MNI EUROPEAN OPEN: Ueda Sees Limit To Boost Economy Via Easing

EXECUTIVE SUMMARY

- TRUMP SAYS CHINA ‘NOT EASY’ AS TRADE TALKS TO RESUME TUESDAY - BBG

- MAY CONSUMERS INFLATION EXPECTATIONS FALL - NY FED - MNI BRIEF

- TRUMP ADMINISTRATION DEPLOYS MARINES TO LOS ANGELES, VOWS TO INTENSIFY MIGRANT RAIDS - RTRS

- BOJ’S UEDA SEES LIMIT TO BOOST ECONOMY VIA EASING - MNI BRIEF

- BOJ LIKELY TO EASE TAPERING PACE OF BOND BUYS, EX-OFFICIAL SAYS - BBG

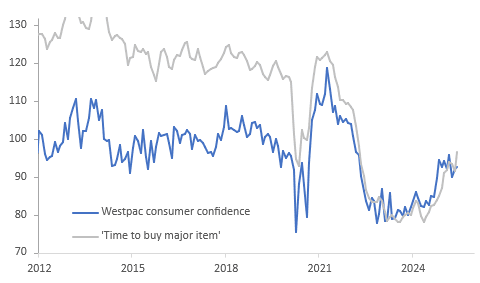

- AUSTRALIA'S CONSUMER SENTIMENT RISES IN 'CAUTIOUS PESSIMISM' - BBG

Fig 1: Lower Rates/Inflation Cautiously Boosting Australian Confidence

Source: MNI - Market News/LSEG

UK

ENERGY (BBC): “The government has committed £14.2bn of investment to build the new Sizewell C nuclear plant on the Suffolk coastline, ahead of the Spending Review. It will create 10,000 direct jobs, thousands more in firms supplying the plant and generate enough energy to power six million homes, the Treasury said.”

RETAIL (BBG): “UK retail sales rose in May at the slowest pace in six months, an industry group found, as increasing prices and higher monthly bills squeezed household budgets.”

EU

FRANCE (POLITICO): “Speaking at a press conference in Nice on Monday, Macron said: “My wish is that there’s not another dissolution, but I’m not in the habit of depriving myself of a constitutional power.””

US

US/CHINA (BBG): “ Trade talks between the US and China will continue into a second day, according to a US official, as the two sides look to ease tensions over shipments of technology and rare earth elements.”

INFLATION (MNI BRIEF): Consumers' inflation expectations receded in May, and uncertainty over inflation outcomes a year ahead also declined in a month in which the U.S. and China agreed to a temporary truce on tariffs, according to the New York Fed Survey of Consumer Expectations published Monday.

PROTESTS (RTRS): “The Trump administration on Monday ordered U.S. Marines into Los Angeles and intensified raids on suspected undocumented immigrants, fueling more outrage from street protesters and Democratic leaders who raised concerns over a national crisis.”

OTHER

CANADA (MNI BRIEF): The Bank of Canada will lower interest rates twice more this year as tariffs and related uncertainty shrink output while inflation remains stable, former Deputy Governor Paul Beaudry said Monday.

CANADA (MNI BRIEF): Canadian Prime Minister Mark Carney pledged to boost military spending to the NATO goal of 2% of GDP this year, a target past governments resisted for decades because the cost adds pressure on the deficit, while saying fewer of those dollars will go to United States contractors.

JAPAN (MNI BRIEF): The Bank of Japan has limited room to stimulate the economy via policy rate, currently 0.5%, cuts if growth comes under pressure, Governor Kazuo Ueda told lawmakers Tuesday.

JAPAN (BBG): “The Bank of Japan is likely to slow the pace of tapering its government bond purchases next fiscal year at the board’s upcoming meeting, according to a former BOJ executive director in charge of monetary policy.”

JAPAN (BBG): “ Japanese Prime Minister Shigeru Ishiba has set pay raises and a ¥1 quadrillion ($6.9 trillion) economy as the top campaign promises for this summer’s upper house election, as the date nears for voters to give their latest verdict on his administration."

NEW ZEALAND (BBG): " New Zealand Finance Minister Nicola Willis wants the central bank to increase the frequency of its rate decisions, ending its practice of a three-month summer break and bringing it in line with global peers."

AUSTRALIA (BBG): "Australia’s consumer confidence edged up in June as the conflicting moves of lower interest rates and cool inflation ran up against slow growth and ongoing trade upheavals to place households in a holding pattern.

