MNI US CPI Preview: Handle With Care

Dec-16 22:01By: Tim Cooper and 1 more...

US+ 1

Download Full Report Here

Executive Summary

- The latest delayed CPI update from the Bureau of Labor Statistics (Thursday Dec 18, 0830ET) threatens to be messy in several regards, muddying the signal for markets and for monetary policy.

- The government shutdown precluded October data collection, meaning overall CPI aggregates will not be available for the month, and the inflation recorded for November is on a 2-month change basis from Sept.

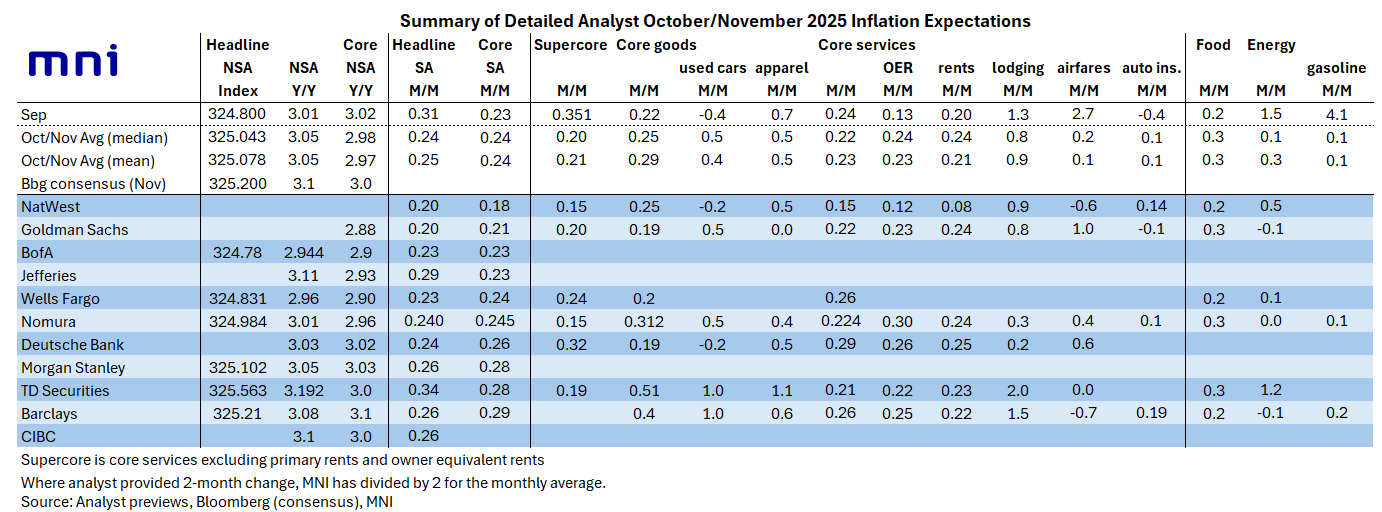

- While the M/M data will never be officially available, MNI's usual aggregation of sell-side analyst expectations points to expectations of an average of 0.24% M/M core CPI monthly across October and November. This would mark a basically steady pace from September's 0.23% M/M.

- The BLS will provide data for a "small" number of subcomponents for October, potentially including several key components of core CPI that could be derived from internet and private data sources, but it's not clear which ones will be published and how this will be presented in the report.

- Consensus is for core goods to accelerate slightly vs September, partly reflecting expected continued tariff passthrough, with an MNI median of 0.25% M/M average for Oct and Nov (Sep: 0.22%).

- Core services prices are conversely expected to moderate very slightly, at an average 0.22% M/M (Sep: 0.24%), with softer travel-related prices seen offsetting a pickup in rents/OER (leaving Supercore softer).

- On top of this, data quality concerns had been deteriorating even prior to the shutdown, and some are concerned that the collection period for this report could downwardly bias November core goods CPI.

- We already have a sense of how markets may react erratically to a disjointed report: the delayed nonfarm payrolls release for November (which like CPI, also saw partial data for October) out Tuesday saw an initial dovish reaction on an elevated unemployment rate but with many complexities within the report, and some clear caveats, limiting the reaction.

- Fed rate pricing comes into the release showing the next cut only fully priced for the June meeting. We suspect the December CPI report will be more pivotal, with the BLS prioritizing its production and getting back to its original release schedule for Jan 13.

Trending Top

Mar-27 20:13