MNI Eurozone Inflation Insight: Services Beat, Travel At Play?

Nov-03 10:25By: Chris Harrison and 1 more...

European Central Bank+ 2

Download Full Report Here

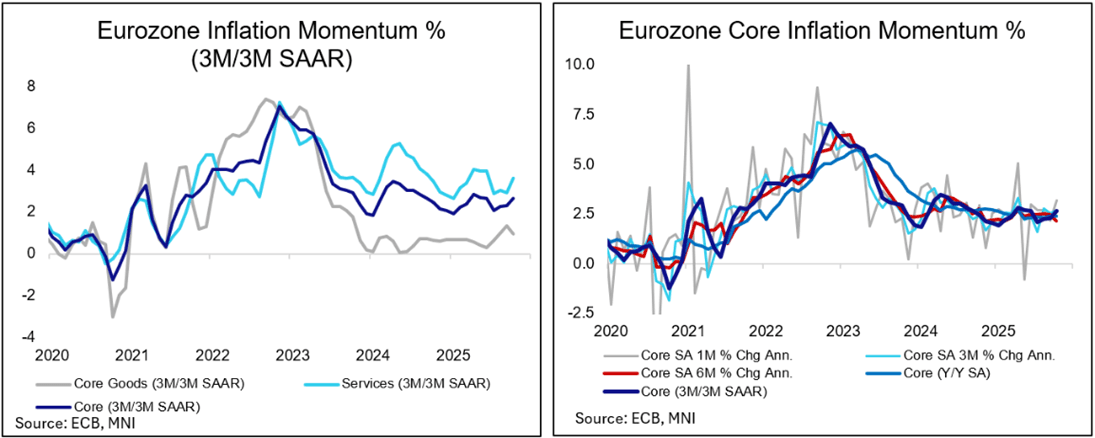

- Eurozone HICP inflation was as expected in the flash October release but core HICP surprised a little stronger with a Y/Y rate showing no moderation from September.

- Services inflation ticked higher although country-level data hint at volatile travel-related categories at play.

- The full October release on Nov 19 will provide a more useful update on exact drivers.

- By major country, Germany, Spain and Netherlands were all stronger than expected, France was in line and Italy saw a sizeable downside miss.

- The ECB is still seen being unlikely to cut at the next meeting in December (1-2bp priced) but with some sources warning that it could see more a lively discussion than some are expecting.