MNI EUROPEAN OPEN: Rising JGB Yields Remain In Focus

EXECUTIVE SUMMARY

- NVIDIA TO RESUME H20 CHIP SALES TO CHINA IN SURPRISE US REVERSAL - BBG

- EU HOPES FOR MINI-DEALS WITH US DESPITE TARIFF THREAT - MNI

- JAPAN’S RULING COALITION SEEN LOSING UPPER HOUSE MAJORITY, POLLS SHOW -RTRS

- CHINA’S Q2 GDP BEATS EXPECTATIONS TO GROW 5.2% - MNI BRIEF

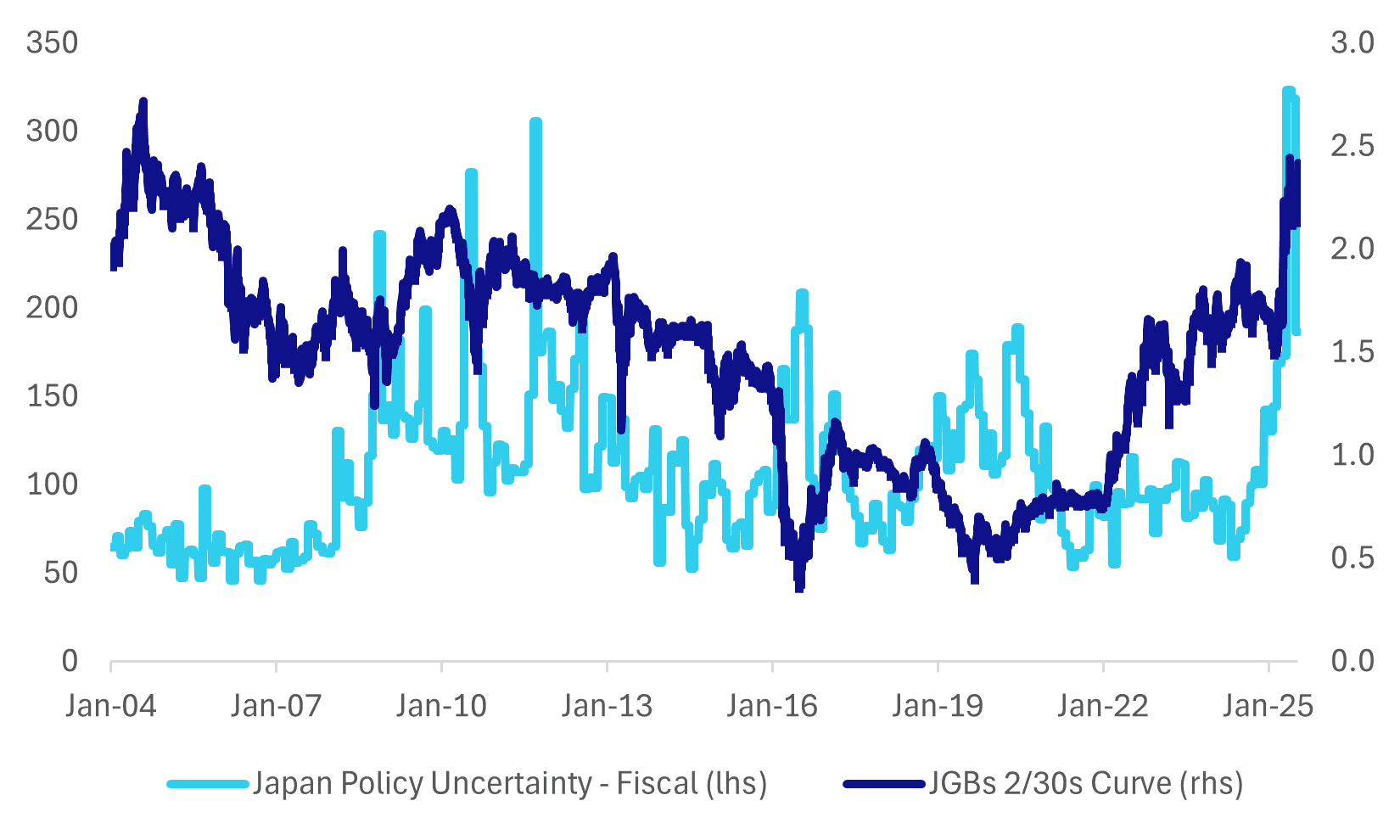

Fig 1: JGBs Yield Curve & Fiscal Policy Uncertainty Index

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

RETAIL SALES (BBG): “ The UK economy is showing more signs of rebounding from its recent slump, with a jump in June retail sales adding to evidence of a strong pick-up in activity seen in other leading indicators.”

EU

TRADE (MNI): The European Union is considering turning its attention to securing a series of mini-trade deals with the U.S., including exemptions for cars, pharma and food, which would bypass a 30% tariff threatened by President Donald Trump while talks for a more comprehensive deal continue past the Aug 1 deadline, EU officials told MNI.

TRADE (POLITICO): “The European Union is looking at targeting €72 billion in U.S. goods in a second round of trade countermeasures, including aircraft, cars and car parts, according to a list seen by POLITICO on Monday.”

