US: MNI POLITICAL RISK - Govt Shutdown Day 8, No Sign Of Offramp

Download Full Report Here

- President Donald Trump will receive an intel briefing in the morning before participating in a “roundtable on ANTIFA” at 15:00 ET 20:00 BST, as National Guard troops arrive in Chicago.

- Senate Majority Leader John Thune (R-SD) teed up a sixth vote on the duelling Republican and Democratic government funding measures at 11:20 ET 16:20 BST. Both bills are expected to fail.

- Republicans are struggling with strategy to ramp up pressure on Democrats. Earlier this week, Trump undermined Republican messaging by hinting at a bipartisan deal on Obamacare. The White House has also offered mixed signals on federal layoffs. Air traffic controller shortages could play a role in ending the shutdown.

- The Trump administration has pushed back plans for a farmer bailout due to the government shutdown.

- The White House is weighing up cancelling an additional USD$12 billion in clean energy funding.

- Canadian Prime Minister Mark Carney escaped an Oval Office meeting without a public blowout, but little progress towards a trade deal with Trump.

- Secretary of State Marco Rubio will attend an October 9 ministerial in Paris to discuss Gaza peace negotiations.

- Senate Democrats will force a war powers vote on Venezuela as Trump moves closer to open conflict with Caracas.

- Russia's Deputy Foreign Minister said efforts at Ukraine diplomacy discussed at the Putin-Trump summit in Alaska have been exhausted.

- Poll of the Day: Democrats are in a weaker midterm position than during Trump's first term.

Full Article: US DAILY BRIEF

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP: BoE Pricing Could Spell Difficulties for Consensus EURGBP Long View

While broader G10 FX ranges are muted, GBP/USD has improved to the best levels of the session, hitting 1.3536 to narrow the gap with the post-payrolls highs of 1.3555. Clearance here would put the price at new monthly highs and within range of 1.3595 - clustered horizontal resistance.

- Currency markets have proven more sensitive to volatility in the longer-end in recent weeks - of particular relevance to GBP given the uptrend in 30y UK Gilt yields - a recent triangle breakout on the daily chart reinforces this theme. Sensitivity here

- As such, politics and the near-term fiscal trajectory of the UK are to remain a key driver for markets here. Keir Starmer's reshuffle will likely be ineffectual for markets given Chancellor Reeves remains in place headed into the November 26th Autumn Budget, although recent appointments of economic advisers to No. 10 have raised some speculation that Reeves' influence over economic policy may have waned.

- As a result, sell-side remain cautious on GBP - however the vast majority prefer long EUR/GBP exposure over exposure to USD given the building pricing of a Fed Sept cut of potentially more than 25bps. This is despite sell-side pushing out expectations of BoE rate cuts this year (see Deutsche Bank, HSBC earlier today) - an extension of which could work against the consensus view of EURGBP higher. Key support to watch lies at 0.8597, the Aug 14 low. Clearance of this level would reinstate the recent bearish threat for the cross.

SPAIN T-BILL AUCTION PREVIEW: On offer this week

Spain has announced it will be looking to sell a combined E2.0-3.0bln of the following letras at its auction tomorrow, September 9:

