MNI EUROPEAN OPEN: USD Weakness Extends

EXECUTIVE SUMMARY

- ZELENSKYY CAUTIOUSLY OPTIMISTIC ABOUT PEACES TALKS - DW

- JAPAN HAS ‘FREE HAND’ FOR BOLD ACTION IN FX MARKET - BBG

- CHINA COULD CUT RATES AS AS SOON AS IN Q1 2026 - SHANGHAI SEC. NEWS

- RBA BOARD DISCUSSED CONDITIONS IN WHICH RATE RISE MAY BE NEEDED - BBG

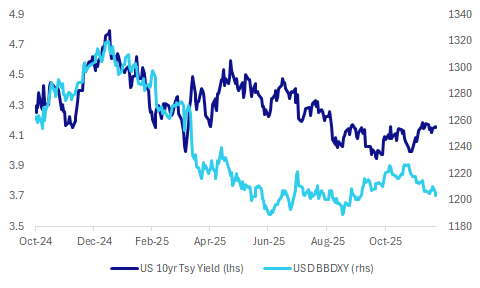

Fig 1: USD BBDXY Index & US 10yr Nominal Tsy Yield

Source: Bloomberg Finance L.P./MNI

UK

EU (TIMES): “Sir Keir Starmer will stick to his “red lines” of not rejoining a customs union with the EU, No 10 has said, despite Wes Streeting suggesting doing so would boost growth.”

TRADE (TIMES): “A survey from the British Chambers of Commerce (BCC) found 54 per cent of exporters say the trade and co-operation agreement with the EU has failed to help them increase sales in the UK’s largest market — a 13 percentage-point increase on last year.”

BUSINESS CONFIDENCE (BBG): “UK businesses ended 2025 feeling more upbeat about the economy’s prospects after they were spared much of the tax pain at last month’s budget.”

EU

RUSSIA (DW): “Kremlin spokesman Dmitry Peskov said the talks between representatives from Russia and the US in Miami on a possible peace deal to end the war in Ukraine is a "working process" rather than a turning point.”

UKRAINE (DW): “Ukraine's President Volodymyr Zelenskyy said the negotiations between his country and the US over a peace deal with Russia look "quite solid at this stage." While admitting no side is likely to get all of its demands, Zelenskyy said many parts of the US proposals are in line with his country's demands.”

UKRAINE (BBC): “Ukrainian Deputy Prime Minister Oleksiy Kuleba said Moscow was carrying out "systematic" attacks on the region. Last week, he warned that the focus of the war "may have shifted towards Odesa". President Volodymyr Zelensky said the repeated attacks were an attempt by Moscow to block Ukraine's access to maritime logistics.”

US

UKRAINE (POLITICO): ““We’re going to keep on trying to negotiate. And I think that we’ve made progress, but sitting here today, I wouldn’t say with confidence that we’re going to get to a peaceful resolution,” vice president Vance said in an UnHerd interview published Monday.”

VENEZUELA (BBG): “President Donald Trump warned President Nicolas Maduro not to challenge the US and vowed to keep oil seized from a supertanker but declined to say if he’s seeking to oust the Venezuelan leader.”

MIDDLE EAST (BBG): “ The US and its allies are renewing their push to hold a conference on Gaza reconstruction, people familiar with the matter said, as the Trump administration looks to inject fresh momentum into a ceasefire between Israel and Hamas after a string of setbacks.”

JAPAN

FX (BBG): “Japan has a “free hand” to take bold action against currency moves that are not in line with fundamentals, Finance Minister Satsuki Katayama said, in her strongest warning yet to speculators following the yen’s weakening even after a rise in interest rates.”

OTHER

AUSTRALIA (BBG): “ Australia’s central bank board discussed the circumstances under which it would have to pivot to interest-rate hikes in 2026 as inflation risks shift to the upside, while reiterating that any future moves will hinge on economic data, minutes of its Dec. 8-9 meeting showed.”

CHINA

RRR (SHANGHAI SECURITIES NEWS): “China could start a new round of cuts to interest rates and the amount of cash banks must keep in reserve in the first quarter of next year, the Shanghai Securities News reports, citing an analyst.”

MNI: PBOC Net Drains CNY76 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY59.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY76 billion after offsetting maturities of CNY135.3 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.3807% at 09:35 am local time from the close of 1.4337% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Monday, compared with the close of 48 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0523 Mon; +3.71% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0523 on Tuesday, compared with 7.0572 set on Monday. The fixing was estimated at 7.0296 by Bloomberg survey today.

