NORGES BANK: MNI Norges Bank Review: November 2025 - No MPR, No Signals

Nov-06 14:01

CLICK HERE FOR THE FULL PUBLICATION

EXECUTIVE SUMMARY:

- Norges Bank held the policy rate at 4.00% in November, fully in line with expectations. The policy statement indicated that “no new information has come in that indicates a material change to the outlook for the Norwegian economy since the monetary policy meeting in September”.

- As such, guidance was completely unchanged: “The outlook is uncertain, but if the economy evolves broadly as currently envisaged, the policy rate will be reduced further in the course of the coming year. "

- The write-up of the Committee’s Assessment didn’t contain any major surprises, but some elements leant slightly hawkish on the margin, in our view. That likely contributed to a modest ~3bp rise in the 2-year NOK swap rate in the aftermath of the decision.

- However, the broader outlook for Norges Bank implied pricing is little changed. Markets still price about 50bps of easing though the next 12 months, one 25bp cut more dovish than implied by the September MPR rate path.

- There remain a range of analyst views around the magnitude and pace of easing in 2026. Some analysts see no more cuts as their base case, while others expect three more cuts to a terminal of 3.25%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: CANADA SEP IVEY PURCHASING MANAGERS INDEX 59.8 SA

Oct-07 14:00

- CANADA SEP IVEY PURCHASING MANAGERS INDEX 59.8 SA

FOREX: Markets May Be Erring in Favour of Larger RBNZ Cut; NZD Underperforms

Oct-07 13:56

The strong open for US equities alongside the retreat from highs for the US 10y yield has helped the USD edge off the day's best levels, an effect most evident in GBP/USD, which has recovered back above the 1.34 handle.

- The medium-term run higher in gold has continued, helping spot to new record highs of 3985.7 (although in futures space, COMEX gold has now shown above $4,000 for the first time), but the strength in gold looks pretty isolated: silver, oil prices and base metals are all seen lower, which may be limiting the bounce off lows for AUD/USD, which is yet to bounce back above 0.6600.

- NZD remains the underperformer into the RBNZ rate decision, and with 36bps of easing priced for Wednesday’s meeting and a cumulative 63bps by November, markets may be erring in favour of a more sizeable rate cut this week.

- A return lower for NZD would re-open upside in AUD/NZD through to 1.1355-67 resistance, clearance above which returns focus to the bull trigger and cycle high at 1.1418.

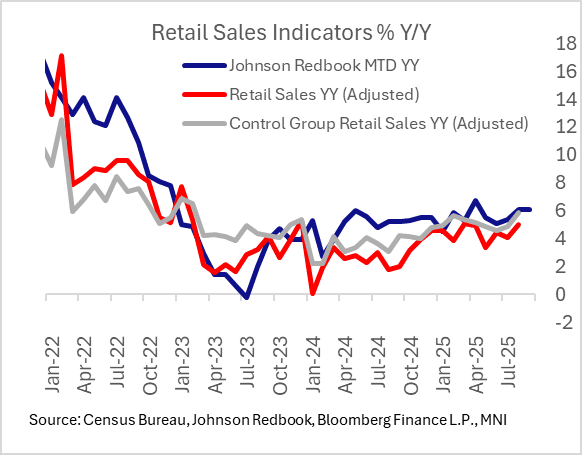

US DATA: Redbook Points To Robust Q3 Retail Sales Momentum, Official Data Or Not

Oct-07 13:42

Johnson Redbook Retail Sales rose by 5.8% Y/Y in the week ending Oct 4, bringing growth in the full month of September to 6.1% Y/Y (under their methodology, the month has 5 retail weeks). That's slightly softer than the 6.3% targeted by retailers but would still represent robust sales through the end of Q3.

- Additionally, their preliminary target for October growth (based on retailers' plans) is 5.7% Y/Y.

- It's still uncertain of course, but with every day of the federal shutdown that goes by, it's less and less likely we get the September Census Bureau retail sales report as scheduled on Oct 16.

- In the meantime we will be using proxies such as the Redbook index and the Chicago Fed CARTS index (which uses still-available data including payment card transactions, retail foot traffic, gasoline sales, and consumer sentiment to proxy retail sales ex-autos). These, plus Wards Automotive September sales, have all shown robust activity in the month consistent with a continued uptick in activity (a rough estimate is that nominal ex-autos/gas sales could post around 6% 3M/3M quarterly annualized growth for Q3, the strongest momentum seen since mid-2024).

- The Redbook report also notes: "As Amazon’s annual 48-hour Prime Big Deal Day sales kick off on October 7th, several major retailers have also announced significant promotional sales in advance of Prime Day. Discount stores have performed well throughout the week, buoyed by essentials such as food and household supplies. Looking ahead, October consists of four weeks, ending November 1st on the retail calendar, and includes two major holiday events: Columbus Day and Halloween."