POLAND: MNI NBP Review - Dec 2025: Entering 'Wait-And-See' Mode

Download Full Report Here

Executive Summary:

- The MPC brought the amount of easing this year to 175bp, taking the key rate to 4%.

- The panel will likely move into wait-and-see mode before considering more cuts.

- The Governor thought 4% rate was ‘perfect’ but other members may prefer a lower level.

The National Bank of Poland (NBP) delivered the widely anticipated 25bp ‘adjustment’, bringing the cumulative amount of easing this year to 175bp and taking the reference rate to 4%. The Governor struck celebratory notes after concluding that the central bank has managed to anchor inflation at the +2.5% Y/Y target but signalled that the Monetary Policy Council (MPC) may slow the pace of easing. In his personal view, the current level of the reference rate is ‘perfect’ and could be left unchanged for longer, but other members may push for a further reduction. Over the near term, the Council will move into a ‘wait-and-see’ mode to observe the impact of past monetary policy action, before reconsidering further steps. We expect the NBP to recommence cuts in March after seasonal and temporary uncertainty factors dissipate and the Council receives a fresh macroeconomic projection.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

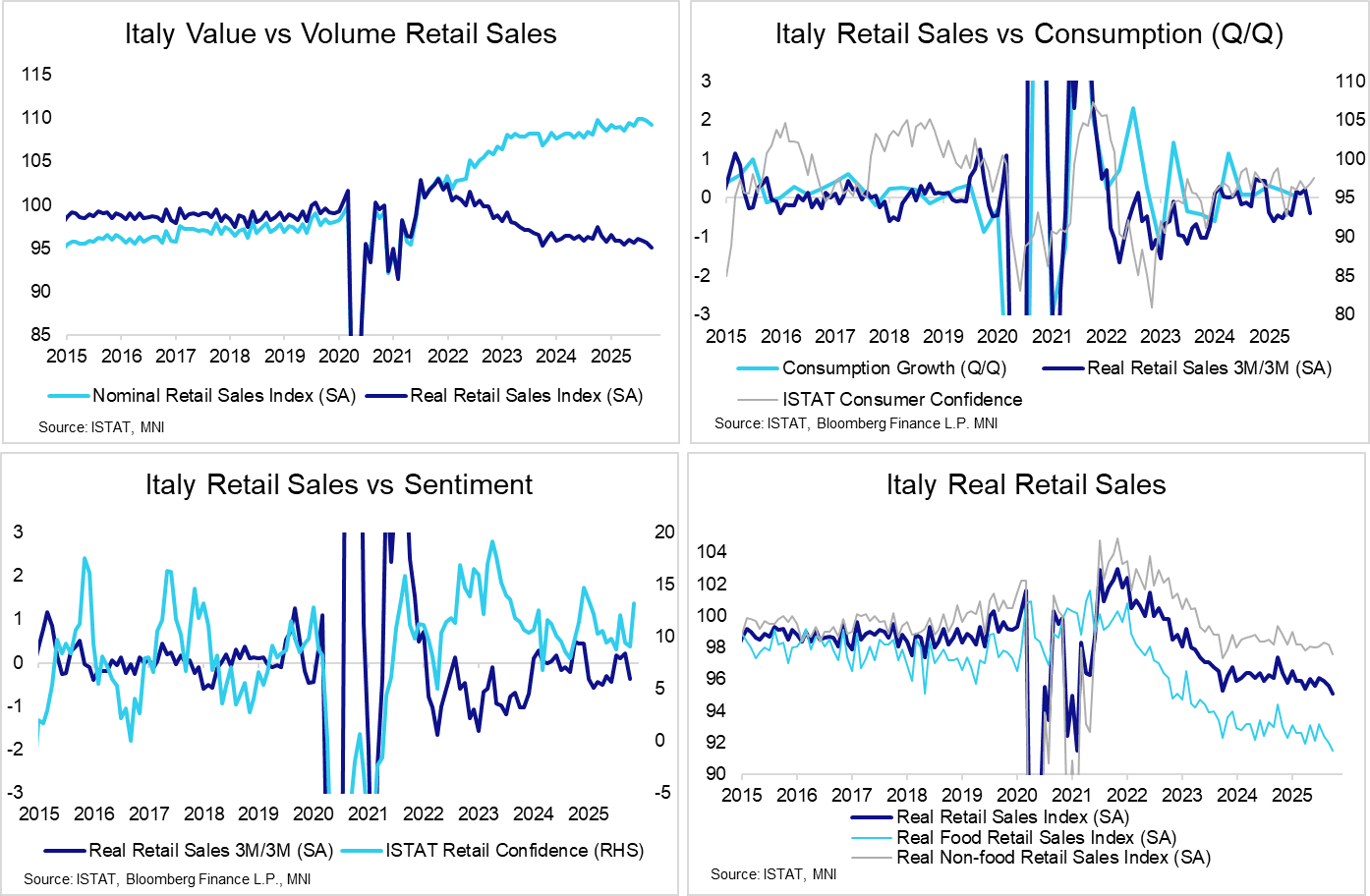

ITALY DATA: Italy Retail Sales Continue Weaker, Food Sees Sustained Fall

Italian retail sales momentum remains weak. In September, real seasonally adjusted retail sales fell 0.5% M/M SA (vs -0.3% prior), and 1.4% Y/Y NSA (vs -1.2% prior). On a rolling quarterly basis, sales fell 0.4% (vs 0.2% prior), returning to negative territory for the first time since April. A reminder that Italian Q3 flash GDP was weaker-than-expected at 0.0% Q/Q (vs 0.1% cons, -0.1% prior). ISTAT noted at the time that domestic demand was a drag on growth, and today's retail sales data suggests consumption was a contributor to this dynamic.

- Both food and non-food sales contributed to the decline in real retail sales in September. Food sales fell 0.5% M/M SA (vs -0.4% prior), the third consecutive month of decline. On a 3m/3m SA basis, food sales fell 0.9% (vs a 0.2% increase prior). Non-food sales decreased 0.6% M/M SA (vs -0.1% prior), though remains relatively more stable on a 3m/3m basis (0.0% September vs 0.2% August). Looking at non-food Y/Y trends, the press release notes the largest increase was seen in "Cosmetic and toilet articles" (4.0% Y/Y), while the sharpest declines were observed in "Shoes, leather goods and travel items (-5.7%) and Clothing (-5.2%)".

