MNI EUROPEAN OPEN: Risk Rebound Stabilizes

EXECUTIVE SUMMARY

- TRUMPS SAYS CHINA MAY GET A NEW TARIFF RATE IN NEXT 2-3 WEEKS - BBG

- WHITE HOUSE’S MIRAN OPTIMISTIC FOR CHINA DEAL - MNI BRIEF

- FED’S HAMMACK PREFERS SMALLER BALANCE SHEET - MNI

- FED'S HAMMACK - HIGH BAR FOR MARKET INTERVENTION - MNI BRIEF

- MNI BOJ WATCH: BOARD LIKELY TO HOLD AS FED, TARIFFS WEIGH

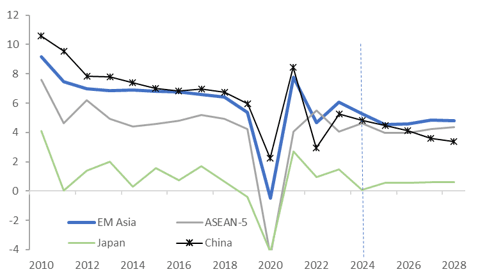

Fig 1: IMF Asia GDP growth outlook %

UK

EU (ECONOMIST): “The British prime minister, Sir Keir Starmer, is due to meet the president of the European Commission, Ursula von der Leyen, on Thursday. This comes ahead of an EU-Britain summit on May 19th that should kick off a much-advertised reset of the post-Brexit relationship.”

EU

ECB (MNI BRIEF): There is little in the way of inflationary risk in the eurozone and the European Central Bank can almost say “mission accomplished” regarding prices, Bank of France Governor Francois Villeroy de Galhau said on Wednesday.

EUR (MNI BRIEF): The European Central Bank would need to offer more swap lines and repo facilities if it were to extend the international role of the euro, Dutch central bank chief Klaas Knot said in a speech at the IMF-World Bank spring meeting in Washington on Wednesday, noting that these are already provided to some eastern European countries.

FISCAL (POLITICO): “In its new half-yearly Fiscal Monitor, the IMF forecast that global public debt will rise by 2.8 percentage points in 2025 to around 95 percent of gross domestic product (GDP). It expects a further increase to nearly 100 percent of world GDP by the end of the decade. Its projections for France and Germany are particularly stark, suggesting that neither country will be able to reduce their budget deficits to levels generally considered sustainable by the end of the decade.”

EU/CHINA (FT/BBG): “Beijing is getting ready to remove sanctions it placed on European lawmakers four years ago, the Financial Times reports — a move that could lead to the revival of an investment deal between the two sides just as punishing US tariffs hit China’s economy.”

CHINA (POLITICO): “"The Commission shall not meet with any lobby groups and/or trade associations that represent Huawei’s interests and/or speak on its behalf," the Commission's spokesperson service told POLITICO in a statement.”

US/UKRAINE (BBG): “President Donald Trump ratcheted up pressure on Volodymyr Zelenskiy to accept a peace deal that critics fear will favor Moscow, accusing the Ukrainian president of prolonging the war that’s now in its fourth year.”

UKRAINE (POLITICO): “The Ukrainian opposition is demanding that President Volodymyr Zelenskyy come to the country’s parliament and explain to members what is actually going on with peace talks and the minerals deal with the United States.”

TRADE (POLITICO): “French Economy and Finance Minister Eric Lombard said Wednesday the European Union and the United States should try to conclude a free-trade agreement.”

EU (POLITICO): “EU competition boss Teresa Ribera has defended the timing of the European Commission's fines on Apple and Meta, waving off criticism that the penalties were delayed to avoid a further escalation of U.S. tariffs.”

ITALY (POLITICO): “Italy’s government is privately unsure that its plan to reach NATO’s defense spending target of 2 percent of GDP will pass muster, despite public assurances to the contrary. The government has said it will be able to reclassify existing civil expenditures to reach that target — but two Italian officials familiar with the budget discussion believe this may not convince the European Commission or NATO.”

US

US/CHINA (MNI BRIEF): White House Council of Economic Adviser Chair Stephen Miran said Wednesday he is optimistic about the Trump administration striking a deal with China that would de-escalate trade tensions.

US/CHINA (BBG): " President Trump says a new tariff rate for China could come in the next two to three weeks."

TARIFFS (FT/BBG): “ The Trump administration is considering reducing tariffs on auto parts ahead of a May 3 deadline that has drawn the ire of global carmakers, according to the Financial Times.”

