MNI EUROPEAN OPEN: USD Holds Monday Gains

EXECUTIVE SUMMARY

- LUTNICK SEES LIKELY 90-DAY EXTENSION OF CHINA TRADE TRUCE - BBG

- TRUMP RAISES PRESSURE ON PUTIN WITH NEW 10-12 DAY TRUCE DEADLINE- BBG

- US BOOSTS Q3 BORROWING $453B TO $1.007T; Q4 $590B - MNI BRIEF

- EU STATES BROADLY BACK EU-U.S. DEAL - OFFICIALS - MNI

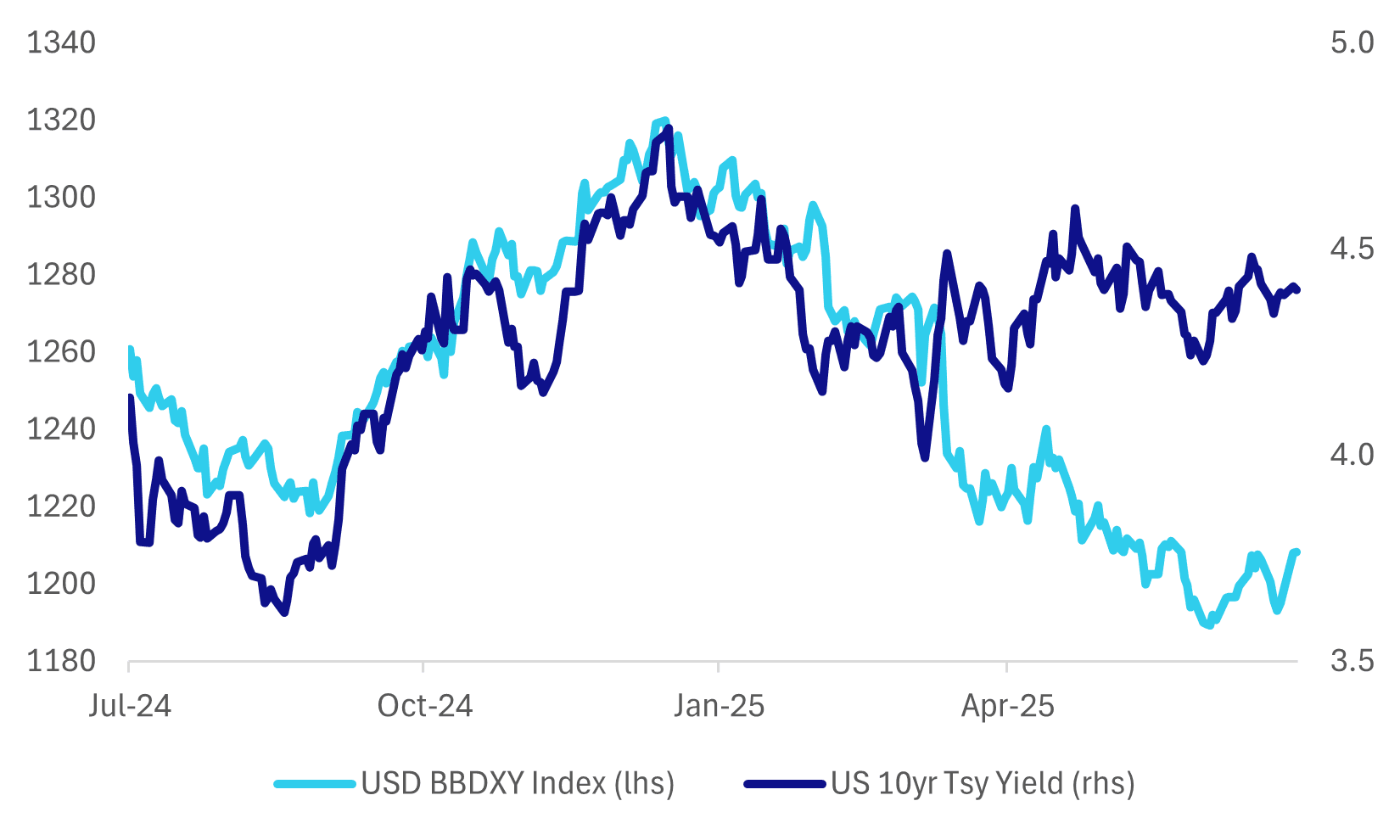

Fig 1: USD BBDXY index & US Tsy 10yr Yield

Source: Bloomberg Finance L.P./MNI

EU

RUSSIA (BBG): "President Donald Trump said he would shorten his timeline for Russian leader Vladimir Putin to reach a truce with Ukraine or face potential economic penalties, heightening pressure on Moscow to bring the fighting to a halt."