COLOMBIA (BBG): “- Colombian inflation slowed more than expected in May to its lowest level since 2021, potentially bolstering the arguments of Finance Minister German Avila who is calling for much deeper interest rate cuts.”

CHINA

STIMULUS (YICAI): “Beijing should accelerate issuing ultra-long-term special treasuries and allocate the funds to local governments in a timely manner, after some places reported gaps in consumption subsidies, said an Yicai.com commentary.”

HOUSING (CHINA ECONOMIC NET): “Xinyang city in Henan is only allowing the sale of completed homes on newly released land, becoming the country's first place to clearly curtail the traditional pre-sale housing model, the China Economic Net has reported.”

CPI (SHANGHAI SECURITIES NEWS): “China's CPI is expected to rise slightly in H2, supported by measures to boost domestic demand and less drag from energy prices, Shanghai Securities News reported, citing Yu Ze, vice dean of the School of Economics at Renmin University.”

CHINA/US (BBG): “Huawei Technologies Co. founder Ren Zhengfei dismissed the impact of US export restrictions on China in a front-page People’s Daily article, wading into one of the key topics dogging Washington-Beijing trade negotiations.”

MNI: PBOC Net Drains CNY255.9 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY198.6 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY255.9 billion after offsetting the maturity of CNY454.5 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4586% at 09:39 am local time from the close of 1.5126% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 46 on Monday, compared with the close of 45 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1840 Tues; +1.00% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1840 on Tuesday, compared with 7.1855 set on Monday. The fixing was estimated at 7.1870 by Bloomberg survey today.

MARKET DATA

UK MAY BRC LIKE-FOR-LIKE RETAIL SALES +0.6% Y/Y; EST. +2.6%; APR. +6.8%

AUSTRALIA JUNE WESTPAC CONSUMER CONFIDENCE RISES TO 92.6; MAY 92.1

AUSTRALIA JUNE WESTPAC CONSUMER CONFIDENCE +0.5% M/M; MAY +2.2%

AUSTRALIA MAY NAB BUSINESS CONFIDENCE +2; APR. -1

AUSTRALIA MAY NAB BUSINESS CONDITIONS 0.0; APR. +2

SOUTH KOREA APRIL CURRENT ACCOUNT SURPLUS $5.70B; MAR. $9.14B

SOUTH KOREA APRIL GOODS TRADE SURPLUS $8.99B; MAR. $8.49B

JAPAN MAY M2 MONEY STOCK +0.6% Y/Y; APR. +0.5%

JAPAN MAY M3 MONEY STOCK +0.2% Y/Y; APR. +0.1%

MARKETS

US TSYS: Asia Wrap - A Quiet Session, Focus On Upcoming CPI

The TYU5 range has been 110-02 to 110-07 during the Asia-Pacific session. It last changed hands at 110-04, down 0-01 from the previous close.

- The US 2-year yield is unchanged, dealing around 4.0075%.

- The US 10-year yield has edged higher, trading around 4.48%, up 0.1 from its close.

- Bloomberg - “Negotiations in London wrapped on Monday with an extension of the talks into a second day, offering little lifeline to the struggling greenback. US Commerce Secretary Howard Lutnick called the discussions “fruitful,” while Treasury Secretary Scott Bessent described it as a “good meeting.”

- Bloomberg - “Senator Ted Cruz has proposed eliminating the interest paid to banks that deposit cash at the Federal Reserve, which could save the government around $1 trillion over a decade.”

- “JPMorgan strategists warn that this move could significantly impact banks' profitability, liquidity management strategies, and short-term interest rates, and risk the Fed losing control of money market rates.”

- The 10-year yield held its support around the 4.35% area last week. While this level holds focus will remain on potentially extending higher, CPI tomorrow will be a very important input.

- Data/Events: NFIB Small Business Optimism

JGBS: Twist-Flattener, Kato: Seeks More JGB Holding By Domestics

JGB futures are weaker and at Tokyo session lows, -12 compared to settlement levels.

- BoJ Governor Ueda has been before parliament, answering questions from lawmakers. The Governor noted limited policy space on the downside, given the current 0.50% policy rate. This is if fresh stimulus is needed. The real rate is being kept sub-0% to stimulate the economy further, as Ueda states that Japan is still some distance from the 2% inflation objective. Ueda reiterated that they will raise rates if they have confidence in achieving the 2% target.