FED (MNI): Federal Reserve Bank of Cleveland President Beth Hammack on Wednesday urged the FOMC to continue reducing its balance sheet and trimming reserves to an amount that may require occasional intervention from the central bank to keep overnight rates under control.

FED (MNI BRIEF): The Federal Reserve must keep a very high bar for any possible market intervention in times of turmoil that is reserved for a full-on breakdown in market functioning of the kind seen in 2008 or 2020, Cleveland Fed President Beth Hammack said Wednesday.

FED (MNI BRIEF): The economic outlook is too uncertain for the Federal Reserve to make any near-term shifts in monetary policy, Cleveland Fed President Beth Hammack said Wednesday.

ECONOMY (MNI): U.S. economic activity was mixed in recent weeks and prices climbed as businesses reported a surge in uncertainty following the announcement of larger-than-expected tariffs this month, the Federal Reserve said in its latest Beige Book report released Wednesday.

DOLLAR (MNI BRIEF): Treasury Secretary Scott Bessent said Wednesday the United States continues to have a strong dollar policy and the currency will stay the world's reserve currency.

FISCAL (BBG): “ President Donald Trump said that imposing a higher tax rate on millionaires would spur the country’s richest to leave the US, downplaying an idea that is under discussion in some Republican circles as a way to pay for an economic package.”

OTHER

JAPAN (MNI BRIEF): Japan’s services producer price index rose 3.1% y/y in March, decelerating from February’s revised 3.2%, showing that corporate pass-through of cost increases remained solid, preliminary data released by the Bank of Japan on Thursday showed.

JAPAN (MNI BOJ WATCH): The Bank of Japan board is expected to keep its 0.5% policy interest rate unchanged at the two-day meeting ending May 1, as policymakers monitor the economic and inflationary impact of recent U.S. trade policies and volatile markets.

INDIA (BBG): “India will suspend a decades old World Bank-negotiated water sharing treaty and downgrade diplomatic ties with Pakistan in retaliation for one of the deadliest attacks on civilians in years.”

IRAN (POLITICO): “Western governments should create a “strike fund” to support a wave of industrial action across Iran that will paralyze the state and hasten the end of the regime, according to the son of the country’s former leader.”

SOUTH AFRICA (RTRS): "South Africa will not increase its value-added tax (VAT) from May 1, the finance ministry said on Thursday, after the proposed hike faced opposition from political parties and caused friction within the coalition government."

CHINA

FISCAL (SECURITIES TIMES): “Local governments will introduce a new round of consumption stimulus this week with a focus on boosting tourism ahead of the May Day holiday and quickening the replacement of big-ticket items, Securities Daily reported.”

HOUSING (SHANGHAI SECURITIES NEWS): “Xiamen city further upgraded the use of housing vouchers to compensate residents displaced under urban-renewal efforts, Shanghai Securities News reported.”

PROPERTY (SECURITIES TIMES): “‘Debt-to-equity swap has become a mainstream approach in Chinese developers’ debt restructuring, Securities Times reported, citing recent public disclosure by companies such as Sunac and Kaisa.”

CHINA MARKETS

MNI: PBOC Net Drains CNY27.5 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY218 billion via 7-day reverse repos, with the rate unchanged at 1.50%. The operation led to a net drain of CNY27.5 billion after offsetting the maturities of CNY245.5 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.6565% at 10:00 am local time from the close of 1.6508% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 51 on Wednesday, compared with the close of 46 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.2098 Thurs; -0.74% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.2098 on Thursday, compared with 7.2116 set on Wednesday. The fixing was estimated at 7.3089 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND APRIL ANZ CONSUMER CONFIDENCE INDEX 98.3; MAR. 93.2

NEW ZEALAND APRIL ANZ CONSUMER CONFIDENCE +5.5% M/M; MAR. -3.5%

JAPAN MARCH SERVICES PRODUCER PRICES +3.1% Y/Y; EST. +3.0%; FEB. +3.2%

S. KOREA'S Q1 GDP -0.2% Q/Q & -0.1% Y/Y; EST. +0.1% & 0.0%; Q4 +0.1% & +1.2%

S. KOREA COMPOSITE BUSINESS SURVEY MFG APR. 93.1; MAR. 91.9

S. KOREA COMPOSITE BUSINESS SURVEY NON-MFG APR. 84.5; MAR. 82.9

MARKETS

Table of Contents

TYM5 has traded a little higher with a range of 110-20+ to 110.27 during the Asia-Pacific session. It last changed hands at Heading 110-27, up 0.06 from the previous close.

