MNI US Inflation Insight: Messy And Misleadingly Soft

Dec-19 20:34By: Tim Cooper and 1 more...

Inflation

Download Full Report Here

EXECUTIVE SUMMARY

- The November CPI report was even messier than had been feared coming into its delayed release, leaving several lingering questions in its wake.

- On the surface, the inflationary pressures from the report appeared much softer than expected.

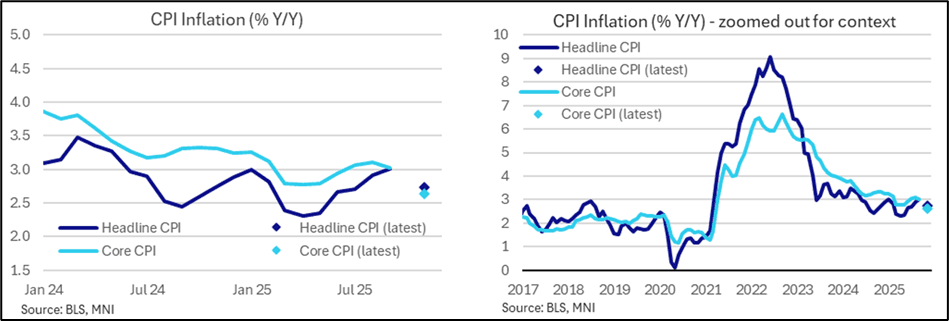

- The two-month change in core CPI (Nov vs Sept; the October release was effectively skipped) came in at 0.159% SA, which roughly speaking translates into an 0.08% M/M average for each of Nov and Oct - well below the 0.24% M/M average expected for those two months (and 0.23% M/M in September).

- The average implied monthly change across Oct and Nov for key core CPI items were softer than expected across the board, most notably for housing.

- Headline CPI came in around 0.10% M/M on average in Oct and Nov (2-month rise was 0.20%). Both food and energy inflation softened on an average M/M pace compared with September though dynamics vs expectations varied.

- But the unusual collection period of late November and methodological choices made by BLS appear to have downwardly biased the readings in the report, and look poised to distort readings for months to come.

- This interpretation appears to be borne out by regional Feds’ extremely soft readings across the relevant underlying metrics which were based on the CPI data.

- Fed Chair Powell had warned this month regarding the latest CPI report that “data was not collected in October and half of November. So, we're going to get data, but we're going to have to look at it carefully and with a somewhat skeptical eye.”

- NY Fed President Williams reinforced this notion in downplaying the signal from the data, confrming that the FOMC will interpret these readings with extreme caution, using the December CPI report due out before the January meeting to make more sense of underlying price dynamics.

- Analysts have sharply downwardly revised expectations for core PCE in October and November (and indeed, Y/Y for several months to come) following the CPI report. All acknowledge that the downside surprise to key aggregates was probably driven by serious methodological issues/choices that may reverse to the upside in the coming months.