TRADE (BBG): “ President Donald Trump indicated he is open to more trade negotiations, including with the European Union, even as he insisted that his letters threatening new tariff rates are “the deals” for US trading partners.”

RUSSIA (BBG): “US President Donald Trump threatened to impose stiff financial penalties on Russia if it does not end hostilities with Ukraine even as he pledged fresh weapons supplies for Kyiv.”

FRANCE (BBG): “Prime Minister Francois Bayrou will outline a plan on Tuesday to sharply narrow France’s deficit, setting the stage for a parliamentary battle that risks triggering another government collapse.”

US

US/CHINA (BBG): “Nvidia Corp. plans to resume sales of its H20 artificial intelligence accelerator to China based on assurances from Washington that such shipments would be approved, a dramatic reversal from the Trump administration’s earlier stance.”

OTHER

US/MEXICO (BBG): “The US government withdrew from a longstanding trade agreement with Mexico governing tomato imports and will push forward with a new tariff of just over 17%, the US Commerce Department announced Monday.”

JAPAN (RTRS): “Japan's ruling coalition will likely lose its majority in the upper house election on July 20, media polls showed on Tuesday, heightening the risk of political instability at a time the country struggles to strike a trade deal with the U.S.”

JAPAN (BBG): "Japanese inflation is strong enough for the Bank of Japan to consider an interest rate hike as soon as this fall if tariff uncertainties fade, according to a former BOJ chief economist."

AUSTRALIA (BBG): "Prime Minister Anthony Albanese said Australia values its relationship with China and will approach it in a “calm and consistent” manner, during opening remarks at a meeting with President Xi Jinping."

CHINA

GDP (MNI BRIEF): The Chinese economy grew by 5.2% y/y in Q2, outperforming market expectations of 5.1%, according to data released Tuesday by the National Bureau of Statistics. This brings H1 growth to 5.3%.

YUAN (21st Century Business Herald): “The yuan is expected to remain strong in the second half, supported by China’s economic resilience and the rising possibility of Federal Reserve cuts amid growing pressure from U.S. President Donald Trump, wrote Xiao Yu, associate researcher at the Chinese Academy of Social Sciences, in a commentary.”

LOCAL GOVERNMENT BONDS (YICAI): “China should allow local governments to tap into future bond quotas to proactively address off-balance sheet debt, analysts told Yicai.com.”

MNI: PBOC Net Injects CNY273.5 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY342.5 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY273.5 billion after offsetting the maturity of CNY69 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.5053% at 09:30 am local time from the close of 1.5360% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 51 on Monday, compared with the close of 50 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1498 Tues; +1.37% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.14918 on Tuesday, compared with 7.1491 set on Monday. The fixing was estimated at 7.1740 by Bloomberg survey today.

MARKET DATA

AUSTRALIA JULY WESTPAC CONSUMER CONFIDENCE M/M 0.6%; PRIOR 0.5%

AUSTRALIA JULY WESTPAC CONSUMER CONFIDENCE INDEX 93.1; PRIOR 92.6

CHINA JULY NEW HOME PRICES -0.27%; PRIOR -0.22%

CHINA JULY NEW HOME PRICES -0.61%; PRIOR -0.50%

CHINA GDP Q/Q 1.1%; MEDIAN 0.9%; PRIOR 1.2%

CHINA GDP Y/Y 5.2%; MEDIAN 5.1%; PRIOR 5.4%

CHINA JUNE RETAIL SALES 4.8%; MEDIAN 5.3%; PRIOR 6.4%

CHINA JUNE INDUSTRIAL PRODUCTION Y/Y 6.8%; MEDIAN 5.6%; PRIOR 5.8%

CHINA JUNE FIXED ASSETS EX RURAL YTD Y/Y 2.8%; MEDIAN 3.6%; PRIOR 3.7%

CHINA JUNE PROPERTY INVESTMENT YTD Y/Y -11.2%; MEDIAN -10.9%; PRIOR -10.7%

CHINA JUNE SURVEYED JOBLESS RATE 5.0%; MEDIAN 50%; PRIOR 5.0%

MARKETS

US TSYS: Asia Wrap - Quiet Session Looking Toward CPI

The TYU5 range has been 110-20+ to 110-25 during the Asia-Pacific session. It last changed hands at 110-23, down 0-01 from the previous close.

- The US 2-year yield is trading around 3.898%.

- The US 10-year yield is trading around 4.433%.

- The 10-year yield is again testing the 4.40/45% pivot within its wider 4.10% - 4.65% range. The market is clearly worried about inflation and the CPI this week will be a critical input into the market's thinking. A sustained close back above the 4.45% area could see more longs pared back, above here and the focus will turn back to the 4.65% area.

- Lance Roberts(RIA) - “Tuesday’s CPI and Wednesday’s PPI reports will be very helpful in appreciating how tariffs are impacting inflation. Thus far, there has been a negligible effect. However, the June reports will fully capture a period when the tariffs were being enforced. If data continues to be on the weak side, we suspect the Fed will become more dovish. However, higher-than-expected inflation data may allow them to continue to postpone rate cuts.”