- The US 10-year yield is lower, dealing around 4.35%, down from its close around 4.38%

- The US 2-year yield is lower, dealing around 3.84%, down from its close around 3.87%.

- Risk has struggled to hold onto its gains leaking lower in Asia as the market looks through the Trump administration's attempts at de-escalation.

- “Minneapolis Fed President Neel Kashkari said it’s the central bank’s job to ensure tariffs don’t cause ongoing inflation.”(per BBG)

- The Department of the Treasury will auction $44 billion of an April 2032 note.

- The 10-year Yield has bounced off its support around the 4.25 area once more, the 10-year is consolidating with the range looking something like 4.25/4.50% for now.

- Data/Events : Chicago Fed Activity Index, Durable Goods Orders, Initial Jobless Claims, Existing Home sales.

JGBS: Futures Stronger After Reversing O/N Weakness, Tokyo CPI Tomorrow

JGB futures are stronger and at session highs, +16 compared to the settlement levels, after rejecting overnight weakness.

- According to MNI's Technicals Team, JGBs are holding the bulk of the recent strong bullish reversal, rejecting any test of fresh cycle lows for the M5 contract. This defies the bearish momentum studies drawn on the longer-term chart, clearing moving-average resistance to print 142.40 at the new upper level.

- Cash US tsys are 2-4bps richer in today's Asia-Pac session. After US market close, US President Trump delivered wide-ranging comments in the Oval Office. Trade/tariffs and monetary policy were among the focus points. Today's US calendar will see Chicago Fed Activity Index, Durable Goods Orders, Initial Jobless Claims and Existing Home Sales.

- Cash JGBs are modestly mixed across benchmarks, with yields 1bp higher to 2bps lower, pivoting at the 30-year.

- Today's 2-year bond auction showed improved demand. The low price came in just above the Bloomberg-surveyed forecast, while the cover ratio increased to 3.5801x, and the auction tail narrowed slightly compared to last month.

- Swap rates are 1-4bps lower, with a steeper curve.

- Tomorrow, the local calendar will see Tokyo CPI and Dept Store Sales data alongside BoJ Rinban Operations covering 3-25-year JGBs.

AUSSIE BONDS: Little Changed After A Subdued Ahead Of Long Weekend

ACGBs (YM flat & XM +1.5) are slightly stronger but well above the morning's lows on a local data light session. Accordingly, the domestic market's attention remained focused on headlines and US tsys.

- Cash US tsys are 2-4bps richer in today's Asia-Pac session. After US market close, US President Trump delivered wide-ranging comments in the Oval Office. Trade/tariffs and monetary policy were among the focus points. Today's US calendar will see Chicago Fed Activity Index, Durable Goods Orders, Initial Jobless Claims and Existing Home Sales.

- Cash ACGBs are flat to 2bps richer with the 3/10 curve flatter and the AU-US 10-year yield differential -11bps.

- Swaps are little changed.

- The bills strip is -1 to -2 across contracts.

- RBA-dated OIS pricing is modestly mixed across meetings today. A 50bp rate cut in May is given an 11% probability, with a cumulative 116bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- Tomorrow, the local market will be closed for the ANZAC Day holiday.

BONDS: NZGBS: Closed At Best Levels Ahead Of ANZAC Day Holiday

NZGBs closed showing modest twist-flattening, with benchmark yields 2bps higher to 1bp lower. This, however, masked the fact that yields finished at or near session bests after opening 6-7bps higher. The NZ-US 10-year yield differential closed 3bps tighter at +17bps.

- The intraday session strength came despite a broad-based pick-up in ANZ consumer confidence. It rose 5.5% to 98.3 in April boosted by another 25bp of monetary easing during the month and despite heightened global uncertainty around US trade policy. It has resumed its uptrend and printed at its highest since December. Both current and future conditions improved.

- Nevertheless, the primary focus for the local market remains abroad. Cash US tsys are 2-4bps richer in today's Asia-Pac session. After the US market close, US President Trump delivered wide-ranging comments in the Oval Office. Trade/tariffs and monetary policy were among the focus points.

- Today’s NZGB supply saw solid demand with cover ratios ranging from 3.32x (May-36) to 4.38x (May-30).

- Swap rates closed flat.

