MNI US Inflation Insight: CPI Still Solid, But No Bar To Cuts

Oct-27 12:48By: Chris Harrison and 1 more...

Supercore CPI+ 2

Download Full Report Here

- The September CPI report was clearly softer than expected, with core inflation at 0.23% M/M (consensus of 0.32) after 0.35% in August, back to the pace seen in June after two 0.3% readings.

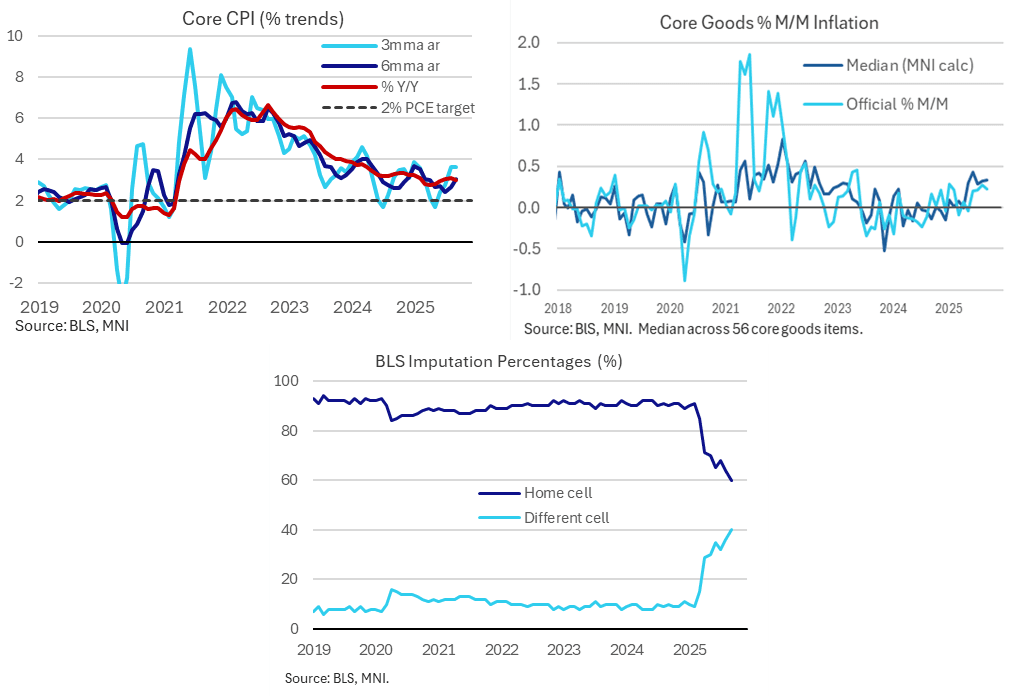

- Core goods were one notable relative weak point with markets still firmly on tariff passthrough watch, increasing 0.22% M/M (consensus 0.34) after 0.28% M/M in August, helped by a surprise decline in used car prices.

- Our look at broad price pressures within the core goods basket suggests September saw a very similar picture to August, with the peak coming back in June rather than seeing any additional acceleration in tariff passthrough.

- Rental inflation was surprisingly soft and included a sizeable reversal of OER inflation after a southern-based spike the prior month. Core services excluding housing were still firm however at 0.35% M/M and are now running at 4.7% annualized over three months or 3.3% over six months, but this metric has poor correlation with its PCE counterpart.

- Core CPI inflation surprisingly eased back a tenth to 3.0% Y/Y after two months at 3.1%, within a 2.8-3.3% range seen since mid-2024. Three-month core CPI stands at 3.6% annualized whilst the six-month is softer at 3.0% annualized.

- Data quality concerns increased again even before government shutdown collection issues, with a new recent high of 40% for different cell imputation in September – this peaked at 15% in the pandemic.

- There is still no release date for the September PPI report, with Fed officials still missing a sizeable piece for core PCE tracking ahead of Wednesday’s FOMC decision.

- Post-CPI, we track core PCE estimates closer to 0.25% M/M for September than the 0.30% estimated pre-CPI. That would see a third month at 2.9% Y/Y but with similar recent run rates rather than ones point to a further acceleration, with the median FOMC forecast eying 3.1% Y/Y for 4Q25.

- The White House has indicated that there won’t be an October CPI report.

- Markets currently fully price 25bp cuts both on Wednesday and then at the next meeting in December before a subsequent cut in March. A June cut is then seen as more likely than not but with less conviction behind it following weekend optimistic headlines concerning US-China trade tensions.