- MNI US OUTLOOK/OPINION: Analysts See Core CPI On Cusp Of 0.2% or 0.3% M/M In June. Ahead of tomorrow’s US CPI release, we note that the broad Bloomberg consensus looks for both core and headline CPI inflation at 0.3% M/M in June although unrounded estimates suggest a risk of rounding lower.

JGBS: Bear-Steeper But Off Cheapest Levels

JGB futures are weaker, -13 compared to settlement levels, but ranges have been narrow.

- Today, the local calendar will be empty apart from 5-year Climate Transition supply.

- Cash US tsys are little changed in today’s Asia-Pac session. Focus is on today’s June CPI inflation data and several Fed speakers ahead of Friday evening's policy blackout.

- Cash JGBs are flat to 7bps cheaper across benchmarks, with a steeper curve. The benchmark 10-year yield is 0.7bp higher at 1.589% after revisiting the cycle high of 1.596% earlier in the session.

- As Japan's upper house elections approach (held July 20), focus remains on the relentless rise in longer-dated JGB yields. The 30-year is up 1bp at 3.182% after hitting 3.219%. This is a fresh high on record (since it was debuted in 1999, per BBG). Concerns around fiscal slippage are a factor in the JGB sell-off. The 2/30yr JGB curve is at +240bps, just off multi-decade highs.

- Swap rates are ~1bp higher to 1bp lower, with a flatter curve. Swap spreads are mostly tighter.

- Tomorrow, the local calendar will be empty.

AUSSIE BONDS: Cheaper, US CPI Tonight, PM Talks On China Relations

ACGBs (YM -3.0 & XM -1.5) are modestly cheaper with narrow ranges.

- Prime Minister Anthony Albanese said Australia values its relationship with China and will approach it in a "calm and consistent" manner. Albanese told President Xi Jinping that "dialog needs to be at the centre of our relationship" and he welcomes the opportunity to set out Australia's views and interests. (per BBG)

- Ronald Mizez (AFR) on LinkedIn: The Commonwealth Bank has urged Jim Chalmers to consider major tax reform to revive productivity, including slashing income taxes, overhauling the GST, capping superannuation concessions and introducing wealth taxes.

- Cash US tsys are little changed ahead of today's US CPI data.

- Cash ACGBs are 2bps cheaper with the AU-US 10-year yield differential at -5bps.

- The bills strip weaker, with pricing -2 to -4.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in August is given an 88% probability, with a cumulative 56bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty.

- The AOFM plans to sell A$800mn of the 4.25% 21 March 2036 bond tomorrow and A$1100mn of the 1.00% 21 November 2031 bond on Friday.

BONDS: NZGBS: Closed With A Modest Bear-Steepener

NZGBs closed showing a modest bear-steepener, with benchmark yields 1-2bps higher. Ranges were narrow. The NZ-US 10-year yield differential is unchanged on the day at +15bps.

- Cash US tsys are little changed ahead of today’s US CPI data.

- “We expect an ageing population to put downward pressure on the neutral interest rate, but other factors may offset its impact,” the RBNZ said in a report published Tuesday in Wellington. Any impacts are likely to be gradual over decades, it said.” (per BBG)

- Swap rates closed 1bp higher.

- RBNZ dated OIS pricing closed little changed across meetings. 19bps of easing is priced for August, with a cumulative 33bps by November 2025.

- Tomorrow, the local calendar will see Non-Resident Bond Holdings data.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 4.50% May-30 bond, NZ$200mn of the 4.25% May-36 bond and NZ$50mn of the 1.75% May-41 bond.

