US INFLATION: MNI US CPI Preview: The Year’s Last ‘Reliable’ CPI Read?

Oct-22 12:27

- We have published and e-mailed to subscribers the MNI US CPI Preview ahead of Friday's release.

- Please find the full report including MNI analysis and views from analysts here: https://media.marketnews.com/USCPI_Prev_Oct2025_f7e5818f86.pdf

Executive Summary

- The delayed September CPI report is due for release on Friday Oct 24 at 0830ET, with the BLS making an exception on social security payments grounds during the government shutdown.

- It’s possibly the last report that won’t be adversely impacted by the shutdown until the new year, although quality concerns were already elevated with high reliance on imputed values back in August.

- We see a median unrounded analyst estimate at 0.40% M/M for headline and 0.30% M/M for core CPI.

- This would mark a marginal sequential acceleration for headline as energy strength offsets a slight moderation in core after a stronger than expected 0.35% M/M in August.

- Monthly core CPI inflation is expected to see firmer goods inflation across a variety of items but softer services, primarily from rents after what’s seen as a temporary upside surprise in August.

- Core CPI inflation is expected to hold at 3.1% Y/Y for a third consecutive month whilst headline CPI firms two tenths to 3.1% Y/Y for its fastest since May 2024 but with chance of rounding to 3.0%.

- Core PCE inflation meanwhile is seen at ~0.30% M/M in September in early analyst estimates, an acceleration from 0.23% in August and 0.24% in July barring potentially wide-ranging revisions. That would see a third month at 2.9% Y/Y, with the median FOMC participant forecasting 3.1% Y/Y for 4Q25.

- There has been no update on potential release date for the September PPI report, likely leaving the Fed with ~65% of inputs for PCE inflation in September ahead of the Oct 28-29 FOMC meeting.

- Markets see a 25bp cut next week as locked in and currently fully price another 25bp cut in December before roughly a quarterly pace thereafter with cuts in March and June.

- The labor market is driving the rate cut profile but broad-based upside surprises in this September report can see this path come into question in the near-term. The median FOMC participant last month eyed two more cuts this year (Oct and Dec) but with a sizeable share looking for a slower pace.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GLOBAL POLITICAL RISK: Week Ahead 22-28 September

Sep-22 12:25

Download Full Report Here

(MNI) London – All timings are subject to change.

Monday 22 September:

- Japan: The formal campaign period for the leadership of the governing Liberal Democratic Party (LDP) got underway, with five candidates on the ballot. Frontrunners to replace outgoing PM Shigeru Ishiba are former Minister of State for Economic Security Sanae Takaichi and Agriculture, Forestry and Fisheries Minister Shinjiro Koizumi.

- United States: While both the Senate and House are on recess for the Jewish New Year, there is the potential for talks this week between Congressional Democrats and Republicans over efforts to avoid a government shutdown on 1 October. Both sides are seen to be digging in, with little sign of whether the GOP will be able to get its ‘clean’ funding bill passed in the Senate or if Democrats' demands on a ‘laundry list’ of demands, such as the permanent extension of subsidies, will be heeded.

