MNI Fed Preview - December 2025: Winter Of Discontent

Dec-08 2025 22:40By: Tim Cooper and 1 more...

US

Hidden PDF

- The FOMC is expected to look through the data fog and deliver a “hawkish cut” on December 10, with a third consecutive 25bp reduction in the Fed funds rate range to 3.50-3.75%.

- While a December cut is over 90% priced, a follow-up cut in January is seen as having under 30% probability, and the next easing is only fully priced by next June.

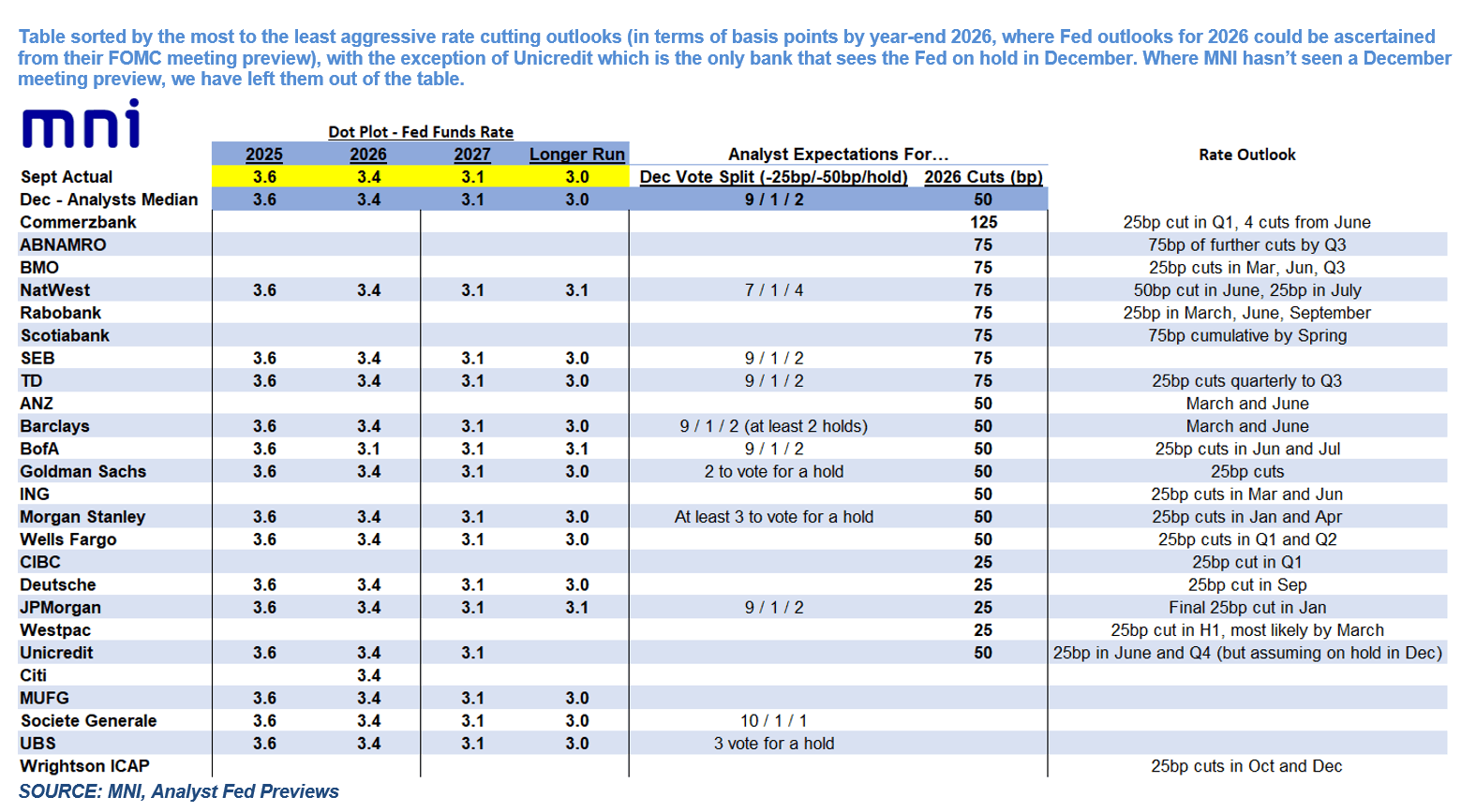

- There will be the usual attention on the Summary of Economic Projections including the Dot Plot, but more attention than usual on the Statement to see how resolutely the easing bias remains.

- Forward guidance is likely to be amended to reflect a more patient stance on cuts. As such the market reaction to the meeting could hinge on how Chair Powell portrays the burden of proof for the next cut.

- Powell will highlight that the Committee is increasingly reluctant to ease further without additional evidence of labor market deterioration. But by the same token, he could express that’s not an insurmountable obstacle, and a follow-up easing is possible in the event of incoming data before end-January.

- The lack of major data since the September projections round portends only limited changes to the macro and rate forecasts. None of the end-year rate dot medians are likely to change, implying 25bp cuts in each of 2026 and 2027.