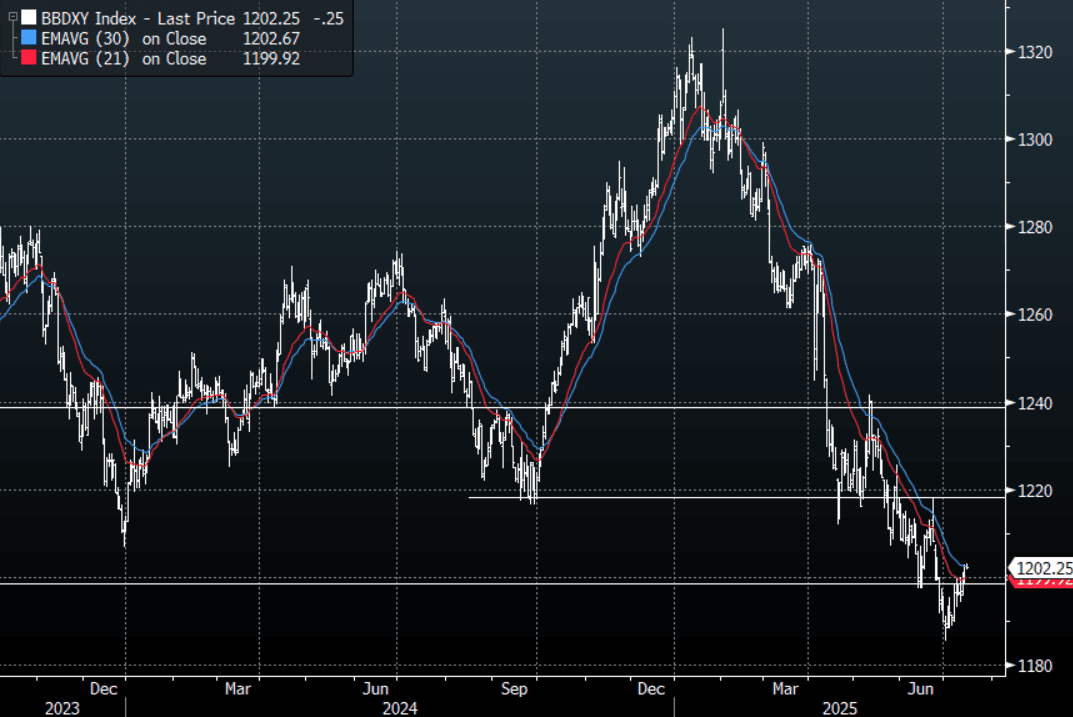

FOREX: Asia FX Wrap - BBDXY Consolidates Above 1200, Focus Turns To US CPI

The BBDXY has had a range of 1201.78 - 1203.10 in the Asia-Pac session, it is currently trading around 1202, -0.02%. The BBDXY is consolidating its gains above the 1200 area as it awaits US CPI tonight. On the way down the BBDXY has been heavily sold every time it has challenged the 30 EMA on the Daily(See Chart Below), will the sellers again use this area to reload shorts or can the USD finally initiate some sort of a correction. CHINA GDP in Line with Targets: China's second quarter GDP YoY printed slightly above estimates at +5.2%, but down from first quarter result of +5.4%. The second quarter result keeps GDP on track with the recently announced growth target of "around 5 percent" for 2025, the same as their 2024 target.

- EUR/USD - Asian range 1.1661 - 1.1678, Asia is currently trading 1.1675. The pair continues to see some demand towards the 1.1650 area. The price is still starting to look a little stretched in the short term and is vulnerable to any correction in the USD, first support is back towards 1.1600 then more importantly the 1.1450 area.

- GBP/USD - Asian range 1.3422 - 1.3441, Asia is currently dealing around 1.3430. Price has rejected the move higher and Bailey’s hint that bigger rate cuts are on their way if the job market deteriorates further has added further headwinds. Support seen around the 1.3350/1.3450 area, a close back below here could signal an even deeper correction.

- USD/CNH - Asian range 7.1689 - 7.1785, the USD/CNY fix printed 7.1491, Asia is currently dealing around 7.1780. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.25%, Gold $3355, US 10-Year 4.33%, BBDXY 1195, Crude oil $65.67

- Data/Events : Germany ZEW Survey, EZ Zew Survey & Industrial Production, Spain CPI

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

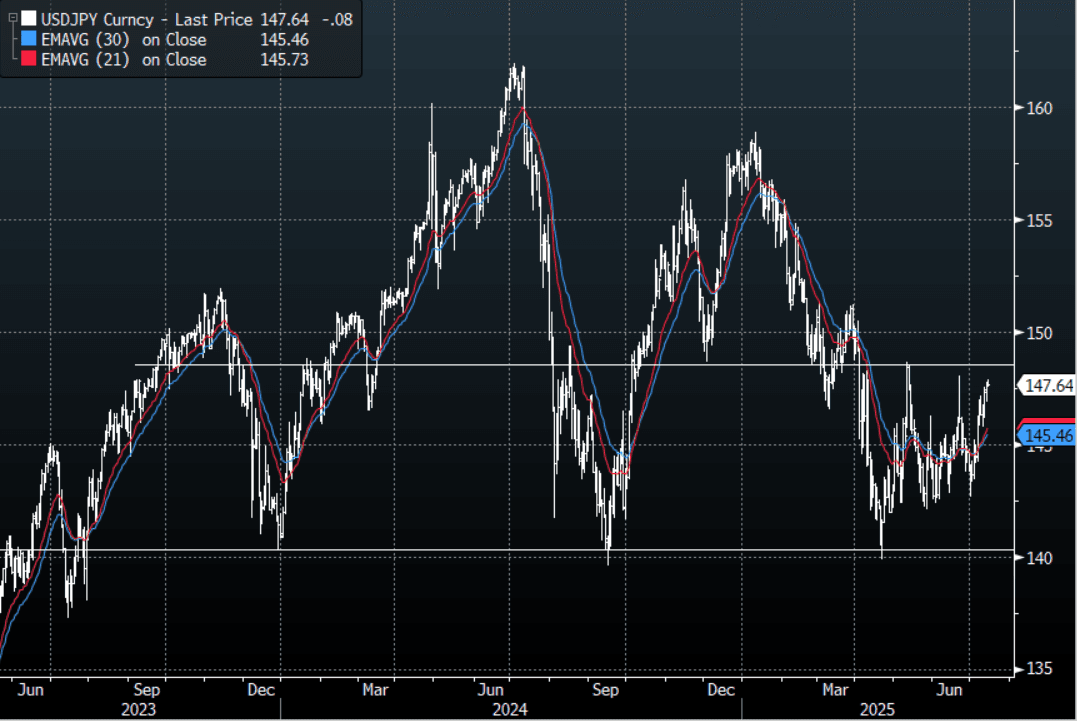

JPY: Asia Wrap - USD/JPY Consolidates Ahead Of US CPI

The Asia-Pac USD/JPY range has been 147.56 - 147.89, Asia is currently trading around 147.65, -0.05%. The pair has traded sideways with little direction, consolidating its recent move higher. The USD/JPY relentless march higher has been pretty telling, challenging a market positioned the wrong way. Price is now consolidating some of those recent gains, dips back towards 146.00 should now find support first up. The US CPI tonight will be closely watched by the bond market and consequently will also be important for USD/JPY.