- RBNZ dated OIS pricing closed little changed across meetings. 27bps of easing is priced for May, with a cumulative 80bps by November 2025.

- Tomorrow, the local market will be closed for the ANZAC Day holiday.

FOREX Wrap - USD Holding Gains, Can It Rebound Further ?

The BBDXY has had an Asian range of 1226.14 - 1228.47, Asia is currently trading around 1227. Trump ramped up pressure on Zelensky to accept a peace deal, “ We are very close to a Deal but the man with ‘no cards’ should now, finally GET IT DONE” he wrote on Truth Social. Bloomberg reports “Christine Lagarde said US tariffs may be more disinflationary than inflationary for Europe, but acknowledged the net impact is still unclear.”

- EUR/USD - Asian range 1.1316 - 1.1358, Asia is currently trading 1.1338.Back at the support around 1.1300, should this area not hold demand should remerge on dips back to 1.1000/1.1100.

- GBP/USD - Asian range 1.3253 - 1.3287,the market seems happy to accumulate GBP on dips but the risk of a short-term retracement remains. Buyers should reemerge back towards the 1.3000 area.

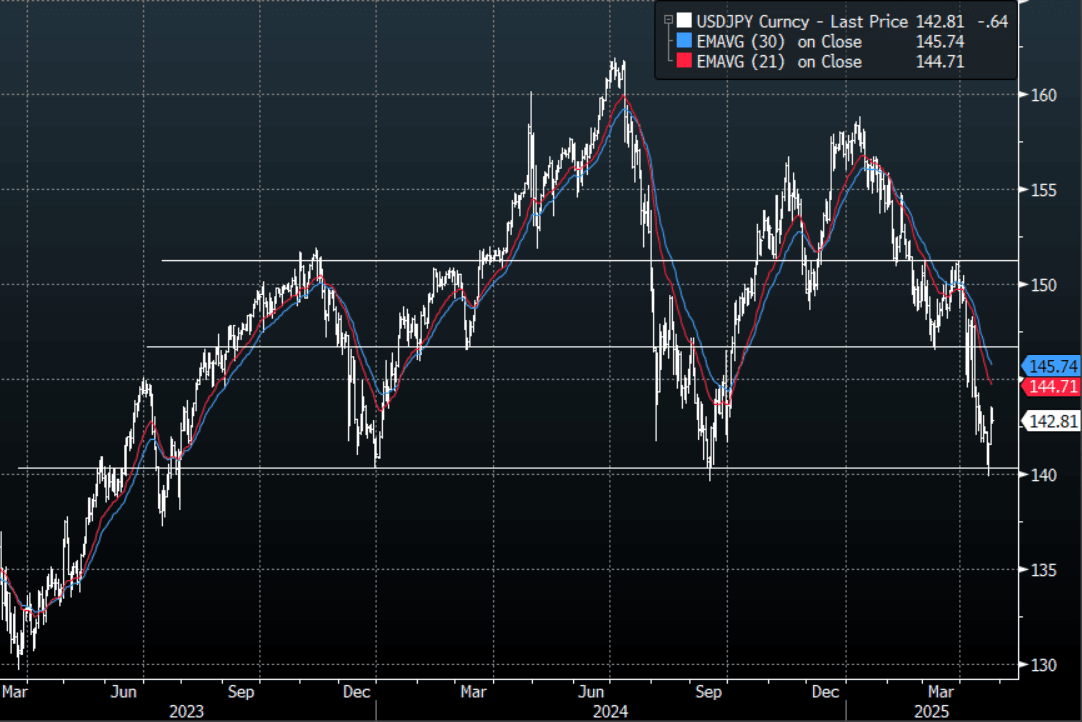

- USD/JPY - Asian range 142.60 - 143.46, has drifted lower for most of the Asia session. On the day the 143 handle should still see some supply, then more importantly the 145/146 area should once more offer good levels for sellers to reengage.

- USD/CNH - Asian range 7.2813 - 7.3039, the USD/CNY fix printed at 7.2098. USD/CNH continues to trade sideways and find support towards 7.2800.

- Cross asset : SPX -0.2%, Gold 3330, US 10yr 4.35%, BBDXY 1227, Crude oil 62.33.

- Data/Events : Chicago Fed Activity Index, Durable Goods Orders, Initial Jobless Claims, Existing Home sales.