- Looking ahead, ISTAT's retail confidence series rebounded in October. However, this indicator's correlation with actual retail sales momentum is relatively weak.

FOREX: USDCAD Extending Winning Streak, Testing Top of Bull Channel

- In line with the broader greenback advance since the FOMC, USDCAD is also on a 5-session winning streak, currently trading at the highest level since April 09. Yesterday, we highlighted that the pair had breached 1.4080, the Oct 16 high, to confirm a resumption of the uptrend.

- Topside momentum has gained traction, with domestic developments assisting the move above 1.41. Canada yesterday budgeted its biggest ever cash deficit this fiscal year, excluding the pandemic, on a fiscal push to revitalize sluggish growth in the country.

- This week’s extension for USDCAD highlights a clear reversal of the corrective bear leg between Oct 14 - 29. Spot is currently testing 1.4136, the top of a bull channel drawn from the Jul 23 low. 1.4167 is the next level of note, the 50.0% retracement of the Feb 3 - Jun 16 bear leg, and above here, attention will be on 1.4274, the April 09 high.

- Final services PMI data will be released later today, however, it’s the October employment data that will be the focus on the Canadian data calendar, set to be a cleaner release given the lack of accompanying US figures. Currently a -5k change in employment is expected, with the unemployment rate seen remaining steady - further increases from the current 7.1% could fuel dovish bets.

US TSY FUTURES: Long Setting In WN Dominates On Tuesday

OI data points to a mix of net long setting (TU, FV & WN) and short cover (TY, UXY & US) as Tsy futures ticked higher on Tuesday.

- There was a bias towards net long setting, with the movement in WN positioning providing the only real swing of note.

| 04-Nov-25 | 03-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,622,213 | 4,596,654 | +25,559 | +995,257 |

FV | 6,816,873 | 6,796,041 | +20,832 | +910,609 |

TY | 5,434,597 | 5,445,139 | -10,542 | -715,395 |

UXY | 2,470,454 | 2,472,105 | -1,651 | -150,249 |

US | 1,883,365 | 1,888,998 | -5,633 | -729,410 |

WN | 2,144,627 | 2,133,029 | +11,598 | +2,214,520 |

|

| Total | +40,163 | +2,525,333 |