MARKET DATA

SOUTH KOREA NOV RETAIL SALES +4.2% Y/Y; OCT. +6.7%

SOUTH KOREA NOV DEPARTMENT STORE SALES +12.3% Y/Y; OCT. +12.2%

MARKETS

US TSYS: Yields Grind Lower, TYH6 Nears Key Tech Level

US Bond futures have ground higher today in very light volumes during the Asia trading day. The 10-Yr is up +02+ at 112-13+ , near to the 100-day EMA of 112-14+. Downside resistance remains at the 200-day EMA of 111-31.

Cash was better with yields up to -1.5bps lower, with the long end outperforming.

- The 2-Yr is flat at 3.509%

- The 5-Yr is down -0.7bps at 3.708%

- The 10-yr is down -1.2bps at 4.155%

- The 30-Yr is down -1.4bps at 4.824%

Tonight markets turn their attention to a US$75bn 6-week and US$50bn 52-week bill auction and a US$28bn 2-Yr FRN reopening and a US$70bn 5-Yr auction.

For the U.S. Q3 2025 GDP release scheduled for tonight expectations are for continued solid growth, albeit at a slightly slower pace than the previous quarter. Markets generally expect real GDP to increase at an annualized rate of 3.3% for the third quarter. However as an alternate indicator the Federal Reserve Bank of Atlanta FED GDPNOW tracker is slightly more optimistic, providing a nowcast of 3.5% as of mid-December. Tonight's release is unique because the standard "Advance Estimate" usually due in October was cancelled due to a federal government shutdown; tonight's report serves as the first official consolidated print for the quarter.