TRADE (MNI): European states broadly accepted the terms of the weekend’s EU-U.S. trade deal, officials told MNI on Monday following a meeting between diplomats and the European Commission earlier today. France was alone in describing the deal as a "surrender,” saying a tougher negotiating style by the Commission earlier on could have proved more effective.

ISRAEL (POLITICO): “The European Commission wants to partially suspend Israel from participating in its flagship research and development program, Horizon Europe. Israel's military activities in Gaza could endanger its participation in the €95-billion scheme, which it joined in 2021 as an associate country, the closest form of research cooperation for non-EU countries.”

US

US/CHINA (RTRS): "Top U.S. and Chinese economic officials met in Stockholm on Monday for more than five hours of talks aimed at resolving longstanding economic disputes at the centre of a trade war between the world's top two economies, seeking to extend a truce by three months."

US/CHINA (BBG): "Commerce Secretary Howard Lutnick said a 90-day extension of a trade truce with China was a likely outcome with negotiations between the two countries underway in Stockholm."

FISCAL (MNI BRIEF): The U.S. Treasury on Monday increased its estimate for federal borrowing for the current quarter by USD453 billion, while reiterating its previous assumption for an USD850 billion cash balance at the end of September.

OTHER

JAPAN (BBG): " Japan’s ruling party will likely debate the fate of beleaguered Prime Minister Shigeru Ishiba at a gathering in the next few days amid rising calls for a leadership change."

SOUTH KOREA (RTRS): "South Korean Finance Minister Koo Yun-cheol said on Tuesday he would seek a mutually beneficial trade deal when he meets U.S. Treasury Secretary Scott Bessent for talks this week, just days before an August 1 deadline expires to avoid punishing tariffs."

CHINA

POLICY (SHANGHAI SECURITIES NEWS): "China’s government is focusing on expanding domestic demand, curbing excessive market competition and stabilizing the property and equity markets in the second half of 2025, as outlined in recent official meetings, Shanghai Securities News says in a report."

SUBSIDY (YICAI): "China’s new child care subsidy of CNY3,600 per child, up to the age of three, will require CNY101.2 billion annually, based on latest official data, Yicai.com has calculated."

CONSUMPTION (YICAI): "China is expected to boost consumption further by removing unreasonable restrictions, optimising the consumer goods trade-in programme and diversifying supply, Yicai.com reported. The trade-in scheme should be further expanded to cover service consumption, including tourism and catering in the second half of the year, said Xiao Lisheng, researcher at the Chinese Academy of Social Sciences."

PANDA BONDS (SECURITIES DAILY): "China’s panda-bond market expanded rapidly in H1, driven by increased participation from foreign institutions, Securities Daily reported. "

MNI: PBOC Net Injects CNY234.4 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY449.2 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY234.4 billion after offsetting maturities of CNY214.8 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.5228% at 09:42 am local time from the close of 1.5806% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 45 on Monday, compared with the close of 46 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1511 Tues; +0.59% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1511 on Tuesday, compared with 7.1467 set on Monday. The fixing was estimated at 7.1909 by Bloomberg survey today.

MARKET DATA

UK JULY BRC SHOP PRICE INDEX +0.7% Y/Y; EST. +0.3%; JUNE +0.4%

MARKETS

US TSYS: Asia Wrap - Yields Drift Lower In A Quiet Session

The TYU5 range has been 110-25+ to 110-28+ during the Asia-Pacific session. It last changed hands at 110-27+, up 0-03 from the previous close.

- The US 2-year yield has shifted lower trading around 3.914%, down 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.402%, down 0.01 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, decent supply was seen around 4.30/35% first up. A decent bounce was seen off this support but the move has failed to follow through above 4.40% for now. The Data this week should hopefully provide more clarity going forward.

- Nick Timiraos on X: ”Fed officials expect they will need to resume lowering interest rates eventually—they just aren’t ready to do it this week. The questions dividing them center on what evidence they need to see first, and whether waiting for that clarity turns out to be a mistake.”

