MNI US Employment Insight: Sept FOMC In Focus As Jobs Stall

Aug-04 12:39By: Chris Harrison

Employment+ 2

Download Full Report Here

Quick Take: Huge Negative Payroll Revisions Dominate Reaction But U/E Rate Still Roughly Rangebound

- The weak payrolls report dominated what had been a decent-sized hawkish reaction from a patient Fed Chair Powell not giving a nod to a September rate cut at Wednesday’s FOMC press conference.

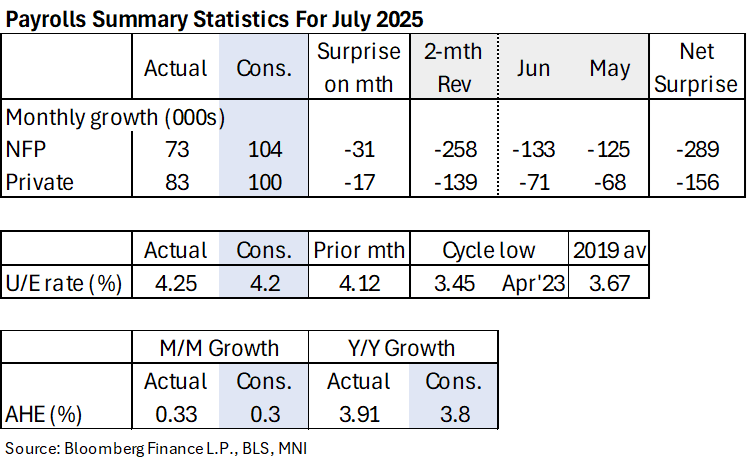

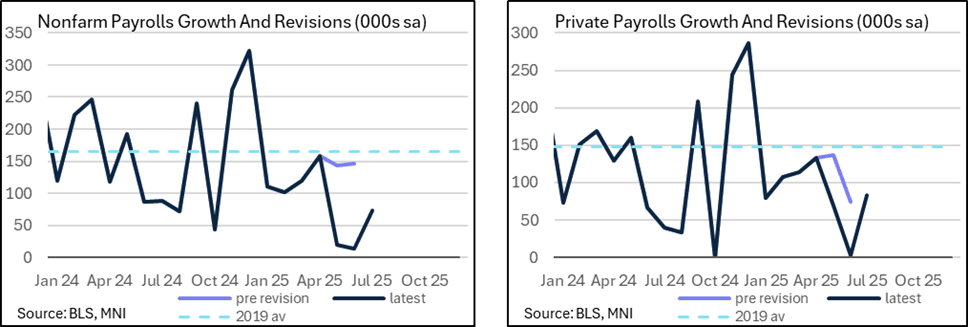

- Nonfarm payrolls growth underwhelmed at 73k in July (cons 104k) but the major headline was the -258k two-month downward revision, of which -139k came from the private sector and -119k from the public sector. Outside of April 2020, that’s the largest two-month downward revision in at least forty-five years.

- We caution however that whilst jobs growth has soured sharply, it’s doing so along with a significant slowing in labor supply under immigration curbs.

- As such, the unemployment rate may have technically ticked up to a new cycle high of 4.248% (exceeding the 4.244% in May) but it continues to roughly plateau in the 4.0-4.25% range seen since last July.

- The median FOMC forecast from the June SEP had the unemployment rate increasing to an average 4.5% in 4Q25 as part of forecast with two rate cuts in 2025 so further deterioration would be expected.

- A note on the latest initial jobless claims data, which are back at 2019 averages, a period when the unemployment rate averaged 3.7%. Other high profile labor indicators were mixed, with ADP stronger than expected and with broad-based sequential improvements whilst the less timely JOLTS report was soft.

- The weak payrolls report prompted an extraordinary response from President Trump, directing his team to fire BLS Commissioner Erika McEntarfer. It’s a broadening out of criticism beyond the Fed’s Powell and its Board. See the MNI Policy Team’s timely look at the outlook for the BLS below.

- First post-FOMC and NFP reaction from FOMC members has been measured.

- Rate cut expectations have surged following the report with a helping hand from a soft ISM manufacturing report also for July. There are now 22bp of cuts priced for the next meeting in September vs 12bp pre-NFP and 61bp to year-end vs 35bp. Analysts are less convinced on Sept cuts at this stage, at least on balance.