MNI Eurozone Inflation Preview – June 2025

Jun-26 13:22By: Moritz Arold and 1 more...

Inflation+ 1

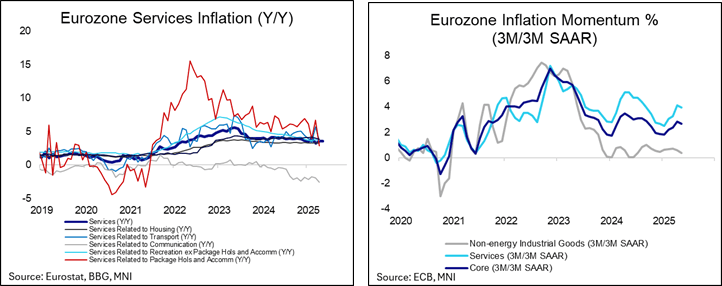

Focus Still On Services Despite Energy Volatility

DOWNLOAD FULL REPORT HERE: Jun2025EZCPIPreview_2.pdf

- The June Eurozone inflation round is split across two weeks, with France and Spain to kick off proceedings on Friday, followed by Italy and Germany on Monday. The Eurozone-wide release is due on Tuesday (alongside the Netherlands). Focus across the region will be on services, with the May 0.8pp disinflation on the Y/Y rate heavily impacted by volatile Easter-timing sensitive categories such as airfares.

- The ECB projected Q2 headline inflation at 2.0% in its latest projections. June flash headline HICP would need to print at 1.9% Y/Y for this to be realised – MNI consensus stands marginally higher, at 2.0%. For core, a 2.5% Y/Y print is required to meet the ECB's 2.5% Q2 projection (MNI consensus is for a lower 2.3% reading here), while 3.6% Y/Y would be required for services (ECB Q2 projection: 3.6%).

- While ECB officials have for now been happy to look through sub-2% headline inflation readings, a meaningful undershoot for core in Q2 and Q3 could see markets reprice the chance of a 1.50% terminal rate. ECB-dated OIS currently appear comfortably in pricing one more 25bp cut this cycle, for a 1.75% terminal.

- News flow since mid-June has until recently been dominated by the sharp escalation – and subsequent de-escalation – of tensions between Israel and Iran, driving notable swings in Brent crude and natural gas futures. These developments are expected to push up energy inflation on a sequential basis in June, but the annual rate is seen remaining in deflationary territory.