MNI US Employment Insight: Payrolls Won’t Sway Foggy Fed Views

Nov-20 20:30By: Tim Cooper and 1 more...

Employment+ 1

Download Full Report Here

Quick Take: Fed Doves Will Point To Unemployment, Hawks To Job Gains

- The long-postponed September Employment Situation report delivered a largely solid if slightly stale snapshot of the US labor market, with an unexpectedly large uptick in the unemployment rate to a 4-year high appearing to outweigh consensus-beating payrolls growth to deliver a slightly dovish market reaction.

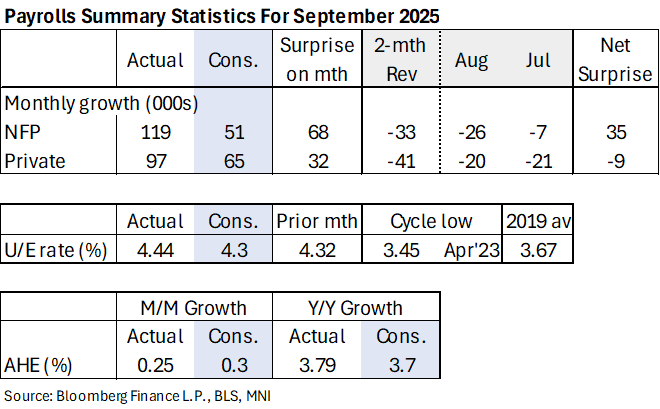

- The payrolls data in the Establishment Survey were stronger than expected, with gains of 119k (cons 51k), following a downward revised August to -4k (22k initially) after 72k in July (from 79k) and -13k in June. This means trend job growth rates are at the lower end of the range of “breakeven” estimates, rather than pushing more materially below, and a very strong response rate to the survey should give more confidence that September’s gains won’t be revised away.

- While private payrolls were on the weaker side when considering downward revisions, we note September saw the first net job creation for private industries outside of health & social assistance since April.

- But to our eye, the Household Survey broadly leaned to a conclusion that the labor market is loosening or at least, not showing material improvement in demand. The 4.44% unemployment rate in September is the highest since October 2021 (4.32% prior) and was above the consensus expectation of 4.3%.

- While it could be argued this represented a "healthy" rise, given that it came with a rise in participation, we didn’t see it as unambiguously so as other metrics continued to point to continued soft labor demand.

- Indeed we don’t think the FOMC’s doves will see much in this report to change their perception of risks to the labor market as a whole, though by the same token the expectation-beating payroll gains will be taken by hawks as evidence that downside has not materialized to a point that warrants further easing just yet.

- With no October or November payrolls data available going into the December 9-10 FOMC, policymakers will have to wade through the data “fog” and ascertain whether the “alternative” measures of labor market health show a trajectory since September that would warrant a further risk-management cut.

- While most such data suggests conditions haven’t improved since September, neither is the bottom falling out of the labor market.

- Post-NFPs, some analysts shifted their views for the December Fed meeting, now seeing a hold whereas they had previously expected a cut, with none that we are aware of doing the converse.

- That was slightly at odds with market-implied prospects for a cut at next month’s meeting which shifted back to 9-10bp vs 6bp beforehand, though larger moves are seen further out the curve.