- “The Fed was united when officials paused cuts this year after tariffs raised fears of renewed inflation. But with tariff-related price hikes proving milder than feared and signs that hiring may be softening, officials are now fractured into three camps over whether to resume cuts.”

- “The focus will be whether Powell offers any hint of a September rate cut in his press conference Wednesday afternoon, and whether in the coming days and weeks his colleagues begin laying the groundwork for a cut at their next gathering.”

- Data/Events: Advanced Goods Trade Balance, FHFA House Price Index, S&P Corelogic, JOLTS, Conf. Board Consumer Confidence, Dallas Fed Services Activity.

JGBS: Modestly Richer, Strong 2Y Auction, BOJ Starts Two-Day Meeting Tomorrow

JGB futures are modestly stronger, +8 compared to the settlement levels.

- Today, the local calendar will be empty apart from 2-year supply.

- The 2-year bond auction showed strong results today. The low price printed stronger than the Bloomberg-surveyed forecast of 100.09, while the cover ratio increased to 4.4665x from 3.9028x. The auction tail also narrowed compared to last month.

- The Japan Times via BBG - "In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation. In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation."

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's modest sell-off. Wednesday's FOMC announcement is widely expected to be a steady rate outcome.

- Cash JGBs are 1-2bps richer apart from the 30-year which is 1bp cheaper. The benchmark 2-year yield is 1.5bps lower at 0.825% versus the cycle high of 0.890%.

- Swaps are mixed, with rates flat to 1bp lower.

- Tomorrow, the local calendar will be empty ahead of the BOJ Policy Decision on Thursday.

AUSSIE BONDS: The Wait Is Over, Q2 CPI Tomorrow Followed By FOMC

ACGBs (YM +1.5 & XM +1.0) are slightly stronger after a subdued data-light session.

- The focus of this week will be tomorrow's Q2 CPI data, which is expected to show the underlying trimmed mean measure making further progress towards the band midpoint of 2.5%. Bloomberg consensus is forecasting a 0.7% q/q rise, bringing the annual rate to 2.7% after 0.7% & 2.9% in Q1. This is slightly higher than the RBA's May Q2 forecast of 2.6%. Services developments will also be monitored. The RBA is expected to cut rates 25bp on August 12.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's modest sell-off. Wednesday's FOMC announcement is widely expected to be a steady rate outcome. It’s virtually unanimous that there will be two dissents in favour of a cut at this meeting, with Gov Waller widely expected to do so and Gov Bowman also likely (among analysts who expressed an opinion on this).

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at -8bps.

- The bills strip is slightly stronger, with pricing flat to +2.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in August is given an 89% probability, with a cumulative 59bps of easing priced by year-end.

- The AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Friday.

BONDS: NZGBS: Closed At Bests But Only Modestly Richer

NZGBs closed at session bests, 2bps richer across benchmarks.

- The NZ-US 10-year yield differential finished 3bps tighter at +15bps.

- Swap rates closed 2bps lower.

- RBNZ dated OIS pricing closed little changed across meetings. 21bps of easing is priced for August, with a cumulative 35bps by November 2025.

- The local calendar will feature the release of ANZ business confidence for July tomorrow. It continues to point to a gradual recovery in the economy. Cost and price components remain elevated, and inflation expectations are at 2.7% off their low.

- ANZ July consumer confidence is out on Friday. It rose sharply in June to 98.8, the highest this year, but still off December's 100.2. Rate cuts, which take time to be reflected in mortgage payments, have helped improve households' financial situations and reduced the time to buy component.

- June building permits will also be printed on Friday. They rose 10.4% m/m in May, and indicators suggest that the construction sector is recovering.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 4.50% May-30 bond and NZ$175mn of the 4.25% May-34 bond.

