MNI Riksbank Review - September 2025: That’ll Do

Sep-23 2025 13:39By: Emil Lundh

Sweden

Hidden PDF

EXECUTIVE SUMMARY:

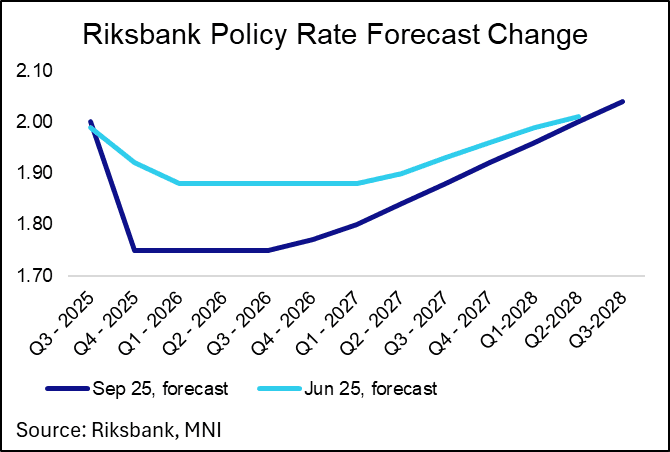

- The Riksbank cut rates by 25bp to 1.75% in September. It was a very close call, but MNI had leant in favour of such a move. The Board opted to provide additional support to the economy, following increased confidence that the summer acceleration in inflationary pressures is likely to be temporary. The policy statement noted that the policy rate “is expected to remain at this level for some time to come”, signalling a likely end to this easing cycle.

- The decision was not unanimous, with Deputy Governor Seim preferring to leave the policy rate unchanged “together with a policy rate path signalling some probability of a further cut later this year”.

- In line with the policy statement guidance, the September MPR rate path was flat at 1.75% through to Q3 2026 before starting to slope upwards

- The knee-jerk dovish reaction in SEK FX and rates markets following the decision did not last. 2-year SEK swap rates quickly unwound the ~4bp fall seen immediately after the rate cut was announced, eventually moving a few basis points higher on the session. We don’t think the decision should be interpreted as a “hawkish cut” though (certainly not when compared with Norges Bank last week). Markets were already coming into the decision pricing a 1.75% terminal policy rate, with today’s cut just bringing that move forward. It’s not surprising that the Riksbank views the outlook for GDP as somewhat better following the large fiscal stimulus recently announced by the Government.