MNI US CPI Preview: Watching Initial Tariff Passthrough

Apr-09 14:37By: Chris Harrison

Inflation+ 2

Download Full Report Here

Executive Summary

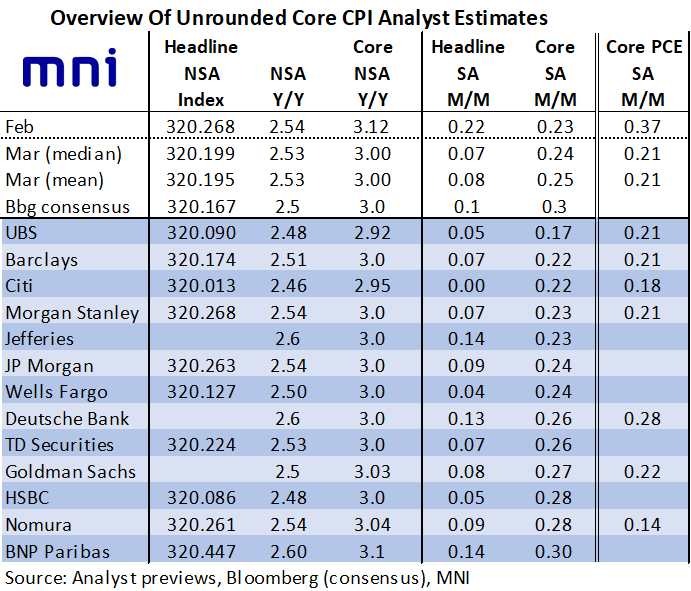

- Analyst unrounded estimates see core CPI inflation little changed in March, at circa 0.25% M/M after 0.23% in February. It implies risk to the downside for rounded consensus of 0.3% M/M.

- The US imposed 20% tariffs on China in early March after 10% in February, offering an early look at passthrough before the latest (total) 104% tariff on China plus large “reciprocal” tariffs elsewhere.

- The core CPI Y/Y is expected to ease a tenth to 3.0% for its lowest since Apr 2021 but recent run rates are likely to have remained hotter, including the six-month rate for a third month running.

- Analysts see some CPI-specific items providing the main upside sequential drivers and indeed tentatively see core PCE moderating to ~0.20% M/M after a robust 0.375% M/M in February.

- Headline CPI meanwhile is seen at a ‘low’ rounded 0.1% M/M, with a large drag from energy.

- We’d look to fade any dovish reaction to a soft reading that specifically sees greater odds of an intermeeting cut considering Powell’s tone last week.

- Beyond that, there could be sensitivity to surprises in either direction, perhaps more so to a hawkish surprise if it’s seen as a prelude to firmer price increases as “Liberation Day” tariffs kick in, forcing the Fed to keep rates on hold for longer at the expense of growth. Ultimately though, continued tariff headlines and prospects around any ‘deals’ will have a greater impact on market pricing.