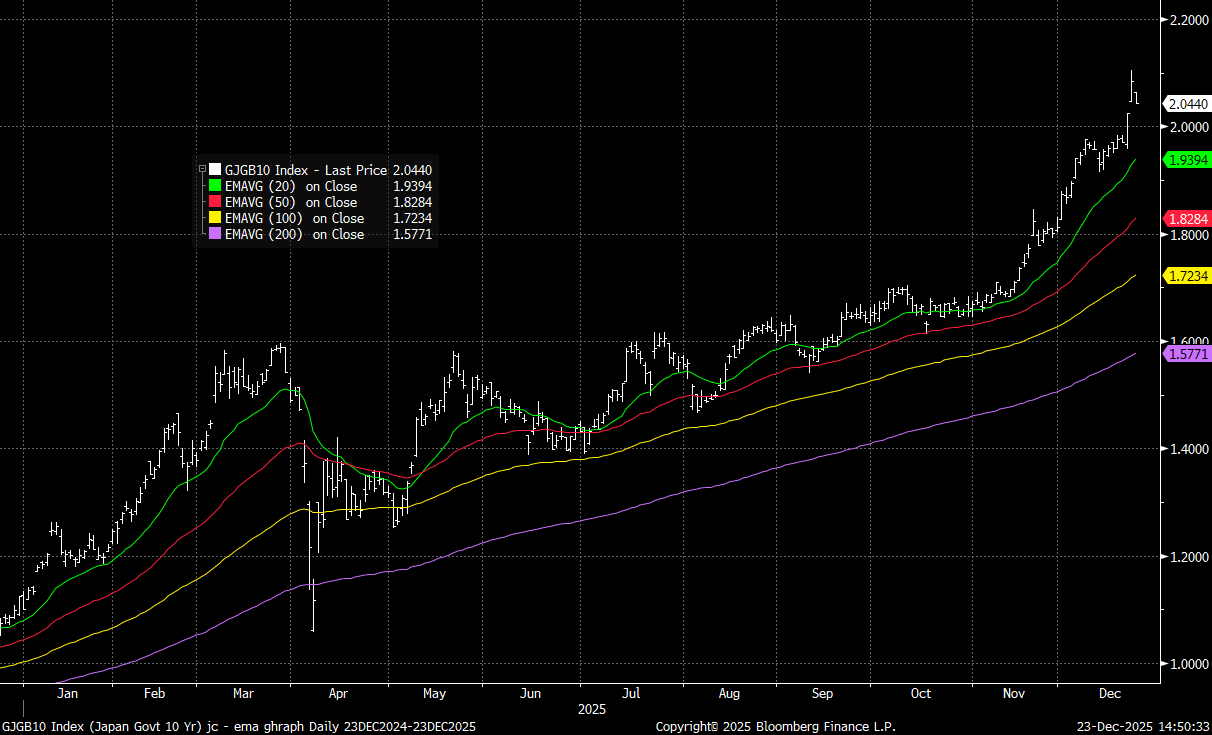

JGBS: Yields Lower, 10yr Still Above 2.0%, Takaichi Vows Responsible Fiscal Pol

JGB futures continue to recover from recent lows, last 132.85, +.45 versus settlement levels. US Tsy futures have also drifted a little higher in the first part of Tuesday. For JGB futures, this looks to be a correction from oversold conditions, with broader bearish risks still intact.

- It has been a similar backdrop for JGB outright yields, we sit around 2-4.5bps lower across most parts of the curve, led by 5-+10yr tenors. The 10yr was last around 2.04%, but remains above all key EMAs in yield terms, see the chart below. The nearest support point is back around 1.94% (per the 20-day EMA).

- USD/JPY weakness has likely helped yields retrace lower at the margins, with the pair testing under 156.00 amid increased FX rhetoric from the Japan FinMin around the intervention risk.

- Headlines have also crossed this afternoon: "JAPAN PM TAKAICHI IN NIKKEI INTERVIEW: "RESPONSIBLE PROACTIVE FISCAL POLICY" DOES NOT MEAN IRRESPONSIBLE BOND ISSUANCE OR TAX CUTS - [RTRS]"

- BoJ hike odds are around flat for both the Jan and March meetings 2026, per market OIS pricing.

- Tomorrow on the data front we get the PPI services for Nov along with the final Oct reads for the leading and coincident indices. Still due later today is Nov final machine tool orders.

Fig 1: JGB 10yr Yield Versus Key EMAs

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: ACGB Yields 3-4bps Lower, RBA Cautious On Outlook

Aussie bond futures have held a positive bias in Tuesday trade consistent with gains in US Tsy futures and JGBs, while at the same time the RBA Minutes, from the Dec policy meeting, didn't contain any hawkish surprises. Front end, 3yr futures (YM) are marginally outperforming, up +4bps to 95.795, although we are slightly down from best levels. 10yr futures (XM) are +3.5bps to 95.185. ACGB yields are around 3-4bps lower, with the front end marginally leading in yield terms.

- The RBA Minutes noted that the Board felt it needed more time to assess data to determine how persistent the pickup in inflation is. It was "too early" to know especially given the newness of the monthly CPI. It noted the upside risks to Q4 inflation and the "circumstances" that would drive a hike were also discussed. However, it noted a number of times that it was appropriate to be "cautious".

- Elsewhere, the December Bloomberg survey showed a median upward revision to consensus cash rate forecasts in 2026 as well as H1 GDP growth driven by stronger investment. A lot of forecasters have taken out easing expectations from their projections with some adding tightening.

- RBA tightening expectations are little changed for the Feb 2026 meeting, with market implied pricing giving around a 35% probability to a hike.

- The ACGB 10yr has backed away from a test 4.80% for now. A clean break higher could see the 5% handle targeted, while dips under 4.70% have been supported so far in Dec. For the 3yr upside focus rests around 4.20%.

- The AU-US10yr spread is slightly flatter at +61bps, but remains close to recent highs and continues to reflect risks around the 2026 central bank outlook between the Fed and RBA.

BONDS: NZGBS: Yields Mixed, 2/10s Curve Off Highs, NZ-US 10yr At +30bps

NZGB yields are mixed, with the 2yr higher, +2bps to 2.72%, while the rest of the curve is weaker in yield terms (down around 1.5-1.8bps). The 10yr is back to 4.44%. The back end moves are consistent with regional/US Tsy yield trends, so far in Tuesday trade and reverses some of yesterday's solid yield gains. Local news flow has been light, with markets winding down ahead of the Christmas/NY break.

- Broader ranges are holding for NZGBs, with some selling interest emerging when 10yr yields dip under the 4.40% region. For the 2yr we have edged up from a test of Dec lows under 2.70%. The 2/10s curve is slightly flatter at +172bps, but has been in a strong uptrend since the start of Dec.

- The 2yr swap rate (NDSO) is firmer, last around 2.76%, bouncing off 20-day EMA support (near 2.70%), in recent sessions.