- JAPAN Long Dated Yield Surge Continues, With Election Driving Uncertain Outlook: As Japan's upper house elections approach (held July 20), focus remains on the relentless rise in longer-dated JGB yields. The 30yr is up a further +4bps today, last around 3.21%. Concerns around fiscal slippage is a factor in the JGB sell-off.

- Reuters : "Barclays calculates that the rise in 30yr yields currently factors in about a three percentage-point cut to Japan's 10% consumption tax rate. "Even if the ruling parties retain their majority in the upper house, they would still be unable to pass budget bills, including the upcoming supplementary budget, without the cooperation of the opposition parties."

- "JAPAN, EU TO ISSUE JOINT STATEMENT ON ECONOMIC ALLIANCE:YOMIURI" - BBG

- "JAPAN RULING BLOC MAY STRUGGLE FOR MAJORITY: MAINICHI ANALYSIS" - BBG

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to continue to correct higher the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 146.50($1.4b July 16).

- CFTC data shows Asset managers reduced their JPY longs slightly +89331, while leveraged funds have almost squared their newly built JPY longs +5224.

- Data/Event : US CPI

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

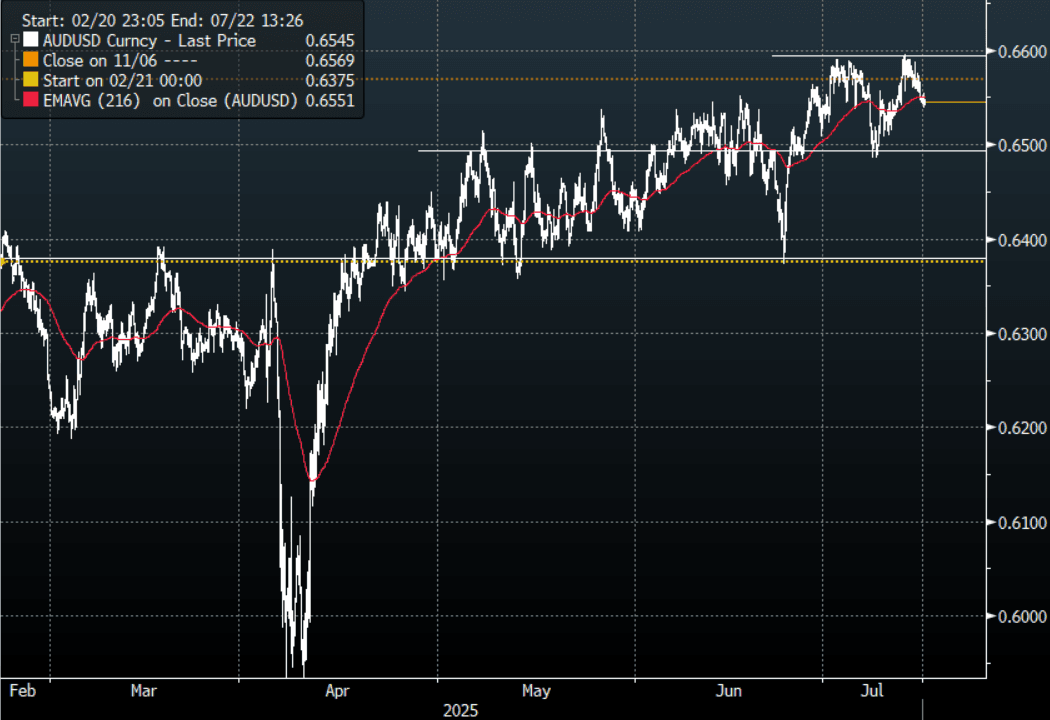

AUD: Asia Wrap - AUD/USD Middle Of The Range, Awaits US CPI

The AUD/USD has had a range of 0.6539 - 0.6555 in the Asia- Pac session, it is currently trading around 0.6545, +0.01%. Risk got a boost this morning as Nvidia posted on a blog that they had received assurances from the US Government that it would be granted licenses to resume sales of its H20 to China. AUD/USD initially tried to bounce on this but has not followed through, it trades in the middle of its recent 0.6500 - 0.6600 range awaiting US CPI tonight.

- Ronald Mizez(AFR) on LinkedIn: The Commonwealth Bank has urged Jim Chalmers to consider major tax reform to revive productivity, including slashing income taxes, overhauling the GST, capping superannuation concessions and introducing wealth taxes.

- The July Westpac consumer confidence index rose 0.6%m/m, putting the index at 93.1 (from 92.6 in June). The edge higher comes despite last week's surprise RBA on hold decision. Sentiment is up from recent lows, but still below recent highs, leaving us within recent ranges.