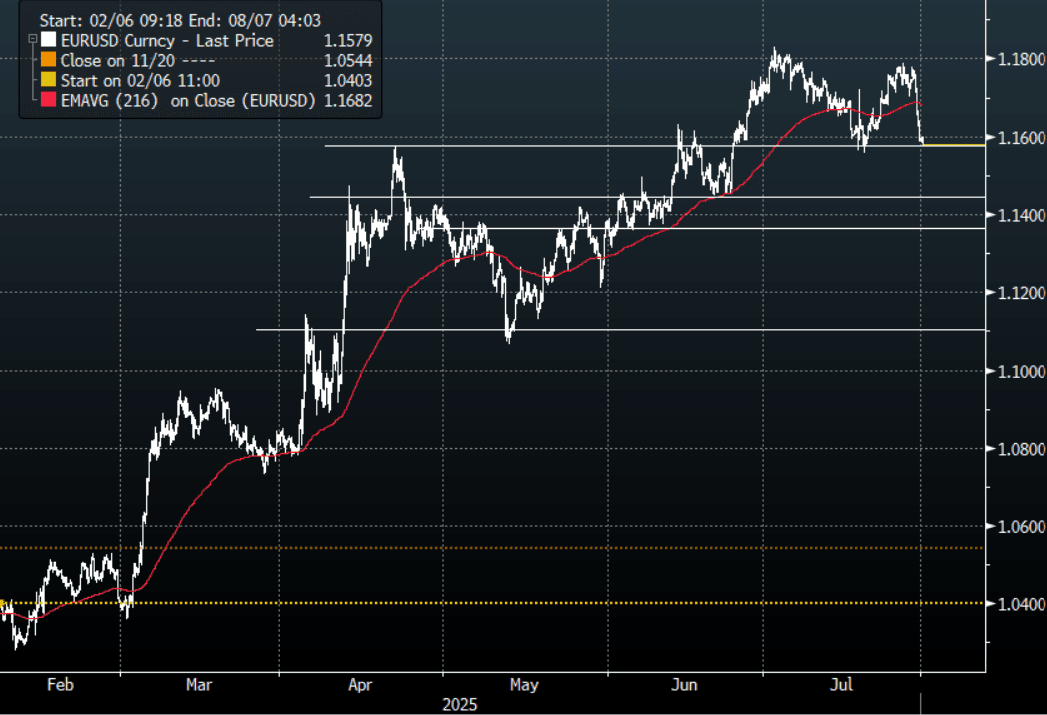

FOREX: Asia FX Wrap - The USD Correction Could Have More To Go

The BBDXY has had a range of 1207.45 - 1208.74 in the Asia-Pac session, it is currently trading around 1208, +0.05%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking was seen. Yesterday's US-EU trade deal was seen as a big loss for the European Union and this has provided the USD bounce with further tailwinds. There is lots of event risk coming up this week and we are heading into month-end so some caution is warranted, this could potentially see some more paring back of USD shorts. Today is corporate month-end and this could also add to some short-term USD demand putting further pressure on the shorts.

- EUR/USD - Asian range 1.1575 - 1.1599, Asia is currently trading 1.1580. The pair saw some heavy selling putting in a top towards 1.1800 for now. The price looked a little stretched in the short term, and with the USD making a recovery the EUR is set for a correction of sorts. First support around 1.1550 then the more important 1.1350/1.1450 area where I would expect demand first up.

- GBP/USD - Asian range 1.3337 - 1.3362, Asia is currently dealing around 1.3340. This pair looks like it is now breaking lower indicating a deeper correction. Support seen now back towards 1.3100/1.3200 and look for supply now on bounces back towards 1.3500.

- USD/CNH - Asian range 7.1775 - 7.1839, the USD/CNY fix printed 7.1511, Asia is currently dealing around 7.1800. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3311, US 10-Year 4.40%, BBDXY 1208, Crude oil $66.59

- Data/Events : Spain GDP & Retail Sales, EZ ECB 1&3 Year CPI Expectations, France Total Jobseekers