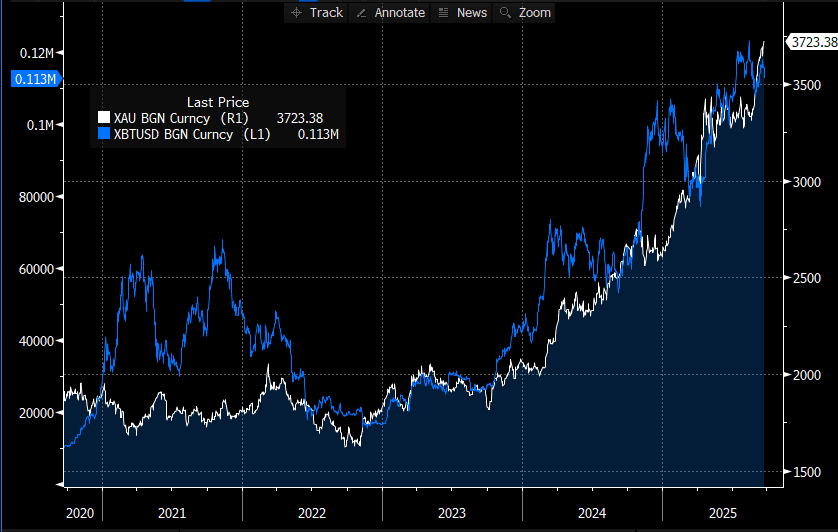

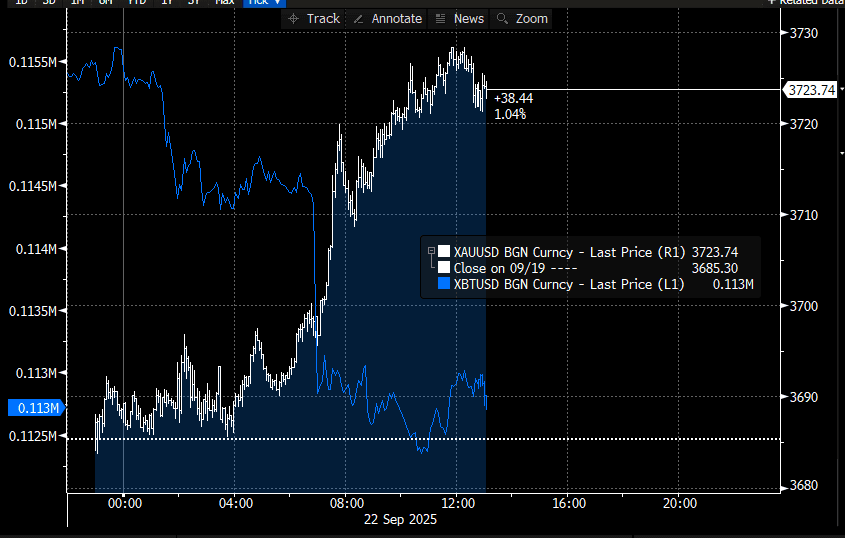

GOLD: /CRYPTO: Fresh ATH For Spot Gold; Potentially Supported By Crypto Weakness

Sep-22 12:21

- Spot gold registered a fresh all-time high of $3,728/oz this morning (currently +1.03% at $3,723). Gold remains in a clear bull cycle, and shallow short-term pullbacks remain corrective.

- The next objective is $3744.2, a Fibonacci projection point, with initial firm support not seen till $3,578 (the 20-day EMA).

- On an intraday basis, it’s not unreasonable to suggest that this morning’s weakness in cryptocurrencies (reportedly spurred by a large liquidations in Ethereum and Bitcoin) drove some rotations into Gold. Over the short-term, crypto and gold can exhibit a negative correlation due to the former’s risk sensitive nature.

- However, over the medium/long-term, the correlation between the likes of bitcoin and gold is positive. Some argue that both assets have can perform as a monetary inflation hedge, and are positively correlated with overall financial system liquidity.

- Bloomberg also reported this morning that "On Friday, bullion-backed ETFs surged 0.9%, the most in percentage terms since 2022", indicating that investor demand for gold following the Fed's rate cut last week remains strong.

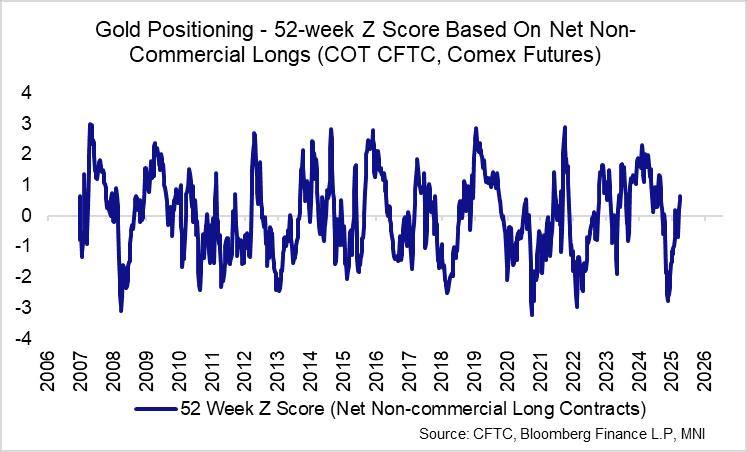

- Gold positioning metrics unsurprisingly continue to advance further into “long” territory according to CFTC COT data as of September 16.

- However, 52-week Z scores of net longs both on an outright and % OI basis still don’t screen as stretched as was seen around last year’s US election.

- Other precious metals are also performing strongly today, with silver up 1.4%, platinum up 0.7% and palladium up over 2%.

Figure 1: Gold and Bitcoin Since 2020

Figure 2: Gold and Bitcoin Intraday

Figure 3: Gold Positioning Metrics

FOREX: EURJPY Consolidating Breach of 174, EZ PMIs and Japan Politics in Focus

Sep-22 12:19

- Last Thursday’s advance for EURJPY resulted in a breach of 173.97 resistance, the Jul 28 high and bull trigger. This confirmed a resumption of the medium-term uptrend and maintains the price sequence of higher highs and higher lows.

- The cross has been oscillating either side of the 174.00 mark to start the week but has been consolidating above the figure across the late European morning. Sights are on 174.86 next, a Fibonacci projection, before the 2024 highs which reside at 175.43, a key medium-term resistance. Support moves up to 173.01, the 20-day EMA.

- Event risk this week will continue to keep EURJPY in focus, starting with tomorrow’s Eurozone flash PMIs. The Eurozone-wide composite PMI has been gradually improving in recent months, but this has largely been a function of a recovery in manufacturing. While welcomed after several years of malaise, the services sector is much more important in terms of total value added. A deterioration in services sentiment (and by extension actual activity) would be one pre-requisite for another ECB rate cut this cycle.

- Separately in Japan, Tokyo CPI is due Friday, while domestic emphasis remains on the high level of political uncertainty ahead of the LDP leadership election on Oct 04. A poll released by the Asahi newspaper revealed that Shinjiro Koizumi remains the most popular candidate, securing 41% of the vote from LDP supporters compared to 24% for Tanae Takaichi. While the Koizumi-Kato team are seen as broadly endorsing a more hawkish BOJ, the JPY may stay under pressure until further clarity is secured.