- The AUD/USD continues to hold above its support around 0.6500, looks like it's back to the 0.6500 - 0.6600 range and it should now take its cues from the USD. Watching to see if the market can build on this outperformance and break above 0.6600.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6560(AUD631m), 0.6495(AUD611m),. Upcoming Close Strikes : 0.6575(AUD609m July 16), 0.6480(AUD586m July18), 0.6700(AUD611m July 16).

- CFTC Data shows Asset managers added to their shorts slightly -38252, the Leveraged community pared back their shorts to -19061.

- AUD/JPY - Today's range 96.55 - 96.86, it is trading currently around 96.65, -0.20%. The pair has had a good move above 96.00 and this time looks to be building momentum to extend higher. The market has been caught wrong-footed in both legs of this pair and price action suggests a potential move back to 99.00/100.00. Dips back to 95.50/96.00 should now be supported.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

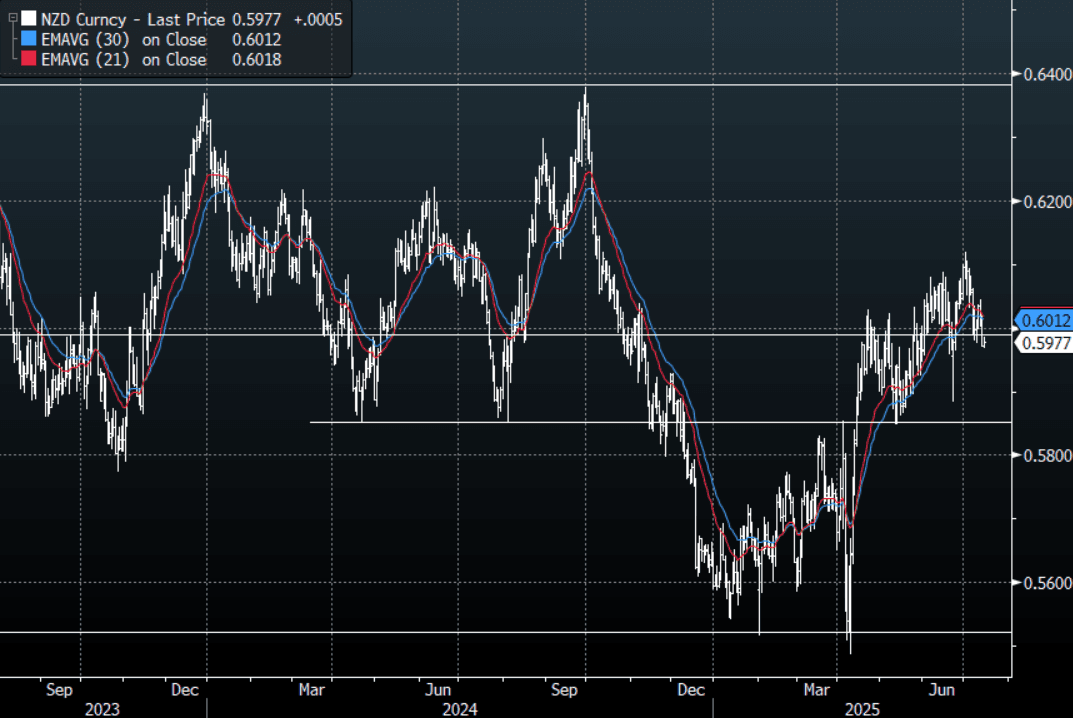

NZD: Asia Wrap - NZD/USD Probing Support Around 0.5980

The NZD/USD had a range of 0.5968 - 0.5986 in the Asia-Pac session, going into the London open trading around 0.5975, +0.08%. Risk got a boost this morning as Nvidia posted on a blog that they had received assurances from the US Government that it would be granted licenses to resume sales of its H20 to China. NZD/USD is again probing its support just below 0.6000, lets see if it can follow through. A break below this support and the market would potentially move back towards the 0.5850/0.5900 area.

- Bloomberg - “Nvidia Corp. plans to resume sales of its H20 artificial intelligence accelerator to China, after it received assurances from the US government that it would be granted licenses, the company said in a blog post.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5932(NZD317m July18).

- CFTC Data shows Asset Managers added slightly to their newly built longs in NZD +9229, the Leveraged community added slightly to their shorts last week -8654.

- AUD/NZD range for the session has been 1.0945 - 1.0967, currently trading 1.0950. The cross has broken out of its recent range and is now trying to push through the more pivotal 1.0950 area. Dips back to 1.0850/1.0900 should now be supported as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Early China/HK Gains Not Sustained, China Property Falls

Sentiment in the tech space was buoyed by early headlines that chip/AI bellwether Nvidia would resume sale of its H20 chip to China (with US government approval). US equity futures rose, led by the Nasdaq (last up around 0.35%), while Hong Kong and China tech sensitive plays were also higher. However, as the afternoon session has progressed, we have moved away from these best levels.

- In China, the aggregate CSI 300 index was up 0.60% at one stage, but at the lunchtime break is now -0.50% weaker. The Shanghai Composite is down 0.93%. Outside of the tech news, we also had Q2 GDP print, which was slightly better than forecast (y/y growth holding above 5%). Monthly June activity data saw Industrial production beat, but retail sales, fixed asset investment and property indicators were weaker. Home prices also fell more than in May.

- The CSI 300 real estate index is down 2% at the break. Headlines "CHINA'S URBANISATION IS TRANSITIONING FROM HIGH-SPEED GROWTH TO STEADY DEVELOPMENT- XINHUA" RTRS, crossed a short while ago, which has likely dampened speculation of sharp policy shift in this space (like we saw in 2015 and which was also speculated on late last week). China's Vanke also reported a first half loss.

- In Hong Kong the HSI is still up 0.20%, but is also well off earlier highs. The tech sub is +0.41% at the break, but was much higher in earlier trade.

- Elsewhere, Japan markets are little changed, while the Kospi has ticked down, struggling to hold above 3200 in index terms. The Taiex is up around 0.80% and one of the better performers on the day.

- In SEA trends are fairly modest, with Philippines and Malaysia, but Thailand and Indonesia a touch higher.

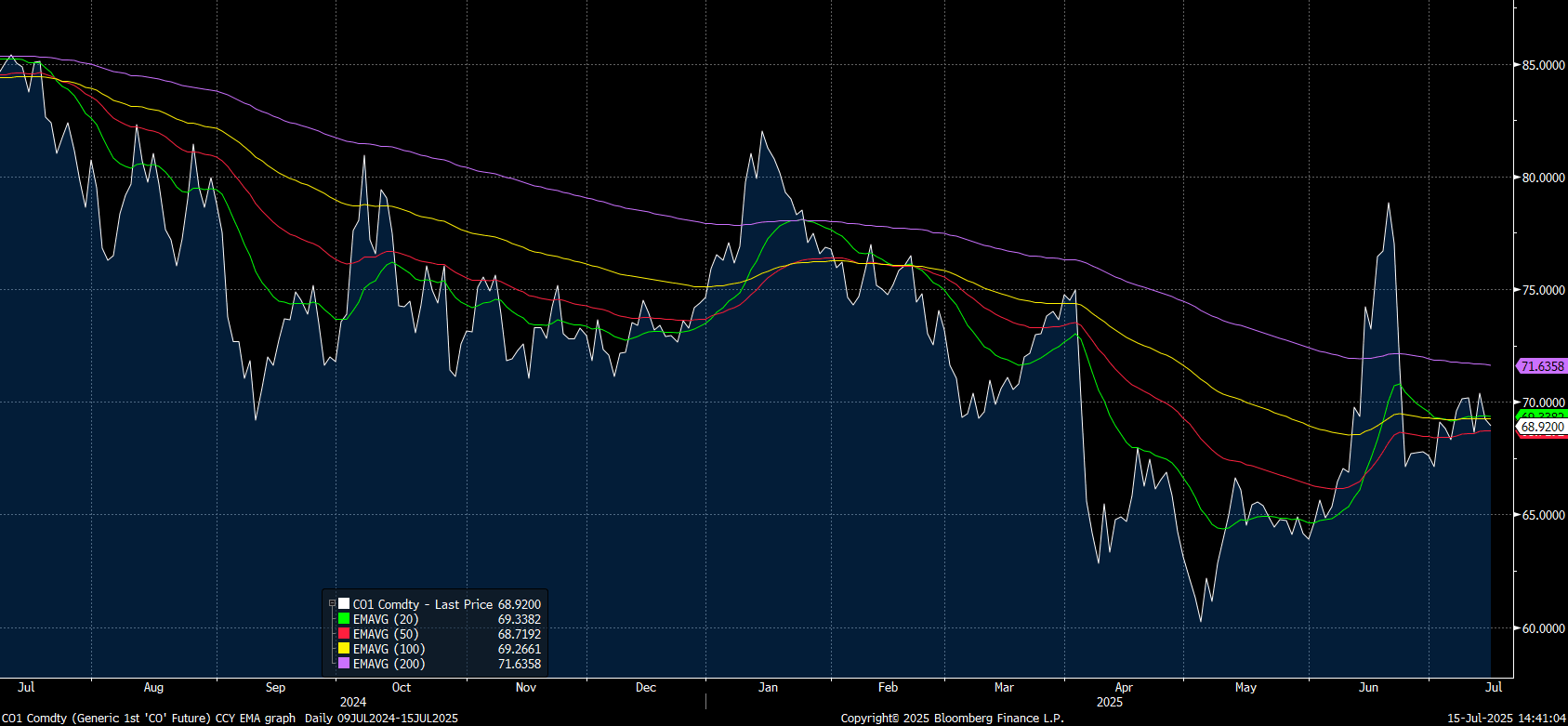

Oil Drops Further as US Pressures Russia

- Oil prices declined Tuesday in the Asia trading day with focus being on President Trumps plan to pressure Russia.

- Trump has floated potential for tariffs on Russia's energy exports, a move that could interrupt supply.

- Despite this, oil fell further today following on from yesterday's significant falls.