Fig 1: USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

FOREX: Antipodean Wrap - AUD & NZD Consolidate

Risk has struggled to hold onto its gains leaking lower in Asia as the market looks through the Trump administration's attempts at de-escalation. Overall the market seems comfortable buying AUD and NZD on dips, but is wary at current levels as price stalls and potentially signals some sort of a retracement ?

- AUD/USD - Asian range 0.6352 - 0.6372, AUD has traded sideways most of the Asian session. Dips back to the 0.6250/0.6300 area should continue to find demand while the market continues to focus on a lower USD.

- AUD/JPY - Asian range 90.63 - 91.32. Price goes into the London trading around 90.80, still firmly within the last 8 days range of 0.8950/0.9200.

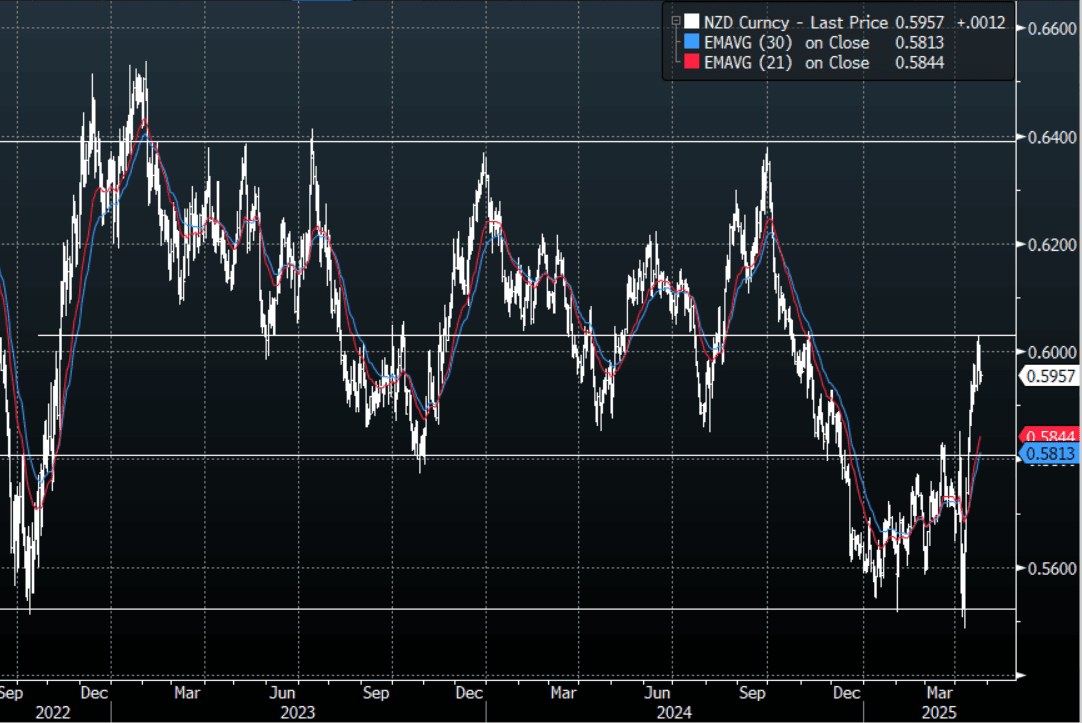

- NZDUSD - Asian range 0.5944 - 0.5963, going into London trading around 0.5950. Price struggles to hold above 0.6000 once more, demand should return first around 0.5900, then around the 0.5850 area.

- AUD/NZD - Asian range 1.0676 - 1.0708, the cross has drifted lower in the Asian session. The cross is going into London pretty directionless but the risks appear skewed towards bounces being capped, with supply returning on bounces back towards the 1.0800 area.

Fig 1 : NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Japan & Aust Firmer, But Taiwan & South Korea Weaker

Outside of Hong Kong losses, trends in other Asia Pac markets have been mixed. US equity futures sit modestly in the red, Eminis under 5400 at this stage, struggling to hold above this level. Focus remains on the next tariff related news flow piece, with Trump stating earlier China's new tariff rate could come in the next 2-3 weeks.

- Japan markets have risen further, last up +0.70% for the Topix. Export related names are rising, perhaps benefiting from the recent rebound in USD/JPY, although other export orientated/tech related markets have struggled today.

- The Taiex is off 0.50%, while the Kospi is down around 0.45%. We had Q1 GDP out of South Korea earlier, which was below market expectations and showed a y/y contraction for the first time 2020.

