MNI Norges Bank Review: Jun '25 - Cut Against All Odds

Jun-19 14:27By: Emil Lundh

Norway

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK: MNI Norges Bank Review - 2025-06.pdf

EXECUTIVE SUMMARY:

- Norges Bank surprisingly delivered a 25bp cut to 4.25%, going against analyst expectations and market pricing that were overwhelmingly in favour of a hold. Higher confidence in the inflation outlook was the key driver of the pivot, with some attention also given to gradually rising unemployment rates. The policy statement noted that “if the economy evolves broadly as currently projected, the policy rate will be reduced further in the course of 2025”.

- Clearly, the pullback in inflationary pressures after the Q1 acceleration (which prompted a U-turn on prior guidance for a March cut) provided the Board with sufficient confidence to start its easing cycle. Zooming out, the decision to cut one quarter earlier than expected is unlikely to have a meaningful impact on macroeconomic outcomes, or the likely medium-term terminal rate.

- The problem for markets is that Norges Bank’s credibility must be called into question for future decisions, given the March rate path and recent guidance offered little to suggest a June cut was a material possibility. Although inflation was lower than expected heading into the June decision, it was similarly softer than projected throughout 2024, when Norges Bank consistently disappointed on expectations for a dovish pivot. The fact Norges Bank essentially enter a communication blackout between rate decisions also doesn’t help with preparing markets ahead of policy decisions.

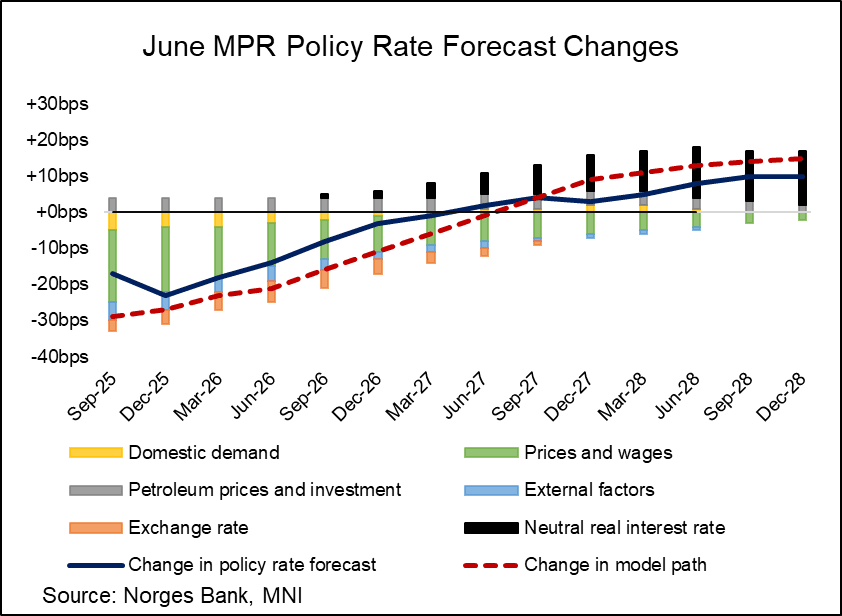

- The June MPR rate path was revised up to 23bps lower compared to March (Q4 2025 average at 3.98% versus 4.21% in March). In the press conference, Governor Wolden Bache detailed that the new rate path was consistent with one or two more cuts this year. Analyst calculations on the rate path suggest that the MPR meetings (September and December) are the most likely meetings for additional cuts to be delivered. Analysts generally expect 25bp cuts in September and December.