MNI Eurozone Inflation Insight – October 2024

Oct-31 16:41By: Emil Lundh and 2 more...

InflationEurozone

MNI (LONDON) - Lack Of Core Progress Fuels Hawkish ECB Repricing

PDF ANALYSIS HERE: Hidden PDF

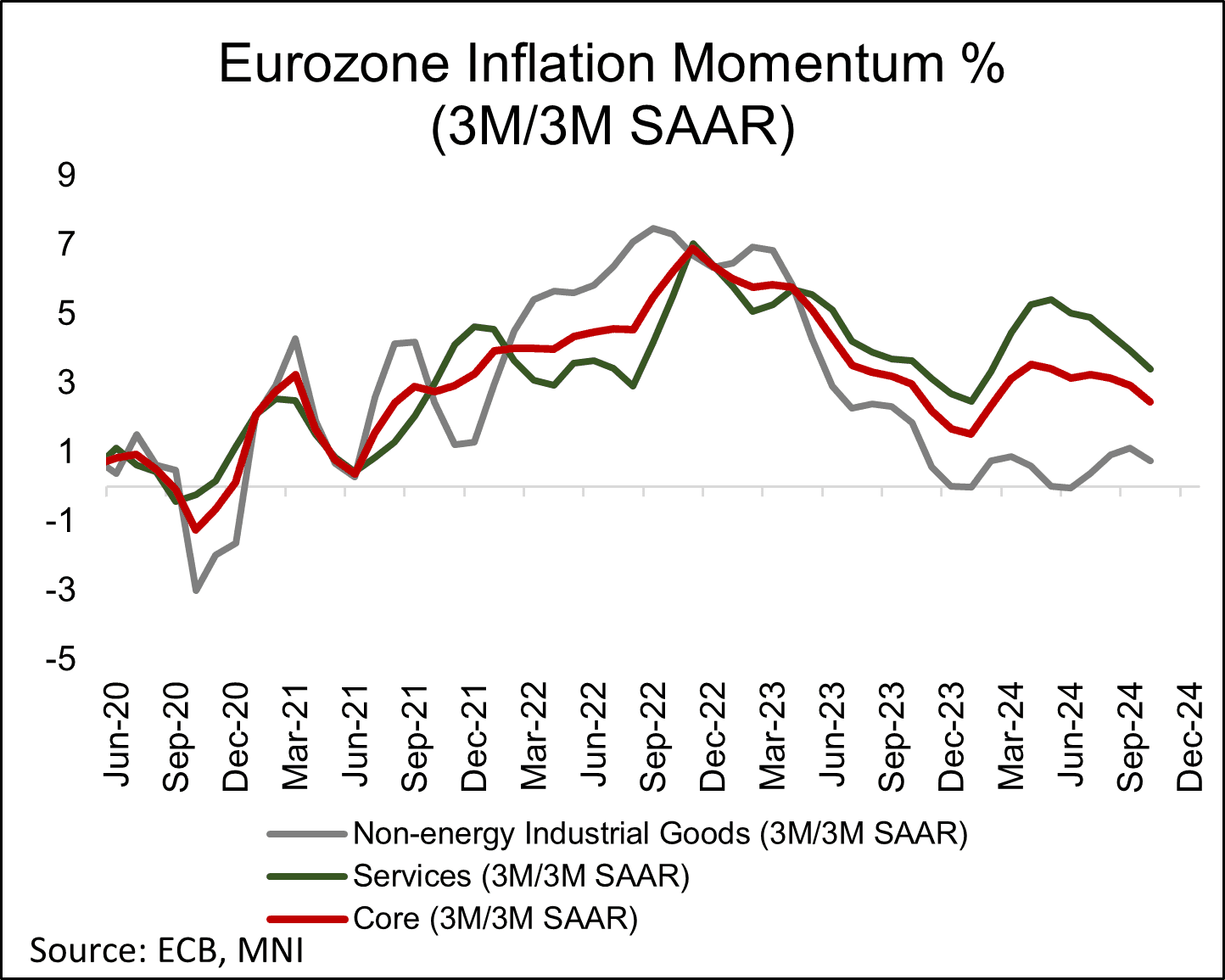

- The October Eurozone flash inflation round saw some reacceleration from cycle lows in September. While an uptick in headline inflation was expected on the back of energy base effects, core inflation also printed above expectations at 2.7% Y/Y (vs 2.6% cons, 2.7% prior).

- Taken alongside a stronger-than-expected Q3 EZ GDP print (0.4% Q/Q vs 0.2% expected by consensus and the ECB), this yielded a hawkish adjustment of ECB implied rates, with spillover from the UK autumn budget exacerbating the move.

- Of course, the ECB’s December macroeconomic projections will also take into account the November inflation round, leaving plenty of scope for further market repricing over the next 6 weeks.

Trending Top

Jun-26 16:22