- In SEA, market shifts are not beyond 1% in either direction at this stage. The ASX 200 is a up a further 0.70%, continuing its recent recovery. The index is now back to early April levels.

CHINA STOCKS: Hong Kong Stocks Pare Recent Gains

Hong Kong stocks are struggling in the first part of Thursday trade. The HSI was last down 1.25%, putting the index back under 22000. If this trend continues through to the close it would be the HSI's first dip since last Wednesday. Trade/tariff concerns remain front and center in terms of market sentiment shifts. The HS tech sub index is off around 2.25% at this stage, so it continues to display a higher beta compared to the main index.

- Mainland China indices have ticked down as well, the CSI 300 last off around 0.20%.

- Earlier remarks were made by US President Trump in the oval office, which suggested the ball was in China's court in terms of a potential trade/tariff deal. He stated if a deal can't be reached then the US will decide on the tariff rate. An announcement on tariff levels was possible within the next 2-3 weeks Trump stated.

- This followed overnight comments from US Tsy Secretary Bessent, who stated that there had been no unilateral offer from Trump to cut China tariffs and that a full trade deal negotiation would take a number of years.

- Such a backdrop may be tempering HK/China equity sentiment, particularly in light of recent gains. The HSI was tracking close to +15% firmer from recent April lows at the start of this week.

- UBS also downgraded Hong Kong stocks back to neutral from overweight, highlighting tariff concerns on the revenue outlook (per BBG).

OIL: Crude Range Trading, Monitoring Tariff & OPEC Developments

Oil prices are little changed during today’s APAC session holding onto Wednesday’s losses given lacklustre risk sentiment with mixed equities and lower commodity prices. Crude has been in a narrow range of less than 50c/bbl. WTI is up 0.1% to $62.36/bbl after an earlier high of $62.54. Brent is +0.1% to $66.21 following today’s peak of $66.40. Benchmarks are likely to remain sensitive to US tariff developments given the consequences for global energy demand. The USD index is down 0.1%.

- There were Reuters reports yesterday that OPEC is under pressure from within to increase output materially again in June, which pushed prices lower. The group meets on May 5 to discuss quotas at a time of lax compliance.

- Politico reported that the White House is considering lifting sanctions on Russia’s Nord Stream 2 gas pipeline but Secretary of State Rubio said that the suggestion is “unequivocally false” and he hadn’t spoken with Middle Eastern envoy Witkoff about easing Russian sanctions and that was not part of talks on a Ukraine deal.

- Later the Fed’s Kashkari speaks. US March orders, Chicago Fed index, April Kansas manufacturing index and jobless claims print. The ECB’s Lane participates in a panel and Germany’s April Ifo survey is published.

GOLD: Rebounds +1% After Recent Losses

After cumulative losses of 4% in the past two sessions, gold has rebounded in the first part of Thursday trade. Bullion got as high as $3367.34, but was last near $3325/30, still up +1.2% for the session. The broader risk rebound has stalled somewhat from a US equity futures standpoint, while region equities are mixed, albeit with Hong Kong weaker, which could be lending some support to gold moves today. The USD BBDXY index is down, but only modestly and remains close to recent highs.

- Near term risk sentiment is likely to be dictated by trade/tariff developments, which will inevitably spillover to gold.

- The structural backdrop for gold still looks sound though: uncertainty around global growth, fragile equity market sentiment and underlying flows from central banks all support points.

- In terms of technicals, firm support is seen at the 20-day EMA of $3,193.5. Shallower selloffs will be considered corrective at this stage. Initial resistance is at $3,500.1, the Apr 22 high. Moving average studies remain in bullish mode.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 24/04/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 24/04/2025 | 0700/0900 | ** | PPI | |

| 24/04/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 24/04/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/04/2025 | 1230/0830 | * | Payroll employment | |

| 24/04/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 24/04/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/04/2025 | 1300/1500 | ECB's Lane at Peterson Institute Webcast on Monetary Policy Strategy | ||

| 24/04/2025 | 1325/1425 | BOE's Lombardelli on Monetary Policy Strategy | ||

| 24/04/2025 | 1400/1000 | *** | NAR existing home sales | |

| 24/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/04/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/04/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/04/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/04/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 24/04/2025 | 2100/1700 | Minneapolis Fed's Neel Kashkari | ||

| 25/04/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 25/04/2025 | 2330/0830 | ** | Tokyo CPI | |

| 25/04/2025 | 0600/0700 | *** | Retail Sales | |

| 25/04/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade |