MNI INTERVIEW: IMF’s Adrian Sees Risks From Frothy Stocks

Surging stock valuations raise the risk that a shock could lead to the kind of sharp reversal that spills over into private credit and eventually the broader banking system, senior IMF official Tobias Adrian told MNI.

“We could see a negative shock that leads to a repricing, which in itself is probably not a financial stability concern, but that could trigger a forced selloff in some nonbanks,” said Adrian, Financial Counsellor and Director of the IMF’s Monetary and Capital Markets Department, in an interview at his offices ahead of this week’s IMF fall meetings. “That could then spill over into the banks as well.”

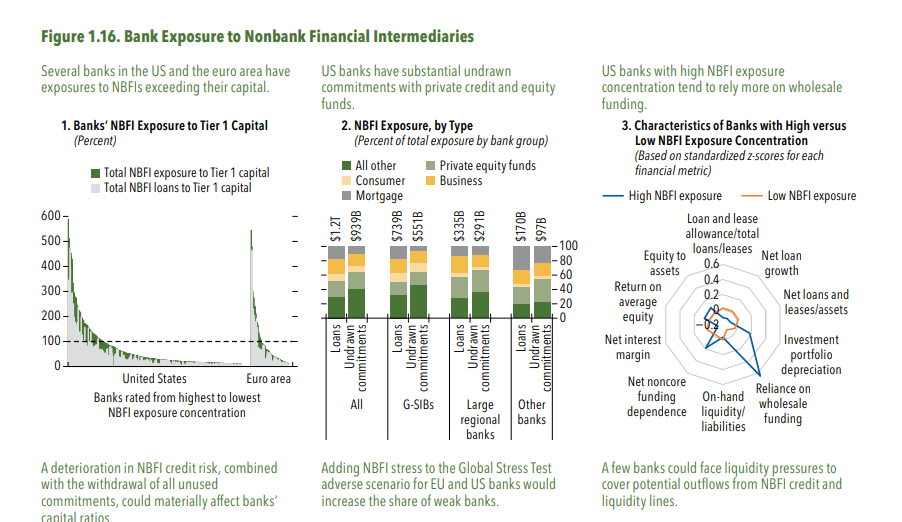

Rising linkages between non-bank financial institutions and the traditional banking system raises the risk that troubles into one area might quickly spread to others.

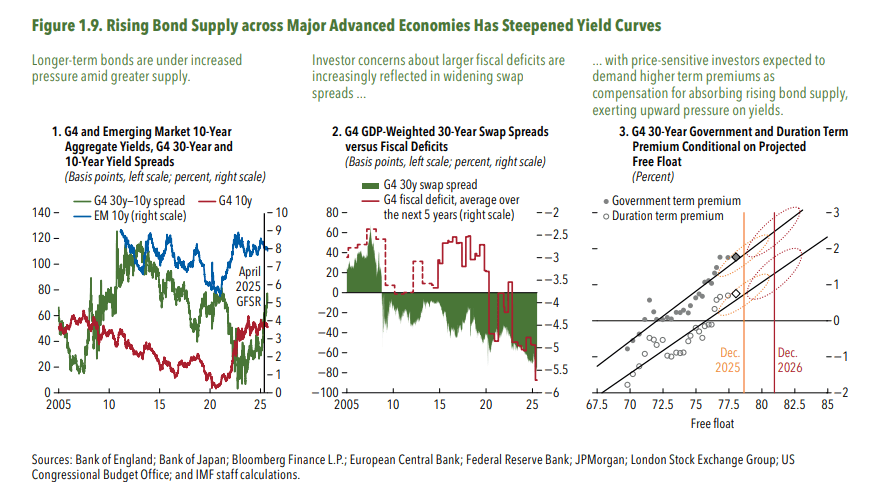

One additional worry for the Fund is high deficit levels in major economies which lends itself to spikes in longer-term bond yields that would exacerbate financial risks. “Long-term premia continue to rise, and there may be continued pressure on these long-term bond premia.”

STABLECOINS

Adrian said he is closely watching the growth of the market for stablecoins and sees the financial stability risks from that market as akin to those from money market funds – adding that regulators should address those risks using similar tools.

“You could have redemption pressures in the stablecoins, just as you have redemption pressures in money market funds, and that could then trigger some redemption pressures in the underlying bill market and the repo market, leading to market functioning issues and ultimately, potentially financial stability concerns,” he said.

“The regulatory response to that is very similar to what we have done in money market funds, which is to impose liquidity requirements, in some countries capital requirements as well.”

BENIGN BACKDROP

Adrian described the global economic backdrop as benign, adding that the effects of tariffs had thus far not been as pronounced as some had feared.

“We always believed that the economy would be resilient, and the economy turned out to be resilient. Having said that, growth is somewhat below the forecast we had prior to the tariff announcement. So there's some ratcheting down of global growth. And there's certainly some upward surprise inflation in the U.S.,” he said.

Still, he expects inflation to subside back to the Fed’s target within a reasonable timeframe, adding that the Fund is broadly aligned with the U.S. central bank’s policy approach so far. The Fed last month cut interest rates in an effort to stymie the possibility of a significant deterioration in the labor market following recent downward revisions to monthly payrolls growth.

“It's really about the balance between supply and demand, so to the extent that demand is slowing down, as can be seen in the labor market, that would put downward pressure on inflation,” said Adrian.

He was not overly concerned about new threats from the United States to further hike tariffs on China, citing muted market concerns for now despite last week’s initial selloff. “The magnitudes are small relative to April. There is some perception that perhaps there will be reassuring policy developments.”

The report itself urged officials at the world’s major central banks to be measured in reducing interest rates further because inflation remains elevated and tariff effects are still filtering through.

“In jurisdictions where inflation is still well above target and where tariffs might constitute a supply shock, central banks need to proceed carefully with any easing and maintain their commitment to price stability mandates,” the Fund said.