Fig 1: EUR/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

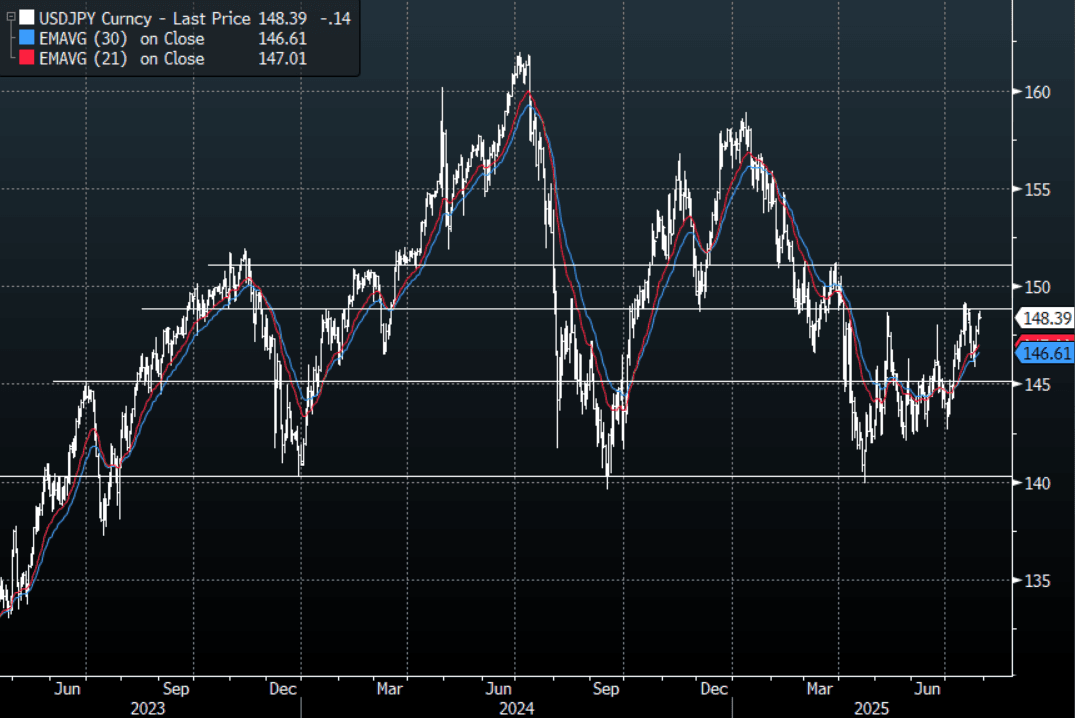

JPY: Asia Wrap - USD/JPY Consolidates On A 148 Handle, Eyes July Highs

The Asia-Pac USD/JPY range has been 148.29 - 148.71, Asia is currently trading around 148.45, -0.05%. USD/JPY continued to build on its momentum higher as the USD shorts reduce risk heading into an important week for risk. Corporate month-end today will add to the headwinds for the USD shorts. A move back above the highs for July would turn the focus towards the pivotal 151.00/152.00 area.

- The Japan Times via BBG - “In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation. In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation.”

- "X-BOJ DEPUTY GOVERNOR NAKASO: DOLLAR TO RETAIN SUPREMACY AS KEY GLOBAL CURRENCY BUT 'CRACKS' APPEARING AS INVESTORS DIVERSIFY INTO OTHER CURRENCIES. BOJ LIKELY TO RESUME INTEREST RATE HIKE IT RESTORES CONFIDENCE THAT ECONOMY, INFLATION WILL MOVE IN LINE WITH PROJECTIONS. BOJ MUST BE VIGILANT TO UPSIDE RISKS TO INFLATION AS RISING FOOD PRICES COULD LEAD TO OVERSHOOT IN INFLATION EXPECTATIONS" RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.65($823m).Upcoming Close Strikes : 149.00($1.16b July 30), 147.00($1.52b Aug 1), 146.00($1.43b Aug 1) - BBG.

- CFTC data shows Asset managers surprisingly added slightly to their JPY longs +72326( Last +71610), while leveraged funds have slightly reduced their newly built short JPY position -11571(Last -12606).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