- the 3-month Dec 5, 2025 letras

- the 9-month Jun 5, 2026 letras

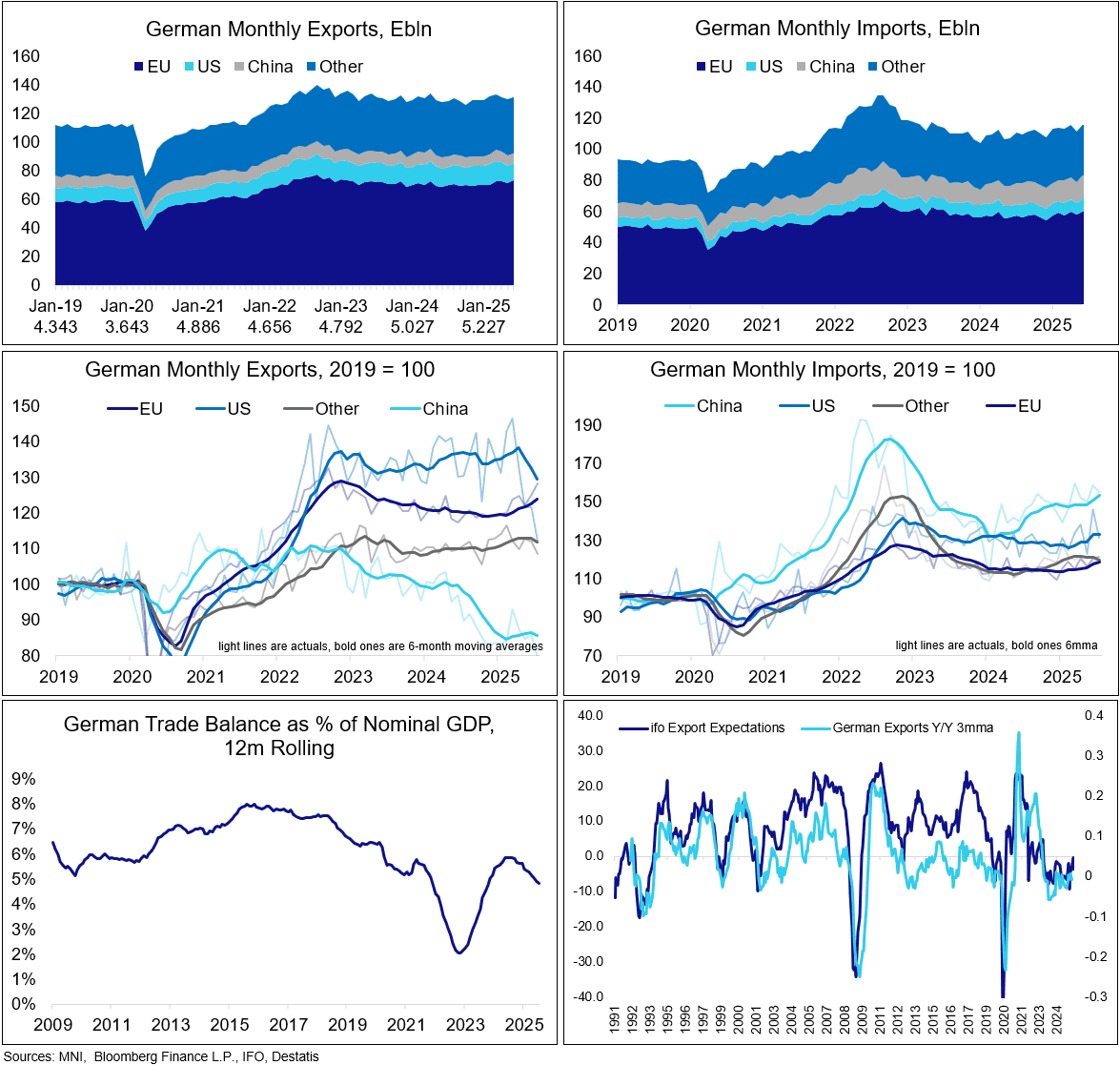

GERMAN DATA: Exports To US and China Continue Decline While Trade W/ EU Firmer

The German trade surplus, contrary to expectations for an uptick, decreased to E14.7bln in July (seasonally-adjusted, vs E15.5bln cons, E15.4bln prior, revised from E14.9bln), the second lowest since May 2023. The decrease came as an exports decline (-0.6% M/M vs 0.1% cons, 1.1% prior, revised from 0.8%) outpaced marginally lower imports (-0.1% M/M vs -1.0% cons, 4.2% prior, revised from 4.1%). Recent trends in the data suggest that German trade is becoming more EU-centric.

- As a % of nominal GDP on a 12-month rolling basis, the trade surplus extended its current downtrend, at 4.8% as of July, 1.1pp below levels seen around a year ago. That compares with a 2015 high of 8.0% and 2022 low of 2.1% (see bottom left chart).

- Across countries and back on a nominal basis, the US continues to stand out with exports to the country collapsing, sitting at their lowest since December 2021 after four consecutive sequential declines (23.5% decline vs March which was underpinned by tariff-front running).

- Exports to China also screen weak, printing the lowest since August 2016 and having declined 26.5% if comparing the last three months to the series' highs. This decline comes against the backdrop of reports (1,2) suggesting China has built significant manufacturing overcapacity in recent years, indicated by domestic supply rising faster global demand, rising numbers of lossmaking industrial firms in the country, as well as declining capacity utilization, which may weigh on demand for German products.

- Exports to and imports to other EU countries both appear to be on a solid uptrend, meanwhile, confidently standing above cycle lows seen around a year ago.

- IFO export expectations deteriorated in August, falling to -3.6 points, from -0.3 points in July. “Disillusionment is spreading in export business [...] although a tariff rate of 15 percent from the US is less than feared, it will nevertheless weaken export momentum”, IFO comments.