MNI Fed Review - Dec 2025: Not A Particularly Hawkish Cut

Dec-10 2025 21:38By: Tim Cooper

US

Hidden PDF

EXECUTIVE SUMMARY:

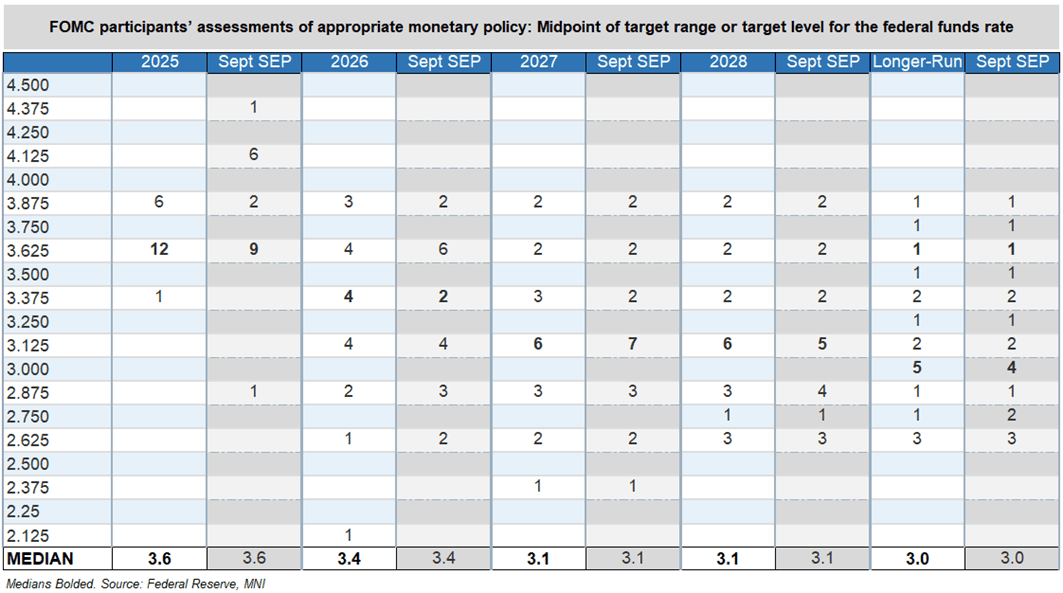

- The FOMC delivered what was widely anticipated to be a “hawkish cut” at the December meeting, lowering the Funds rate range by 25bp to 3.50%-3.75% while portraying a cautious stance on further adjustments in the Statement and Dot Plot.

- But with most of the main communications having been well-anticipated – from the subtle shift in forward guidance in the Statement, to the unchanged Dot Plot rate forecast medians – overall the meeting outcome brought some slight dovish surprises and a concomitant market reaction.

- Rates markets ended up pricing in two 25bp cuts thorough October 2026 a little more firmly (by about 3bp) than they did before the decision, though a January cut remains a longshot (about 25% implied probability before and after the meeting).

- We go through the composition of the Dot Plot (unchanged medians, including 1 cut in each of the next 2 years), the adjustments to the economic projections (slightly lower inflation profile through 2026), and the change in Statement language (eyeing the “extent and timing” of future adjustments) in our review – but none of these were at all surprising. In particular, the paucity of official economic data since the September projections made it unlikely that participants would have a radically changed view of the outlook, and so it proved in the SEP.

- That didn’t mean there weren’t some surprises, but these were marginally dovish leaning on net.

- We haven’t yet seen any analyst view changes following the meeting, though there’s probably not enough new information received that would change opinions on the rate trajectory.

- See PDF report for:

- MNI View

- Market Reaction

- MNI Instant Answers

- Press Conference Transcript

- FOMC Meeting Links

- Policy Statement Changes

- MNI Policy - Fed Watch