- " Kato: Seeking more JGB holdings by domestic investors, will make efforts toward appropriate JGB management. Crucial to seek JGB holdings by diverse groups." – BBG

- The broader implications of greater domestic participation in JGBs may mean less outbound investment in overseas bonds (and potential equities). This could have implications for offshore debt markets.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs have twist-flattened across benchmarks, with the 7-year yield 2bps higher and the 30-year yield 1bp lower. The benchmark 10-year yield is 0.9bp higher at 1.477% versus the cycle high of 1.596%.

- Swap rates are flat to 5bps higher, with the curve steeper. Swap spreads are wider.

- Tomorrow, the local calendar will see PPI data.

AUSSIE BONDS: Futures Modestly Richer, Bus Survey Shows Pick Up In Labour Costs

ACGBs (YM +2.0 & XM +3.0) are modestly stronger after today’s confidence data.

- NAB business price/cost components in May were mixed, containing elements of concern and optimism. The pickup in labour costs in addition to signs that wage growth is rising again, is likely to be monitored closely. The employment component of the survey though was very weak, which may pressure pay gains.

- Westpac's measure of consumer confidence rose 0.5% in June to 92.6 after May's 2.2% increase, boosted by 50bp of RBA easing this year and lower inflation. The index is at its highest since January, but still 1.8% below that level as global events have weighed on sentiment.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's modest rally.

- Cash ACGBs are 3bps cheaper after yesterday's holiday with the AU-US 10-year yield differential at -18bps.

- The bills strip has twist-flattened, with pricing -3 to +2.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in July is given an 82% probability, with a cumulative 73bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty.

- The AOFM plans to sell A$1000mn of the 1.75% 21 November 2032 bond tomorrow.

BONDS: NZGBS: Closed With A Modest Bull-Flattener, Net Migration Data Tomorrow

NZGBs closed showing a modest bull-flattener. Benchmark yields finished at their lows, 1-2bps lower, on a local data-light session.

- (Bloomberg) -- "Economists at ANZ Bank New Zealand and ASB Bank have raised their 1q economic growth forecasts, adding to signs the RBNZ may be justified in pausing interest rate hikes next month, according to emailed notes. ANZ expects the June 19 report will show GDP grew 0.7% after provisionally projecting 0.6%."

- " NZ Treasury expects growth impulse from net exports will wane” - BBG.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's modest rally.

- Bloomberg - "Senator Ted Cruz has proposed eliminating the interest paid to banks that deposit cash at the Federal Reserve, which could save the government around $1 trillion over a decade."

- "JPMorgan strategists warn that this move could significantly impact banks' profitability, liquidity management strategies, and short-term interest rates, and risk the Fed losing control of money market rates."

- RBNZ dated OIS pricing closed with 4bps of easing priced for July and a cumulative 29bps by November 2025.

- Tomorrow, the local calendar will see Net Migration data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$200mn of the 4.25% May-36 bond.

FOREX: Asia Fx Wrap - The USD Bounces With Stocks

The BBDXY has had a range of 1208.71 - 1212.46 in the Asia-Pac session, it is currently trading around 1211. “Rachel Reeves will announce a “housing bank” as early as Wednesday to deliver cheaper financing to housebuilders, the FT reported”(BBG). “Thames Water’s senior creditors submitted a rescue plan to the UK’s water industry regulator, envisaging £5 billion of fresh funds and hefty losses for the utility’s debt holders.”(BBG)

- EUR/USD - Asian range 1.1386 - 1.1436, Asia is currently trading 1.1395. EUR has drifted lower during the Asian session as the USD bounces in response to the move higher in US stocks. Dips should continue to find demand, first support around 1.1350 then the 1.1100/1200 area.

- GBP/USD - Asian range 1.3520 - 1.3564, Asia is currently dealing around 1.3535. The GBP is attempting another run higher but is struggling to gain any momentum above the pivotal 1.3500 weekly pivot. Support seen back towards 1.3400 and then 1.3200.

- USD/CNH - Asian range 7.1778 - 7.1864, the USD/CNY fix printed 7.1840. Asia is currently dealing around 7.1860. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX +0.35%, Gold $3303, US 10-Year 4.48%, BBDXY 1211, Crude oil $65.41

Data/Events : Italy Industrial Production

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - Ueda & Stocks Help USD/JPY Higher

The Asia-Pac USD/JPY range has been 144.40 - 145.29, Asia is currently trading around 144.95. USD/JPY had a pop higher just after the Japanese Fix as Ueda said Japan’s price trend still has some way to go to reach their 2% target.

