EUROPEAN INFLATION: MNI Projects 2.0% Y/Y German National CPI, Core 2.6-2.7%

From state-level data that equates to 89.1% weighting of the national July flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) rose by around 2.0% Y/Y (2.0% prior) and rose around 0.3% M/M. See the tables below for full calculations.

- Analyst consensus stands at 2.0% Y/Y (1.95%Y/Y Bloomberg median to 2dp) and 0.2% M/M, but is skewed to the upside for the M/M print - so there might be some marginal upside risks to consensus.

- Current tracking of Core CPI (ex-energy and food, based on 50% of the national index) implies around 2.6-2.7% Y/Y (2.7% prior).

- We will provide a follow-up bullet looking at underlying drivers in due course.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP - but the direction of the surprise is generally the same.

| Y/Y | July (Reported) | June (Reported) | Difference |

| North Rhine Westphalia | 1.8 | 1.8 | 0.0 |

| Hesse | 2.4 | 2.3 | 0.1 |

| Bavaria | 1.9 | 1.8 | 0.1 |

| Brandenburg | 2.2 | 2.2 | 0.0 |

| Baden Wuert. | 2.3 | 2.3 | 0.0 |

| Berlin | 2.1 | 2.0 | 0.1 |

| Saxony | 2.1 | 2.4 | -0.3 |

| Rhineland-Palatinate | 1.8 | 1.8 | 0.0 |

| Lower Saxony | 1.9 | 2.2 | -0.3 |

| Saarland | 2.2 | 1.9 | 0.3 |

| Saxony-Anhalt | 2.5 | 2.5 | 0.0 |

| Weighted average: | 1.98% | for | 89.1% |

| M/M | July (Reported) | June (Reported) | Difference |

| North Rhine Westphalia | 0.2 | -0.1 | 0.3 |

| Hesse | 0.3 | 0.1 | 0.2 |

| Bavaria | 0.3 | -0.1 | 0.4 |

| Brandenburg | 0.3 | 0.2 | 0.1 |

| Baden Wuert. | 0.4 | 0.2 | 0.2 |

| Berlin | 0.3 | 0.2 | 0.1 |

| Saxony | 0.2 | 0.2 | 0.0 |

| Rhineland-Palatinate | 0.2 | 0.2 | 0.0 |

| Lower Saxony | 0.3 | 0.2 | 0.1 |

| Saarland | 0.5 | 0.1 | 0.4 |

| Saxony-Anhalt | 0.3 | 0.1 | 0.2 |

| Weighted average: | 0.31% | for | 89.1% |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBP: New Cycle Highs Expose Next Resistance

- Latest press lower for the USD has prompted GBP/USD to show to a new cycle high at 1.3773 - this is now the best marked levels since October 2021 and extends the bull cycle in the pair.

- USD is certainly the driver here, and while GBP is firmer against the EUR on the day, GBP/JPY is under pressure as the cross undergoes a corrective pullback off last week's highs.

- An uptick in futures volumes on the break to new highs clearly helping here, and shifts focus to 1.38 round number resistance and then the October 20th 2021 high beyond at 1.3835

- The difficulty of passage of today's welfare bill in the House of Commons may not be directly market relevant, but the scale of opposition will serve as a further reminder of the hurdles facing the PM's pro-growth agenda.

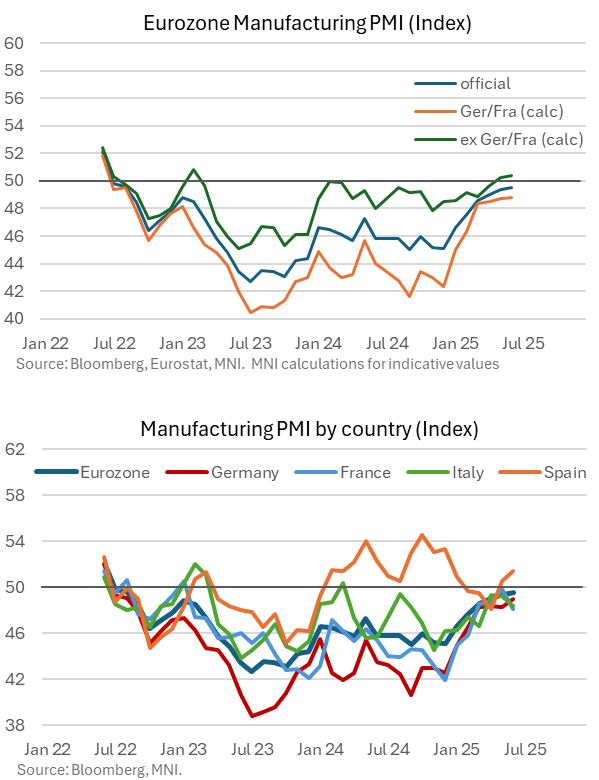

EUROZONE DATA: June Manuf PMI: Weaker Output Charges Seen Across The Region

The Eurozone-wide June manufacturing PMI was little changed from the flash reading at 49.5 (vs 49.4 flash and prior). We estimate the Germany/France manufacturing PMI at 48.8 (vs 48.7 flash and prior) and the ex-Germany and France PMI at 50.4 (vs 50.3 flash and prior). Positive momentum in Spain and, to a lesser extent Germany, extended in June, while France and Italy saw renewed deteriorations.

Interestingly, the Eurozone-wide release noted that new export orders were unchanged on the month - somewhat contrary to the weak signals seen in the Spanish, Italian and French releases earlier this morning. However, a pullback in output charges was seen throughout the region, with some countries highlighting the stronger exchange rate as driver of weaker input costs.

Key notes from the Eurozone wide release:

- "Reduced staffing numbers and lower stocks of purchases were negative influences on the headline PMI in June, while rising production had a positive impact".

- "Encouragingly, total new work stabilised during the latest survey period, thereby ending a 37-month period of decline. Sales made to export customers were also unchanged over the month, which halted the continuous downturn seen since March 2022".

- "Production volumes across the Euro area manufacturing sector increased for the fourth successive month in June. However, the rate of expansion was only marginal and eased to its weakest since March".

- "Lower employment has been recorded throughout the past 25 months and the rate of job shedding was slightly faster than in May. Cutbacks to input buying also continued in June, albeit to the least marked extent for three years. Reduced purchasing activity partly reflected ongoing efforts to streamline inventories"

- "Purchasing costs meanwhile decreased for the third successive month, which led to another marginal reduction in average prices charged by euro area manufacturers".

- "Finally, business optimism continued to recover from April’s recent dip. Confidence levels regarding prospects for output growth over the next 12 months were the highest for more than three years in June and comfortably above the long-run series average".

SPAIN T-BILL AUCTION RESULTS: 6/12-month Letras results

| Type | 6-month letras | 12-month letras |

| Maturity | Jan 16, 2026 | Jul 10, 2026 |

| Amount | E1.293bln | E4.087bln |

| Target | E5-6bln | Shared |

| Previous | E1.853bln | E3.927bln |

| Avg yield | 1.872% | 1.900% |

| Previous | 1.890% | 1.878% |

| Bid-to-cover | 3.1x | 1.71x |

| Previous | 2.02x | 1.45x |

| Previous date | Jun 03, 2025 | Jun 03, 2025 |