MNI US CPI Preview: Data To Shape Fed's Tone On Rate Cuts

Sep-09 20:41By: Tim Cooper and 1 more...

Inflation

Download Full Report Here

Executive Summary

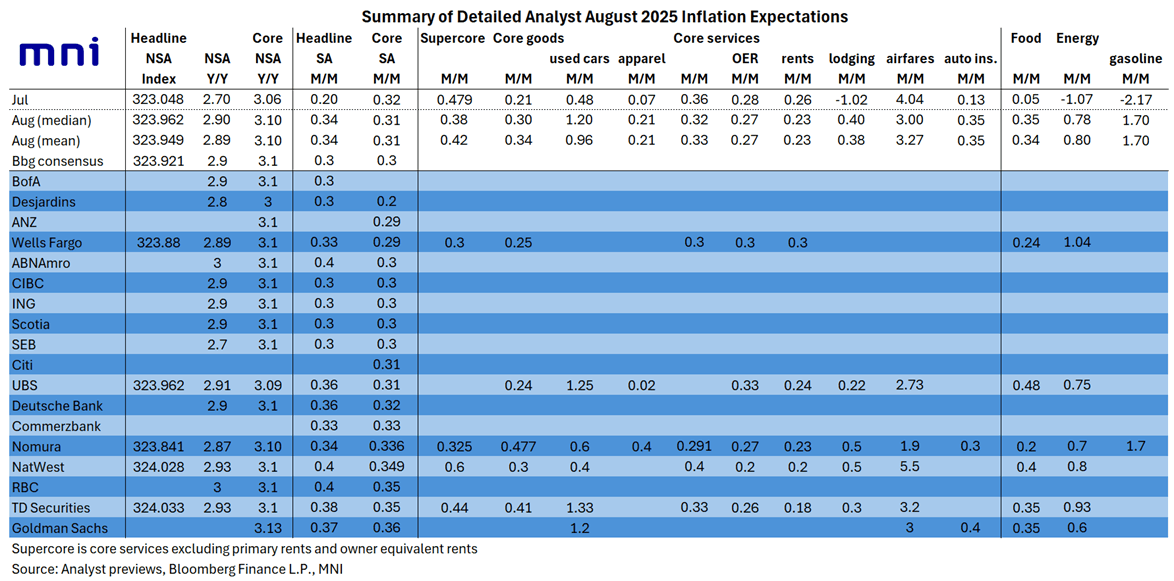

- August inflation data lands this week, with PPI out first on Wednesday September 10 at 0830ET, followed 24 hours later by the CPI report. Consensus (Bloomberg median) is for core CPI to come in at 0.3% M/M rounded in August, same as July, with the MNI unrounded median looking for 0.32% with a slight lean in the risks toward a rounding-up to 0.4%.

- Recall that the July CPI report saw further acceleration in monthly core inflation but the details defied expectations. The rise was driven by volatile services categories and - in a counter-intuitive finding amid continued tariff concerns - core goods were surprisingly soft (and inflation breadth appeared to moderate).

- But very strong July PPI data released subsequently, with undertones of businesses passing along higher tariff-related costs to consumers, reversed those dovish cues.

- Expectations for individual CPI categories see stronger food and energy prices vs July boosting headline inflation (to 0.36% vs 0.20% prior), and within core, “supercore” services cooling slightly (with a wide range of estimates) and housing inflation slightly softer even as core goods pick up from July.

- For PPI, current Bloomberg consensus is for a cooling after July’s hot print, with M/M final demand PPI at 0.3% (0.9% prior) and “core” (ex-food/energy/trade) also at 0.3% (0.6% prior).

- Of course, surprises to the PPI data could affect expectations going into the following day’s CPI.

- On that note, core PCE estimates are for 0.31% M/M vs 0.27% prior, with no analysts seeing core PCE printing above core CPI. That could change based on various PPI components that feed into PCE, but as it stands, the M/M core PCE estimate would be the highest since February.

- With the FOMC communications blackout underway, we won’t get any Fed reaction to the data until next week’s meeting is concluded.

- Given increasing focus on labor risks it’s hard to imagine a set of inflation readings that stops the Fed from cutting 25bp as expected, but it could help shape the updated rate and economic projections to be released at the meeting (including the 2025 “dot” median), as well as Chair Powell’s tone.

- In particular, FOMC participants’ debate over tariffs’ impact on goods prices has shifted somewhat into concerns that services prices are no longer softening to a degree that puts overall inflation on a path to 2%.