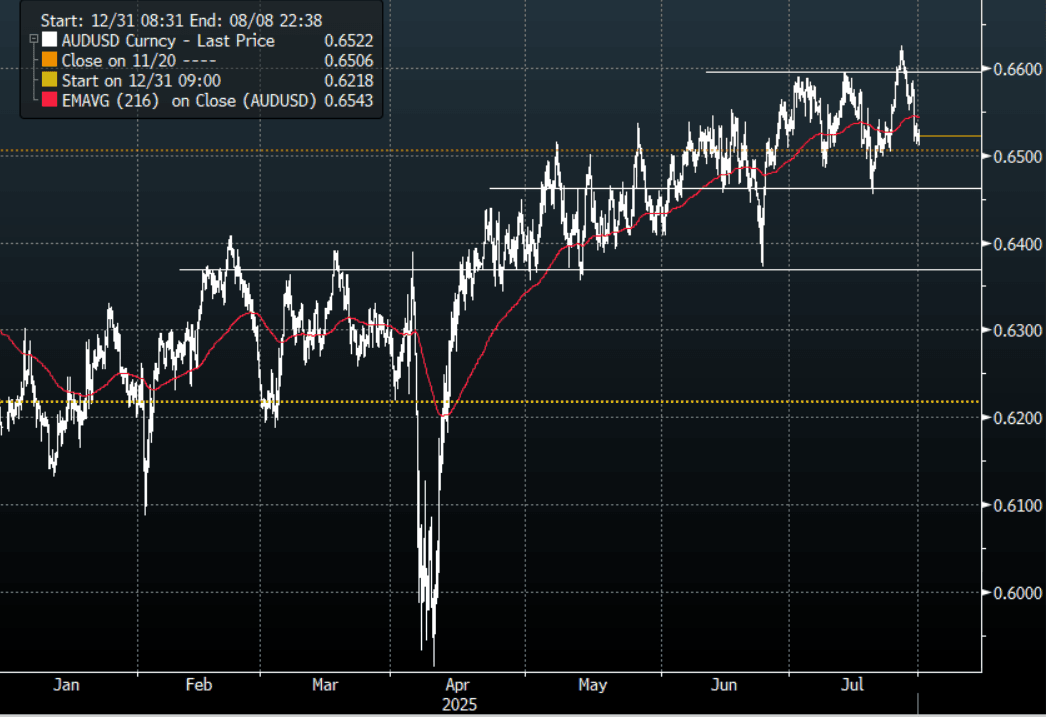

AUD: Asia Wrap - AUD/USD Trades Heavy, Looking Towards Q2 CPI Tomorrow

The AUD/USD has had a range of 0.6512 - 0.6530 in the Asia- Pac session, it is currently trading around 0.6520, -0.02%. The pair could not hold onto its early gains yesterday and slid lower as the USD bounced strongly across the board. The pair failed to gain any momentum above 0.6600 last week and now awaits a very busy calendar this week which could have meaningful implications for risk. Locally the Australian Q2 CPI tomorrow will be closely watched and could provide a catalyst for some movement. Worth keeping in mind it is corporate month-end today and this could see some further headwinds for USD shorts. First support around 0.6450 then the more important 0.6350 area.

- AUSTRALIA: Q2 Core Inflation Expected To Be 0.1pp Above RBA Forecast At 2.7%. Q2 CPI prints Wednesday and will be monitored closely given that the RBA relies on this series with the monthly version not yet complete (due to take place on November 26). Headline inflation continues to be distorted by federal & state government electricity rebates and so attention will remain on the underlying trimmed mean. The RBA’s May forecast was for 2.6% y/y and so a print close to this would likely result in an August cut but steady around Q1 may add doubt.

- CBA Warns Higher CPI Print Could Keep RBA Cautious. A 2.8% print could “be a somewhat awkward 0.2ppt above” the RBA’s latest forecast, but CBA would still expect a 25bp cut on August 12 but see the “decision as not as clear cut as current market pricing suggests”.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD968m), 0.6400(AUD323m). Upcoming Close Strikes : 0.6550(AUD1.01b July30), 0.6600(AUD1.38b July 31), 0.6465(AUD1.01b July31) - BBG

- CFTC Data shows Asset managers added a decent clip to their shorts -53959(Last -38267), the Leveraged community reduced their own shorts to -12010(Last -20048).

- AUD/JPY - Asia-Pac range 96.68 - 96.95, Asia is trading around 96.80. The pair could not hold above 97.00 yesterday. The support between 95.00 - 96.00 held very well last week and the pair is looking to regain its momentum for a move higher. The event-risk coming up this week could provide some short-term headwinds.

