MNI US Macro Weekly: Between A Soft And A Hard Place

May-02 19:09By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download Full Report Here

EXECUTIVE SUMMARY

- As the FOMC heads into its May 6-7 meeting, the economic landscape is no clearer than it was at its previous meeting in mid-March – and in most cases, has become increasingly foggy.

- There have been many developments since then, with plenty of incoming data, an evolution of the outlook, and arguably, a shifting balance of risks. But rather than instigating action on the monetary front, events will have entrenched FOMC participants’ view that patience is the best policy and rates are “well positioned” to allow for nimble reactions to shifts in the data.

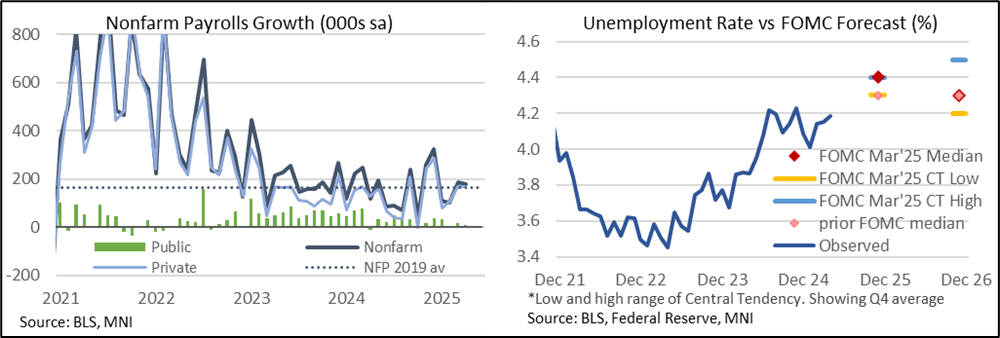

- The dilemma in the current data dependence was well-encapsulated by the latest data this week, including April’s payrolls which were more solid than expected and showed little sign of early tariff disruptions.

- And while Q1 GDP was negative, the Fed may take more signal from solid private demand.

- March's Personal Income and Outlays report showed a strong partly tariff-related pickup in real consumption in March that couldn't offset a weaker quarter as a whole. That said, personal income dynamics were fairly robust at quarter-end, suggesting that despite collapsing sentiment, there is still scope for consumer demand to remain underpinned heading into Q2.

- The changeover from March to April not only provides a neat split between the first and second quarters, but it may also be considered the dividing line between “stale” and more useful, post-tariff data.

- Fed Funds futures lifted sharply off the week’s dovish extremes on a not-as-bad-as feared (but still far from strong) ISM manufacturing report before a continuation of the move on nonfarm payrolls.

- A next Fed cut is now only just fully priced for July (26bp vs 35bp pre-NFP and 43bp pre-ISM mfg) whilst there has been an entire 25bp cut priced out by year-end (76bp vs 91bp pre-NFP and 106bp pre-ISM).

- ISM Services data for April will be of note next week, with a modest deterioration expected (especially given regional Fed services surveys), though perhaps it’s too early for tariff impact to have fed through.

Trending Top

Apr-13 15:35

Apr-13 15:30

Apr-10 20:26