The NZ-US 10-yr spread is relatively steady around +30bps, little changed today, but up from around flat in Oct/Nov, which fits with the respective cen

tral bank outlooks (with the Fed seen more at risk of cutting in the first part of 2026 compared to the RBNZ).

FOREX: USD - BBDXY Extends Lower Pressing 1203-1204 Support

The BBDXY has had a range today of 1203.09 - 1205.35 in the Asia-Pac session; it is currently trading around {BBDXY Index}. The USD has slipped again in the Asian session following on from yesterday's price action. The move last week had more to do with the surge higher in USD/JPY than any real USD strength as the moves elsewhere in currencies and more importantly in metals attest to. Robin Brook made an important point on Friday, take out the JPY in the USD basket and the USD is falling a lot more than is being appreciated. On the day, I suspect rallies to be faded while the 1210 area holds. First sell-zone is between 1207-1209, can this 1203-1204 area continue to provide support if not a move below here would target 1198-1200.

- EUR/USD - Asian range 1.1755-1.1781, Asia is currently trading {EURUSD Curncy}. The pair broke above the overnight highs in Asia and has extended. On the day, support is back toward 1.1730-1750 initially, as the market tries to build some momentum to test higher into the year-end.

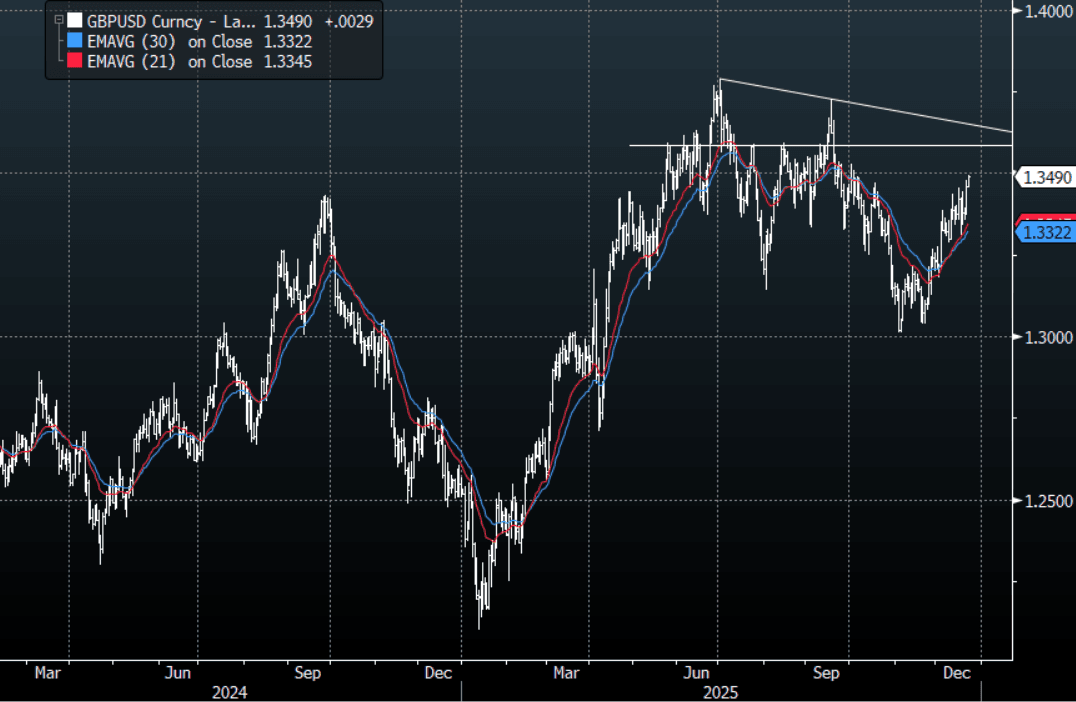

- GBP/USD - Asian range 1.3456-1.3493, Asia is currently dealing around {GBPUSD Curncy}. The pair has regained its upward momentum pushing up to test toward the 1.3500 area. On the day, I look for dips back toward 1.3400-1.3430 to now be supported initially. My skew toward looking for signs to short have not been well founded as of yet.

- Cross asset : SPX +0.02%, Gold $4485, US 10-Year 4.155%, BBDXY 1203, Crude Oil $57.94

- Data/Events : Spain GDP/PPI, Germany Import Price Index

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

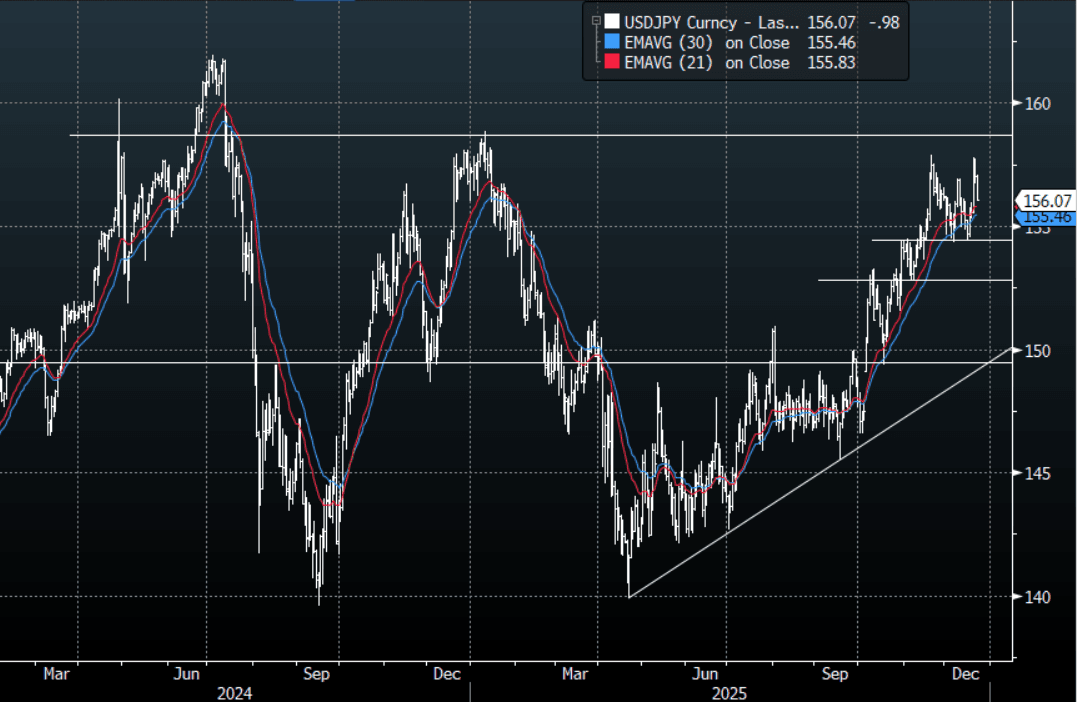

JPY: USD/JPY - Further Jaw-Boning Drags It Lower, Is That All It Takes ?

The USD/JPY range today has been 155.96 - 157.08 in the Asia-Pac session, it is currently trading around {USDJPY Curncy}. USD/JPY has had another leg lower as officials continue jaw-boning about the one-sided nature of the move. The BOJ is in a tough spot, and they are going to need to do something significant to turn around the market's perception of a weak Yen. The minimal reduction in differentials is not incentivising a market that is concerned about Japan’s Fiscal policy to start buying Yen. A test of the BOJ/MOF resolve looks inevitable at the moment as the market turns its focus toward the important 160.00 area. Technically USD/JPY remains in an uptrend, while the first support back toward the 152.50-154.50 area is intact it remains a buy on dips. On the day, we have pulled back nicely, but I suspect buyers are looking to fade this move initially. First support is around 155.80-156.00 and then the more important 154.50-155.50 area.

- "KATAYAMA: DECLINE TO COMMENT ON CURRENT FX, YIELD LEVELS. THERE ARE MANY FACTORS BEHIND FX, YIELDS MOVES. SEE SOME FX MOVES NOT IN LINE WITH FUNDAMENTALS" - BBG

- "JAPAN FINMIN KATAYAMA: WILL TAKE APPROPRIATE ACTION AGAINST EXCESSIVE MOVES, JAPAN HAS A FREE HAND IN DEALING WITH EXCESSIVE MOVES IN THE YEN - [RTRS]

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.00($1.32b), 158.00($968m). Upcoming Close Strikes : 155.50($486m Dec 26), 157.00($889m Dec 24), 158.00($589m Dec 24) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 118 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

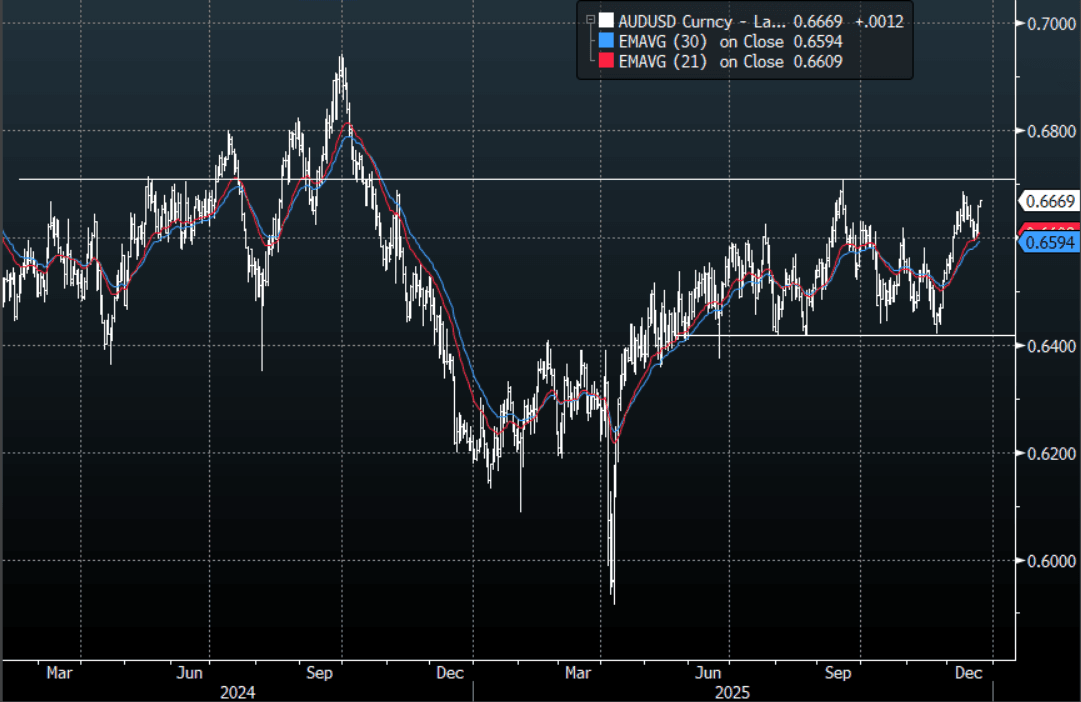

AUD/USD - Extends Above 0.6650 In Asia

The AUD/USD has had a range today of 0.6655 - 0.6670 in the Asia- Pac session, it is currently trading around {AUDUSD Curncy}. The AUD continues to grind higher in Asia building on yesterday's gains with very little pullback as risk looks likely to resume the Santa rally. The AUD price action for the moment remains constructive as the pair looks to build the momentum to retest the 0.6700 area. Technically while the AUD remains above 0.6500-0.6550 dips should continue to be supported. On the day, I suspect dips back toward 0.6620-40 will now be supported as the market turns its focus back toward 0.6700.

- MNI AU -RBA: Board “Cautious”, Inflation Persistence & Excess Demand Could Drive Hike. Rates were unchanged in December as the Board felt it needed more time to assess data to determine how persistent the pickup in inflation is. It was “too early” to know, especially given the newness of the monthly CPI. It did note that the October reading increased the risks that Q4 could exceed its projections, as well as price measures in the Q3 national accounts. Importantly, the “circumstances” that would drive a hike were discussed. However, it noted a number of times that it was appropriate to be “cautious”.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6535(AUD428m), 0.6600(AUD557m). Upcoming Close Strikes : none - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

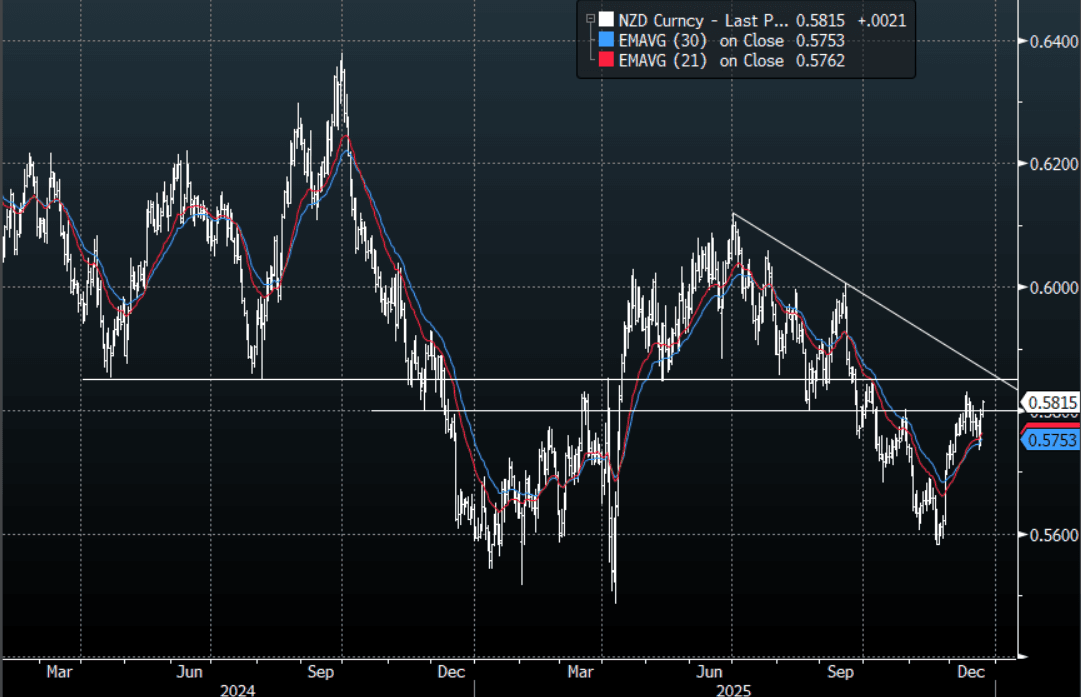

NZD/USD - Pushed Back Above 0.5800 In Asia

The NZD/USD had a range today of 0.5788-0.5817 in the Asia-Pac session, it is currently trading around {NZD Curncy}. The NZD built on the strength seen overnight and pushed back above 0.5800 challenging the top of its recent range. The NZD is holding above 0.5700-0.5750 and for the most part was left unscathed by the choppy price action seen elsewhere last week, as risk looks to build onto the Santa rally I suspect the NZD could probe back above 0.5830. On the day, I suspect a pullback toward 0.5765-85 should find demand as the market looks to potentially challenge the 0.5810/30 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5530(NZD475m). Upcoming Close Strikes : None - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 44 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Stocks Extend Gains, AI / Tech Remain Focus

Asian equity markets are broadly higher today largely extending gains from the previous session driven by momentum from Wall Street and optimism around Artificial Intelligence (AI) related stocks as Tesla and Nvidia gained. Major indices in Japan, Korea and Hong Kong advanced whilst China's indices were more muted. Ahead of the advanced US GDP report, a report in the Shanghai Securities news citing the Chief Macro Analyst from Golden Credit Rating suggests that cuts to rates and RRR's will come in Q1 2026 in China, boosting sentiment. China's embattled property developer China Vanke appears to have won a last minute reprieve from creditors to extend the grace period for a bond due to Jan 28, whilst the proposal to defer principal payment for 12 months was unsuccessful.

- The NIKKEI has done very little today, hovering around 50,374 where it opened. Yesterday's gains took the NIKKEI back above all major moving averages.

- The KOSPI is up +0.43% to 4,123 as it too consolidates above all major moving averages.

- China's major bourses were all up modestly today with the CSI 300 leading gains. Up +0.50% at 4,635, the CSI 300 has consolidated above all major moving averages.

- India's NIFTY 50 failed to capitalize on yesterday's gains of +0.79% and is down -0.10% today and at 26,147 is near to the November high of 26,215.

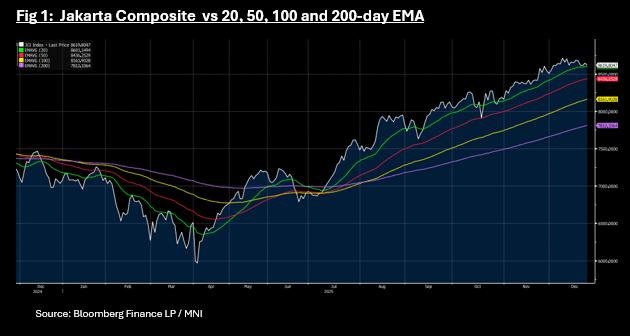

- Both the Jakarta Composite and the FTSE Malay KLCI are down modestly today. The JCI is down -0.30% at 8,621 and is near to the 20-day EMA 8,600, having last traded below it in October.