Fig 1: AUD/USD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

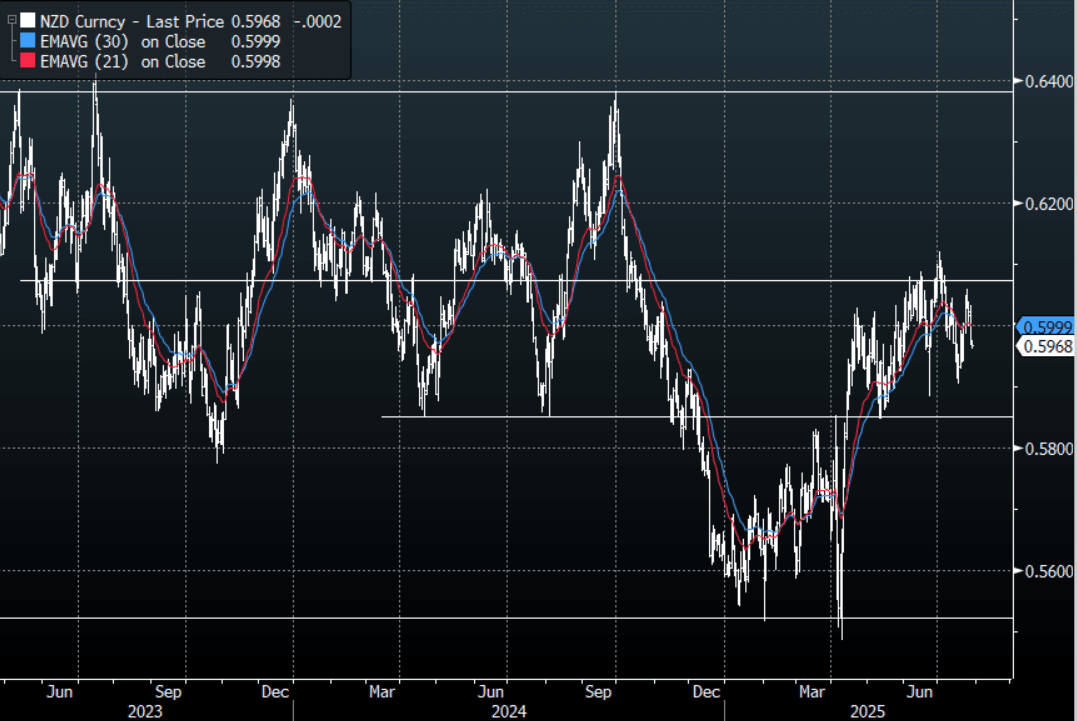

NZD: Asia Wrap - NZD/USD Fails Above 0.6000, Trades Heavy Into Month-End

The NZD/USD had a range of 0.5961 - 0.5976 in the Asia-Pac session, going into the London open trading around 0.5965, -0.08%. The pair could not hold onto its early gains yesterday and slid lower as the USD bounced strongly across the board. There is lots of event risk coming up this week and we are also heading into the corporate month-end today so there could be an extra demand for USD’s further pressuring the USD shorts. Support now seen back towards the 0.5850/0.5900 area.

- "NEW ZEALAND JUNE JOB ADS FALL 2.6% M/M: BNZ" - BBG

- "Job ads index fell 2.6% m/m following a revised 2% decline in May. Drops 2.8% y/y. After a year of relative stability, ads are again on a downwards trajectory: BNZ. “Consistent with the decline in job ads, we expect total employment fell modestly and the unemployment rate climbed to 5.3%” in 2q.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6000(NZD395m July 30), 0.5965(NZD424m July 31). - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +5034(Last +8192), the Leveraged community added slightly to their shorts last week -7328(Last -6744).

- AUD/NZD range for the session has been 1.0912 - 1.0930, currently trading 1.0928. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Sentiment Mostly Weaker Ahead Of Key Event Risks

Most regional Asia Pac markets are down in the first part of Tuesday trade. Losses aren't large, but outside of South Korea and Malaysia, trends are negative throughout the region. This follows and overnight session where US markets modestly outperformed EU weakness. So far today, US equity futures are modestly higher, with Nasdaq futures slightly outperforming. This comes ahead of month end late this week.

- Earlier remarks from US Commerce Secretary Lutnick stated that Trump is considering a few deals before the Aug 1 deadline, he will then decide on the unilateral tariff rate. Lutnick stated that an extension of trade truce was likely in terms of the current meetings under with China officials. Trump also pushed back on the idea he was pursuing a summit with China President Xi.

- The China CSI 300 is off a touch, but still close to recent highs. The HSI is down around 1%, but still above the 25300 level. Japan markets are also weaker, the Topix off close to 0.85%. Proximity to earnings outcomes and the Fed decision/data is being cited as a headwind for these markets.

- Taiwan's Taiex is down around 0.85% as well, after a strong run higher in recent weeks. The Kospi is bucking these trends, up nearly 0.60% and firmly above the 3200 level. Earlier we had headlines of corporate tax increases and changes to the capital gains tax, but these shifts have been flagged in the local media prior to today, which may be limiting the market impact.