- BoJ Governor Ueda has been before parliament, answering questions from lawmakers. The Governor noted limited policy space on the downside, given the current 0.50% policy rate. This is if a fresh stimulus is needed. The real rate is being kept sub 0% to stimulate the economy further, as Ueda states that Japan is still some distance from the 2% inflation objective. Ueda reiterated that they will raise rates if they have confidence in achieving the 2% target.

- "KATO: SEEKING MORE JGB HOLDINGS BY DOMESTIC INVESTORS, WILL MAKE EFFORTS TOWARD APPROPRIATE JGB MANAGEMENT. CRUCIAL TO SEEK JGB HOLDINGS BY DIVERSE GROUPS" - BBG

- Demand seen again today in USD/JPY as risk continues to outperform, large option interest around these levels could see it do some work around here.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase.

- With the failure to break below 142.00 last week, price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. US CPI tomorrow will potentially have a say.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($708m), 143.30($618m). Upcoming Close Strikes : 143.00($1.28b June 12), 140.00($1.22b June 12), 144.00($1.19b June 13), 145.00($4.37b June 16).

CFTC data shows Asset managers maintained their already extensive JPY longs, and leveraged funds are trying again to build their own longs.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD Bounces With Higher US Equity Futures

The AUD/USD has had a range of 0.6502 - 0.6530 in the Asia- Pac session, it is currently trading around 0.6528. The AUD has again found demand back towards the 0.6500 area as it eyes testing above the 0.6550 area. Stocks have performed well in the Asian session and the AUD continues to benefit from this.

- AUSTRALIA DATA: May NAB Business Labour Costs Fastest Since January. NAB business price/cost components in May were mixed containing elements of concern and optimism. The pickup in labour costs in addition to signs that wage growth is rising again are likely to be monitored closely. The employment component of the survey though was very weak which may pressure pay gains.

- AUSTRALIA DATA: Westpac's measure of consumer confidence rose 0.5% in June to 92.6 after May's 2.2% increase boosted by 50bp of RBA easing this year and lower inflation. The index is at its highest since January but still 1.8% below that level as global events have weighed on sentiment.

- Price in the 0.6350 - 0.6550 range for now, a sustained break above 0.6550 is needed for the move higher to accelerate. Price looks set to test the top end of the range but I am not sure how far it extends until we get US CPI tomorrow out the way.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.64200(AUD771m)/ 0.6460(AUD 529m). Upcoming Close Strikes : 0.6350(AUD 711m June 12), 0.6600(AUD643m June 12)

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though continued to add to their shorts once more.

AUD/JPY - Today's range 94.15 - 94.59, it is trading currently around 94.58. Price broke the multiple tops around the 94.00 area over NFP’s. It has since managed to hold these gains, while this continues focus will turn to the high towards 96.00. Support should now be back towards the 93.00/50 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - Holds Gains, Looks To Extend

The NZD/USD had a range of 0.6028 - 0.6059 in the Asia-Pac session, going into the London open trading around 0.6055. The NZD continues to find demand on dips as Stocks have had a good session. NZD/USD looking to hold the 0.6050 area and press onwards to new highs.

- (Bloomberg) -- “Economists at ANZ Bank New Zealand and ASB Bank have raised their 1q economic growth forecasts, adding to signs the RBNZ may be justified in pausing interest rate hikes next month, according to emailed notes. ANZ expects the June 19 report will show GDP grew 0.7% after provisionally projecting 0.6%.”

- “NZ TREASURY EXPECTS GROWTH IMPULSE FROM NET EXPORTS WILL WANE - BBG.”

- The NZD has found solid demand back towards the 0.6000 area as dips remain well supported, aided by the more positive risk backdrop.

- The support back towards 0.5850 has held very well, and while this continues to hold expect buyers to be around on dips. A clear break above 0.6050/0.6100 could provide the spark for the next leg higher. The market remains short and above here they could be forced to pare back.

- CFTC Data showed Asset managers maintaining their shorts, while the leverage actually added to their shorts last week.

AUD/NZD range for the session has been 1.0763 - 1.0797, currently trading 1.0780. A top looks in place now just above 1.0900, the cross topped out yesterday towards the 1.0800/25 sell area, the first target looks to be around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Positive Day for Stocks with Taiwan Leading

With markets broadly positive across the region, Taiwan's TAIEX was the outperformer as TSMC shares surged. TSMC shares were up almost 4% on hopes that there could be some reduction of curbs on techs from the ongoing trade talks as the US indicated it would remove restrictions in exchange for rare earth shipments.

