MNI US Employment Insight: Unemp Trends Higher, Caveats Abound

Dec-17 13:06By: Chris Harrison and 1 more...

Employment+ 4

DOWNLOAD FULL REPORT HERE

Executive Summary

- A highly unusual November payrolls report saw multiple caveats that drove a swift fade of an initially dovish reaction.

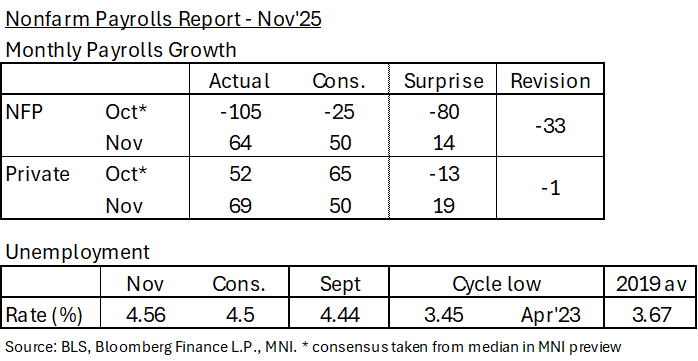

- The two months of nonfarm payrolls growth was a little better than expected for November but much weaker than expected for October, although this was entirely driven by the public sector. Private sector job creation was almost exactly as expected as recent trends actually firmed slightly.

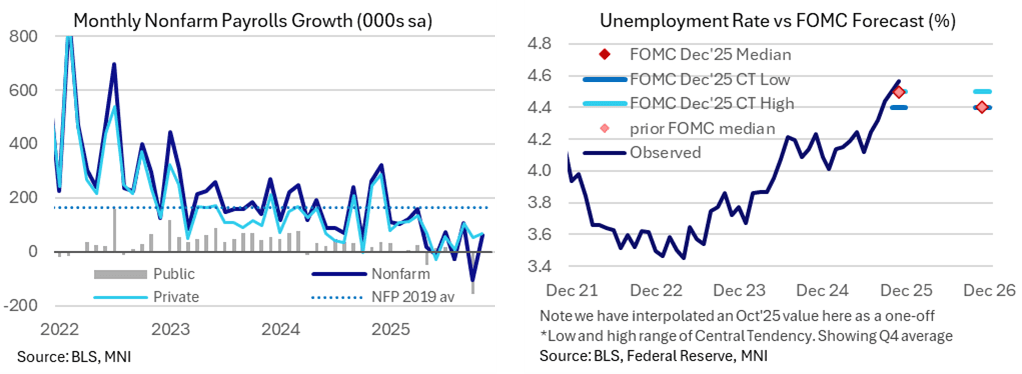

- The household survey for November, with its missing October values clouding recent trends, likely drove the initial reaction with its 4.6% unemployment rate, something that very few analysts forecast (median 4.5% with risks deemed skewed to 4.4%). It did however exaggerate a 4.56% unrounded figure for a 12bp increase, whilst estimates from Goldman Sachs for instance see this as just 2bp ex-government.

- A new historical low for the household survey response rate and higher standard errors, the latter as warned by the BLS and Powell, mean that we can’t put too much weight on these figures. Nevertheless, the existing uptrend looks intact: while the interpolated 0.06pp average monthly increase implies a slower pace of rises vs the preceding three months, this puts the U/E rate on track for an overshoot of the FOMC's 4.5% median expectation for Q4 (something that 7 FOMC members forecast in the December SEP).

- With so many technical caveats to the report, we expect the December payrolls report, back on its original scheduled of Jan 9, to be more impactful ahead of the Jan 28-29 FOMC meeting.

- For now, the next cut is only fully priced for the June meeting under a new Fed chair although there is a cumulative 20bp for the April meeting. A subsequent cut is then broadly fully priced for September.

- Analyst summaries mostly reflect this continued data cloudiness, also putting more weight on the upcoming December NFP report. CIBC do however now expect the Fed to ease twice in 2026, compared to once previously, in Q1 and Q2 with monthly data driving the timing.