OIL: Uncertainty Over Venezuela & Russia Putting Floor Under Oil Prices

Crude is slightly lower during Tuesday’s APAC trading but holding onto the previous days’ gains as geopolitical risks rose in oil producing regions. Prices have moved today in a very narrow range of around 20c with Brent around $61.92/62.08 and currently down 0.1% to $62.01/bbl and WTI between $57.79/57.99 and now 0.2% lower at $57.92/bbl.

- Tensions between the US and Venezuela have boosted oil markets at a time when the focus is on excess supply. The US has boarded two shadow fleet vessels and is seeking a third. President Trump said that the US will capture it and that it would be “smart” for Venezuela’s Maduro to leave power. He also suggested land attacks are possible. The US will keep the tankers and crude but despite this Venezuelan oil continues to be loaded.

- Ukraine’s escalation of attacks on Russian energy infrastructure is adding to geopolitical worries. The closure of Kazakhstan’s main export dock on the Black Sea following a Ukrainian strike at the end of November is ongoing.

- A record market surplus in 2026 has been forecast for some time and the additional production is expected to show up in rising inventories but they may also increase due to global uncertainties. Later on Tuesday US industry-based stock data print with the official EIA out on Wednesday.

- Later US 6 December ADP employment, Q3 GDP, October orders, December Philly & Richmond Fed indices, December Conference Board consumer confidence and Oct/Nov IP/capacity utilisation, as well as Q3 Spanish GDP, Canadian October GDP and BoC summary of deliberations are released.

PRECIOUS METALS: $70 Providing Resistance For Silver

Gold and silver are off new record highs reached today but remain higher than Monday’s closing levels supported by a softer US dollar (BBDXY -0.2%), slightly lower US yields, Fed easing expectations and safe-haven flows due to a rise in geopolitical tensions. Gold reached $4497.74/oz earlier and is now up 1.0% to $4487.0.

- Bullion broke above resistance at $4493.7, a Fibonacci projection, but was unable to hold it. The trend remains bullish.

- Silver is 0.9% higher at $69.66 after rising to $69.993, above resistance at $69.687. It is yet to pierce psychological resistance at $70.00. Moving average studies continue to highlight a dominant medium-term uptrend.

- Geopolitical concerns have risen with increased tensions between the US and Venezuela as the former blockades tankers. Ukrainian attacks on Russian energy infrastructure including an empty vessel in the Mediterranean have added to worries. There are also strains between China and Japan.

- President Trump said that the US will capture the third tanker it is chasing and that it would be “smart” for Venezuela’s Maduro to leave power. The US will keep the tankers and crude that it has seized despite this Venezuelan oil continues to be loaded.

- Equities are generally stronger with the CSI 500 up 0.5% and TAIEX +0.5% but S&P e-mini and Nikkei flat. Oil prices slightly lower with WTI -0.1% to $57.94/bbl. Copper is down 0.1%.

- Later US 6 December ADP employment, Q3 GDP, October orders, December Philly & Richmond Fed indices, December Conference Board consumer confidence and Oct/Nov IP/capacity utilisation, as well as Q3 Spanish GDP, Canadian October GDP and BoC summary of deliberations are released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/12/2025 | 0700/0800 | ** | PPI | |

| 23/12/2025 | 0700/0800 | ** | Import/Export Prices | |

| 23/12/2025 | 0800/0900 | ** | PPI | |

| 23/12/2025 | 0800/0900 | *** | GDP (f) | |

| 23/12/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 23/12/2025 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 23/12/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/12/2025 | 1330/0830 | *** | GDP / PCE Quarterly | |

| 23/12/2025 | 1330/0830 | *** | GDP / PCE Quarterly | |

| 23/12/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 23/12/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 23/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 23/12/2025 | 1415/0915 | *** | Industrial Production | |

| 23/12/2025 | 1500/1000 | ** | Richmond Fed Survey | |

| 23/12/2025 | 1500/1000 | *** | Conference Board Consumer Confidence | |

| 23/12/2025 | 1630/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 23/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 23/12/2025 | 1800/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 23/12/2025 | 1830/1330 | Bank of Canada meeting minutes | ||

| 24/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 24/12/2025 | 1330/0830 | *** | Jobless Claims |