July after the 0.6% M/M in June.