- WTI is down -0.36 at US$66.62 bbl

Brent is down -0.28 at US$68.93 bbl and is at the mid-point between the 100-day EMA of $69.26 and the 50-day EMA of $68.71.

source: Bloomberg Finance LP / MNI

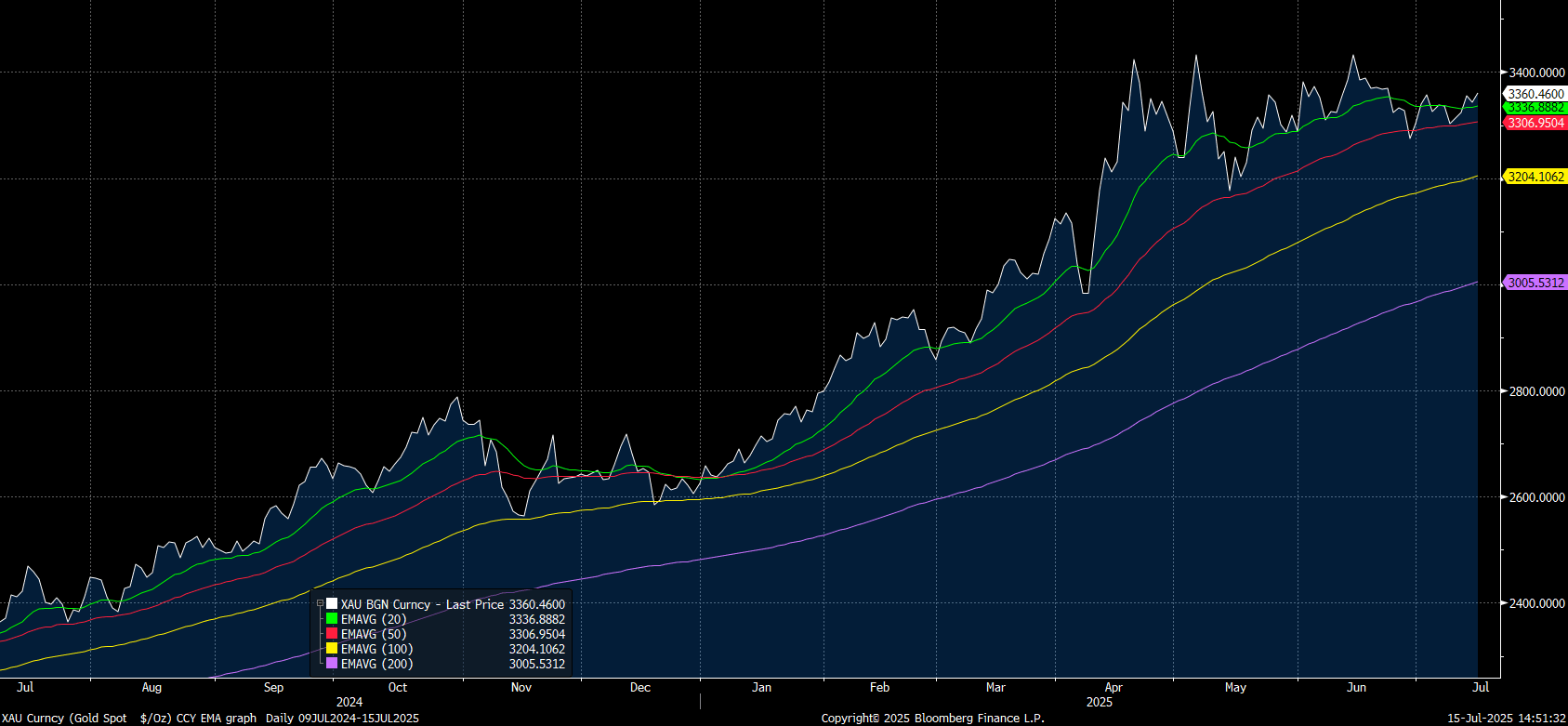

Gold Pares Back Yesterday's Losses

- As President Trump takes aim at Russia, global risk sentiment is challenged.

- This has given gold a boost and it has rallied today in the Asia trading day to take back yesterday's losses.

- At US$3,360.48 gold is not far from its early June year highs and remains in a strong technical position with all major moving averages modestly upward sloping.

Gold sits above all major moving averages, the nearest being the 20-day EMA of $3,336.90.

source: Bloomberg Finance LP / MNI

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 15/07/2025 | 0700/0900 | *** | HICP (f) | |

| 15/07/2025 | 0900/1100 | ** | Industrial Production | |

| 15/07/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/07/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 15/07/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/07/2025 | 1315/0915 | Fed Vice Chair Michelle Bowman | ||

| 15/07/2025 | 1645/1245 | Fed Governor Michael Barr | ||

| 15/07/2025 | 1845/1445 | Boston Fed's Susan Collins | ||

| 15/07/2025 | 2000/2100 | Mansion House: Chancellor Reeves and BOE Bailey | ||

| 15/07/2025 | 2345/1945 | Dallas Fed's Lorie Logan | ||

| 16/07/2025 | 0600/0700 | *** | Consumer inflation report | |

| 16/07/2025 | 0800/1000 | *** | HICP (f) | |

| 16/07/2025 | 0900/1100 | * | Trade Balance | |

| 16/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 16/07/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/07/2025 | 1230/0830 | *** | PPI | |

| 16/07/2025 | 1315/0915 | *** | Industrial Production | |

| 16/07/2025 | 1315/0915 | Cleveland Fed's Beth Hammack |