- In South East Asia, most markets are down, except for Malaysia. Losses are modest though at this stage. Thailand markets have returned, unable to build on recent positive momentum. Thailand has accused Cambodia of violating the recent ceasefire agreement, while a meeting between the countries respective militaries has been postponed.

OIL: Crude Holds Gains As Uncertainty Rises Over US Action Against Russia

Oil has held onto most of Monday’s gains. It has trended gradually lower through the APAC session though with WTI now down 0.1% to $66.64/bbl, close to the intraday low, after reaching $67.09 early in trading. Brent is 0.1% lower at $69.96/bbl after a high of $70.28. They rose around 2.8% yesterday following US President Trump saying he will bring forward the deadline for an end to hostilities in Ukraine. If effective, the measures he has proposed against Russia, including on purchasers of its crude, could impact global oil supplies.

- Trump said he would bring the ceasefire deadline forward to 10-12 days from July 28. He appears to have lost patience with Russian President Putin saying he’s “not so interested in talking any more” after the latter has said one thing and done another. Trump said that he’ll likely make an announcement Tuesday. The original deadline was September 2.

- With OPEC meeting on August 3 to decide its output target for September and sanctions & trade remaining in focus, attention remains on fundamentals. US industry-based inventory data is released later Tuesday and will be monitored for signs of weakness in demand.

- Later preliminary June US trade, May house prices, July consumer confidence and June JOLTS job openings are released. There is also preliminary Q2 Spanish GDP.

Gold In Narrow Range Ahead Of Key Events This Week

Gold has been range trading during today’s APAC session, holding Monday’s loss, as markets wait for key events taking place this week. Wednesday’s FOMC decision is a particular focus but so too are trade talks, US Q2 GDP and July payrolls on Wednesday and Friday respectively. Bullion is 0.1%lower at $3312.2/oz after falling to a low of $3308.15 followed by a high of $3320.95. The moderately higher US dollar and yields have been pressuring gold.

- US-China talks will continue today. US commerce secretary Lutnick expects that there will be a 90-day extension of the tariff lull. Korea, Thailand and Brazil are working on agreements before the August 1 deadline.

- Bloomberg reported on research from Fidelity stating the possibility that gold could reach $4000/oz by end-2026 driven by Fed rate cuts, weaker greenback and continued central bank buying.

- Silver is down 0.2% to $38.10. It has been also been in a narrow range between $38.198 and $38.047.

- Equities are mixed with the S&P e-mini up 0.1% and KOSPI +0.5% but Hang Seng down 1.0% and Nikkei -0.9%. Oil prices are slightly lower with WTI -0.2% to $66.58/bbl. Copper is down 0.4%.

- Later preliminary June US trade, May house prices, July consumer confidence and June JOLTS job openings are released. There is also preliminary Q2 Spanish GDP.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 29/07/2025 | 0600/0800 | Flash Quarterly GDP Indicator | ||

| 29/07/2025 | 0700/0900 | *** | GDP (p) | |

| 29/07/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 29/07/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 29/07/2025 | 0830/0930 | ** | BOE M4 | |

| 29/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 29/07/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 29/07/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 29/07/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 29/07/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 29/07/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 29/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/07/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 30/07/2025 | - | Bank of Japan Meeting | ||

| 30/07/2025 | 0130/1130 | *** | CPI inflation | |

| 30/07/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 30/07/2025 | 0530/0730 | *** | GDP (p) | |

| 30/07/2025 | 0530/0730 | ** | Consumer Spending | |

| 30/07/2025 | 0600/0800 | ** | Retail Sales | |

| 30/07/2025 | 0600/0800 | ** | Retail Sales | |

| 30/07/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 30/07/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 30/07/2025 | 0700/0900 | *** | HICP (p) | |

| 30/07/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/07/2025 | 0800/1000 | *** | GDP (p) | |

| 30/07/2025 | 0800/1000 | *** | GDP (p) | |

| 30/07/2025 | 0800/1000 | ECB Wage Tracker | ||

| 30/07/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 30/07/2025 | 0900/1100 | *** | EMU Preliminary Flash GDP | |

| 30/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 30/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/07/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/07/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/07/2025 | 1345/0945 | *** | Bank of Canada Policy Decision |