MNI: RBA Cash Rate Strategy Hinges On Q4 Data - Fmr Staffers

A further 1% quarter-on-quarter rise in trimmed-mean inflation in Q4 will pressure the Reserve Bank of Australia to raise its 3.6% cash rate in 2026, but geopolitical and global economic risks are likely to encourage caution, and higher unemployment could eventually prompt a return to easing later in the year, former staffers told MNI.

A Q4 quarter-ended trimmed mean print of 0.8-0.9% would likely see the RBA board hold rates and await further evidence on the trajectory of inflation, while another 1% increase would drive a hike, said Mariano Kulish, University of Sydney professor and former RBA senior manager. He noted that the Bank had not raised rates sufficiently to contain inflation, as evident in Q3’s 3% trimmed mean result, which also drove the Board's caution this week. (See MNI RBA WATCH: Bullock Strikes Cautious Tone Following Pause)

“One of the risks of cutting too early is exposure to shocks that could push inflation higher, such as tariffs,” Kulish said. “Repeatedly missing the target can reset market expectations, making it harder to anchor inflation. Another quarter of 1% trimmed mean growth should warrant a further rate hike.”

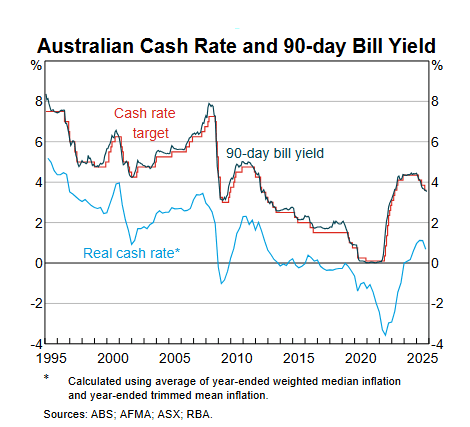

Kulish criticised the Bank’s cautious stance, arguing that preserving employment while waiting for inflation to normalise risks undermining its credibility. “If the Bank is going to fight deviations from its target, it should be seen as responding to adverse inflation outcomes,” he said, noting that low real interest rates make it unclear where deflationary pressures would come from to pull inflation down without further rate rises. (See chart)

However, a hike in 2026 would require a significant shift in the RBA’s signalling away from its “narrow path” narrative of protecting labour market gains, Kulish added. “This is my main criticism of the Bank at this stage ... it’s not taking a decisive or active stance, as it doesn’t want to be seen as causing a recession,” he said. “The Bank should be seen as responding to adverse inflation outcomes. Given the shocks, if some output has to be lost, then you lose a bit of output."

Markets expect the cash rate to remain at 3.6%, with further easing unlikely before late 2026, following the Board’s decision to hold rates this week.

LABOUR MARKET RISKS

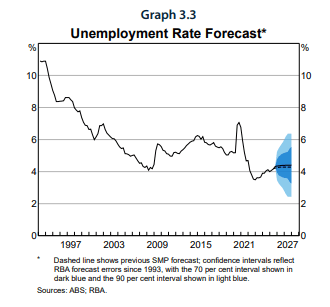

Callam Pickering, APAC senior economist at employment website Indeed.com and former RBA senior analyst, said the Bank’s unemployment projection, which sees the rate peak at 4.4% over the projection period, may be overly optimistic, given September’s 4.5% print. “Unless employment growth picks up significantly, unemployment could continue rising," he said. "Growth we’ve seen in 2025 isn’t sufficient to keep the rate at 4.4%." (See chart)

Pickering highlighted structural issues in the labour market. Much of Australia’s post-pandemic job boom was concentrated in healthcare and social assistance, driven by the expansion of the NDIS and the country’s aging population. Growth in this sector has slowed over the past year, while private sector job creation has been soft, he noted. “If the private sector doesn’t fill the gap, employment growth could slow, and the unemployment rate will rise," he said, noting an increase toward 5% in 2026 would prompt the Bank to ease.

While Pickering acknowledged that a Q4 trimmed mean of 0.8-1% could justify rate hikes and add pressure on the board, he doubted this outcome, predicting inflation is more likely to moderate.

GLOBAL RISKS

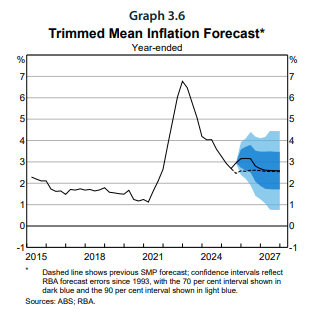

Martin Eftimoski, an RBA economist from 2017 to 2021, cautioned against over-interpreting a single quarter of data. He noted that the Bank relies on mean reversion in its forecasts, and short-term deviations should not dictate policy shifts. “The Bank uses long-run historical averages for productivity and CPI growth to guide expectations. (See chart) Temporary shocks do not warrant major adjustments,” he said.

Global macroeconomic risks, including slowing growth in China and the U.S., would likely prevent the RBA from hiking rates unless inflation showed sustained strength over multiple quarters, he added. “The global picture is not conducive to interest rate increases if inflation is only mildly above target,” he said. "If all these global macro economic risks somehow disappear in the next two quarters, the governor probably should hike. But that's not the world we live in."