MNI UK Labour Market Review: August 2025 Release

Aug-12 09:54By: Emil Lundh

Employment

- The August UK labour market release was on balance stronger-than-expected, with 3m/3m employment growth surprising to the upside and the unemployment rate holding steady despite some risks of a one tenth increase.

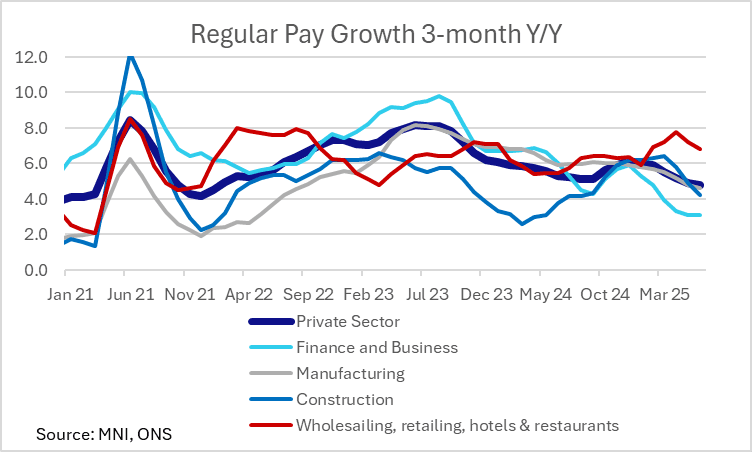

- However, private sector regular pay data remains consistent with the idea that wage growth is slowing. Meanwhile, data such as vacancies, RTI-PAY payrolls and other labour market metrics/surveys point to more subdued developments than the headline LFS figures suggest.

- We have argued that a continually softening labour market is a necessity for another quarterly cut in November. The August release was worth a modest hawkish reaction in BOE implied pricing, but there’s still far too much data (on both inflation and the labour market) to come before excluding a November cut. OIS markets currently price ~11bps of easing through that meeting.