RBNZ: MNI RBNZ Review-May 2025: RBNZ Keeping Options Open

- Download full report here.

- The RBNZ cut rates 25bp to 3.25% following a vote, the first in two years, that included an option to leave rates unchanged. The vote wasn’t unanimous with one dissenter but Governor Hawkesby said that there was consensus around the projections.

- RBNZ Governor Hawkesby reiterated today that the message at yesterday’s press conference was not to assume that a July rate cut is programmed into the MPC’s thinking.

- The MPC may want to wait and watch trade developments and how Q2 CPI (July 21), Q2 labour market and Q3 inflation expectations data (both August 7) print.

- Markets had fully priced in yesterday’s 25bp cut ahead of the decision, with a total of 64bps of easing expected by November 2025. That has now adjusted to 50bps, inclusive of yesterday’s move.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Monitoring Support

- RES 4: 165.43 High Nov 8

- RES 3: 164.90 High Dec 30 ‘24 and a key medium-term resistance

- RES 2: 164.55 High Jan 7

- RES 1: 163.76/164.19 High Apr 25 / High Mar 18 and the bull trigger

- PRICE: 162.19 @ 07:10 GMT Apr 29

- SUP 1: 161.41/159.48 50-day EMA / Low Apr 9

- SUP 2: 158.30 Low Apr 7 and key support

- SUP 3: 157.02 76.4% retracement of the Feb 28 - Mar 18 bull cycle

- SUP 4: 155.60 Low Low Mar 4

SHort-term weakness in EURJPY appears corrective and the trend condition remains bullish. Last week’s gains reinforce a bullish theme. Key S/T support lies at 158.30, the Apr 7 low. A break of it is required to signal scope for a deeper retracement. This would open 157.02, a Fibonacci retracement. First support to watch is 161.41, the 50-day EMA. Attention is on 164.19, the Mar 18 high and a bull trigger. Clearance of this hurdle would resume the uptrend.

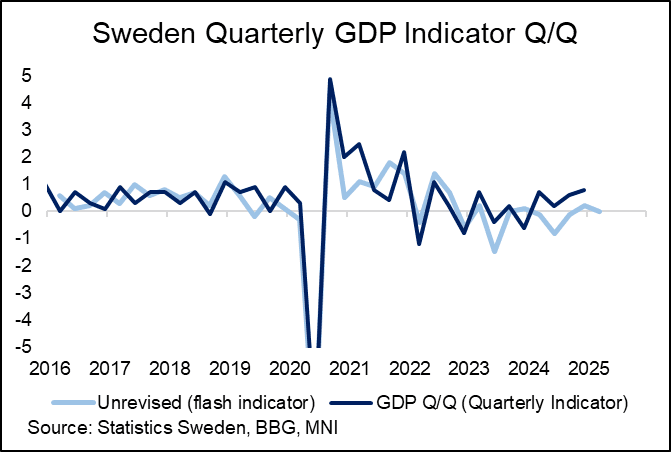

SWEDEN: Weaker Than Expected Q1 GDP Indicator - But Plenty of Caveats As Always

The Q1 GDP indicator was weaker-than-expected at 0.0% Q/Q (vs 0.8% in Q4). Consensus was for 0.2% Q/Q, while the Riksbank March MPR had forecast a 0.5% reading.

- The weaker-than-expected print comes despite a decent rebound in the March GDP indicator of 0.6% M/M, and an upward revision of February to -0.7% (vs -1.5% initial).

- As ever, one should not read too much into this indicator. It is often heavily revised and a poor predictor of actual GDP outcomes – see chart

- Little net reaction in Scandi FX to this morning’s swathe of Scandi data (which also included Norway retail sales, Sweden trade balance, lending and wages).

- A more important barometer of the Swedish economy will be the April Economic Tendency Indicator at 0800BST/0900CET.

BTP TECHS: (M5) Northbound

- RES 4: 121.93 76.4% of the Dec 5 ‘24 - Mar 14 bear leg (cont)

- RES 3: 121.43 1.618 proj of the Mar 14 - Apr 4 - 9 price swing

- RES 2: 121.00 High Feb 7 (cont) and a key resistance

- RES 1: 120.65 1.382 proj of the Mar 14 - Apr 4 - 9 price swing

- PRICE: 120.02 @ Close Apr 28

- SUP 1: 119.42/118.96 High Apr 22 / 20-day EMA

- SUP 2: 117.28 Low Apr 10

- SUP 3: 116.06 Low Apr 9

- SUP 4: 115.75 Low Apr 14 and a bear trigger

BTP futures have traded higher last week and the contract is holding on to the bulk of its recent gains. Last Thursday’s strong rally reinforces current bullish conditions. The move higher resulted in the break of key resistance at 120.39, the Feb 28 high. Sights are on 120.65 next, a Fibonacci projection. Firm support to watch lies at 118.96, the 20-day EMA. The contract is overbought, a pullback would unwind this trend condition.