- Most of China's major bourses were up with the Hang Seng leading the way. The Hang Seng is up +0.33%, following yesterday's close up +1.63%. The CSI 300 gained just +0.16% today whilst the Shanghai Comp rose +0.11%. Shenzhen however went the other way, down -0.25%.

- The TAIEX in Taiwan is up +2.11% following on from yesterday's gain of +0.60%.

- The KOSPI is moderately higher by +0.22%, to be up over 6% in the last five trading sessions.

- The FTSE Malay KLCI rose a mere +0.14%, similar to yesterday's modest gains of +0.17%

- The Jakarta Composite is very strong, up +1.30% having been closed Friday and Monday.

- The FTSE Straits Times in Singapore is down -0.11% and the PSEi in the Philippines is down -0.55%.

- The NIFTY 50 has had a good start to the day up +0.22% following on from yesterday's gains of +0.40%.

OIL: Crude Holds Recent Gains While Watching Trade Talk Progress

Oil has held onto gains from recent trading during today’s APAC session with prices slightly higher as the market watches the second day of US-China trade talks to take place today. WTI is up 0.2% to $65.39/bbl but off the intraday high of $65.66. It remains above resistance at $64.86. Brent is 0.3% higher at $67.21/bbl following a peak of $67.40, approaching resistance at $67.73, a Fibonacci retracement level. The USD index is up 0.2%.

- Crude reacted sharply to the announcement of US reciprocal tariffs on fears of their impact on global energy demand. Thus it is watching the US-China trade talks closely and is currently mildly optimistic following US Commerce Secretary Lutnick describing negotiations so far as “fruitful”.

- The other issue markets are watching is US-Iran nuclear negotiations. The UN said that Iran’s stockpiling of almost weapons grade uranium needs to be monitored and addressed. There is a UN watchdog meeting this week in Vienna followed by one between the US and Iran in Oman on Sunday, according to Iranian officials.

- Later US May NFIB small business optimism and UK April/May labour market data are released. ECB’s Donnery and Buch appear. The focus remains on Wednesday’s May US CPI data but also Thursday’s US long-dated Treasury auction given fiscal concerns.

Gold Down Today As Risk Sentiment Improves With Ongoing Trade Talks

Gold prices reached $3327.96 early in the session up from Monday’s close of $3326.19, but trended lower thereafter falling to $3302.03. It has stabilised between $3304-3310 and is currently down 0.7% to $3305.0. The stronger US dollar (USD BBDXY +0.2%), little change in US yields and stronger equity markets have weighed on bullion in today’s APAC trading. US-China trade talks are continuing today and hopes of a deal are impacting safe-haven flows.

- Export controls are the focus of the US-China talks in London. There appears a willingness for the US to ease restrictions on tech exports if China eases rules on rare earths. Gold prices stabilised once trade negotiations began and the US delayed duties but official progress is needed for them to moderate again with any set back likely to drive a resumption of flight-to-quality flows.

- Silver is also weaker down 0.7% to $36.50 after falling to $36.31 from a high of $36.83. It broke above initial resistance at $36.71 briefly.

- Equities are generally stronger with the Hang Seng up 0.3%, TAIEX +2.1% and S&P e-mini +0.3%. Oil prices are moderately higher with WTI +0.1% to $65.37/bbl. Copper is down 1.0%, while iron ore is off its lows to be around $94-95/t.

- Later US May NFIB small business optimism and UK April/May labour market data are released. ECB’s Donnery and Buch appear. The focus remains on Wednesday’s May US CPI data but also Thursday’s US long-dated Treasury auction given fiscal concerns.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 10/06/2025 | 0600/0800 | *** | CPI Norway | |

| 10/06/2025 | 0600/0700 | *** | Labour Market Survey | |

| 10/06/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/06/2025 | 0800/1000 | * | Industrial Production | |

| 10/06/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 10/06/2025 | - | *** | Money Supply | |

| 10/06/2025 | - | *** | New Loans | |

| 10/06/2025 | - | *** | Social Financing | |

| 10/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 10/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 10/06/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/06/2025 | 0630/0730 | BOE Saporta Speech At Bank of Finland and SUERF Conference | ||

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0930/1130 | ECB Lane At 2025 Government Borrowers Forum | ||

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI |