MNI EUROPEAN OPEN: RBNZ Delivers Hawkish 25Bps Cut

EXECUTIVE SUMMARY

- MIRAN SAYS NO MATERIAL DOWNSIDE TO US 10% UNIVERSAL TARIFF RATE - BBG

- FED'S WILLIAMS SAYS PANDEMIC CHANGED INFLATION PERCEPTIONS - BBG

- BOJ TO WATCH JGB SHORT-END IMPACTS - UEDA - MNI BRIEF

- RBNZ CUTS OCR 25BP TO 3.25% - MNI BRIEF

- AUSSIE MONTHLY CPI EDGES HIGHER AT 2.4% Y/Y - MNI BRIEF

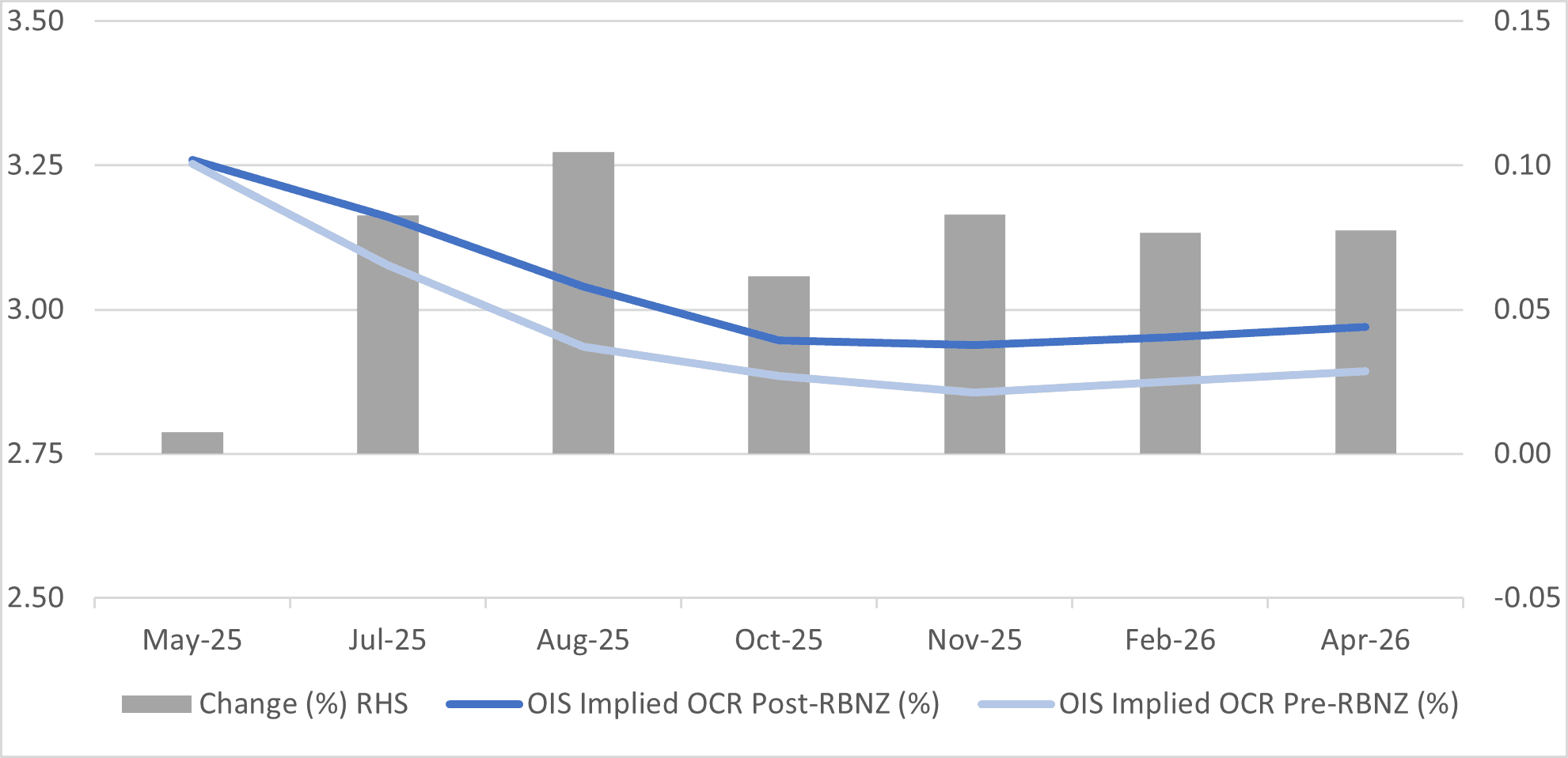

Fig 1: RBNZ Dated OIS Today vs. Pre-RBNZ Levels (%)

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

HOUSING (BBG): “The UK government said it would cut back planning hurdles faced by smaller housebuilders, as Prime Minister Keir Starmer seeks to deliver on his target of building 1.5 million new homes.”

EU

ECB (MNI INTERVIEW): Risk Rising Of Sub-2% ECB Rates-Malta's Demarco

ECB (MNI BRIEF): The European Central Bank is on the path to 2% inflation, but high levels of economic and geopolitical uncertainty, coupled with more sensitive inflation expectations, mean nothing has been decided ahead of the ECB’s next decision, Joachim Nagel said in a speech on Tuesday. (see MNI SOURCES: Risks Tilt To Downside As ECB Mulls Path Below 2% )

ECB (BBG): “ European Central Bank Chief Economist Philip Lane said inflation will hover around 2% for the rest of the year, but the impact of US tariffs on medium-term price pressures will determine monetary policy.”

UKRAINE (POLITICO): “German Chancellor Friedrich Merz wanted to use Ukrainian President Volodymyr Zelenskyy’s visit to Berlin on Wednesday to project resolve in the face of Russia’s escalating war on Ukraine. Instead, the chancellor is under fire from within his own ranks over unclear statements he made this week on whether Germany is prepared to provide Ukraine with long-range Taurus missiles that could strike deep into Russian territory.”

UKRAINE (BBC): “Russian forces are making gains in the Ukrainian north-eastern region of Sumy - a development that may be linked to Moscow's attempts to create "buffer zones" along the border, Ukrainian regional authorities have said.

US

GOVERNMENT (BBG): “President Donald Trump says that the government would retain guarantees and an oversight role over Fannie Mae and Freddie Mac even as he pursues a public offering for the mortgage giants.”

TARIFFS (BBG): “White House Council of Economic Advisers Chair Stephen Miran said that while it’s not yet determined where US tariff rates will end up, the 10% universal baseline surtax isn’t big enough “to have any adverse consequences in the economy.””

FED (BBG): "Federal Reserve Bank of New York President John Williams said pandemic-era price shocks changed American consumers’ inflation perceptions, and policymakers can’t take for granted that people’s estimates of future price increases will remain anchored. "

OTHER

CANADA (MNI): King Charles played up Canada's sovereignty in a Throne Speech in Ottawa Tuesday, backing Prime Minister Mark Carney's rejection of Donald Trump's comments about using economic force to bring trade concessions followed by turning America's northern neighbor into the 51st State.

JAPAN/US (RTRS): “ Japan has proposed purchasing billions of dollars worth of U.S. semiconductor products during ongoing tariff negotiations with the United States, the Asahi newspaper reported, citing an unidentified source.”

JAPAN (MNI BRIEF): The Bank of Japan must remain attentive to the risk that rising yields on super-long Japanese government bonds (JGBs) could spill over to medium- and short-term yields, which more directly influence the economy, Governor Kazuo Ueda told lawmakers Wednesday.

AUSTRALIA (MNI BRIEF): Australia’s monthly CPI indicator rose 2.4% y/y in April, slightly above expectations, with the trimmed mean also ticking up to 2.8%, Australian Bureau of Statistics data showed Wednesday.

AUSTRALIA (BBG): “Australia gave preliminary approval to extend the life of its biggest and oldest liquefied natural gas plant for decades, potentially creating billions of dollars in new drilling opportunities but raising questions about the nation’s climate agenda.”

NEW ZEALAND (MNI BRIEF): The Reserve Bank of New Zealand’s Monetary Policy Committee cut the Official Cash Rate by 25 basis points to 3.25% on Wednesday, citing significant spare capacity in the economy.

CHINA

MANUFACTURING (ECONOMIC DAILY): “China must ensure GDP has a reasonable proportion of manufacturing value added by promoting industrial upgrading and strengthening independent innovation, said the Economic Daily in a commentary.”

CHINA (MOFCOM): “Sino-U.S. economic and trade relations are expected to improve despite periodic fluctuations, according to Peng Bo, a researcher at the Institute of International Trade and Economic Cooperation at the Ministry of Commerce.”

CHINA MARKETS

MNI: PBOC Net Injects CNY58.5 Bln via OMO Wednesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY215.5 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY58.5 billion after offsetting the maturities of CNY157 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.5493% at 09:48 am local time from the close of 1.6186% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Tuesday, compared with the close of 46 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1894 Weds; +0.71% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1894 on Wednesday, compared with 7.1876 set on Tuesday. The fixing was estimated at 7.2014 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND APRIL FILLED JOBS -0.1% M/M; MAR. +0.1%

AUSTRALIA APRIL CONSUMER PRICES +2.4% Y/Y; EST. 2.3%; MAR. +2.4%

AUSTRALIA APRIL TRIMMED MEAN CPI +2.8% Y/Y; MAR. +2.7%

AUSTRALIA Q1 TOTAL CONSTRUCTION UNCHANGED Q/Q; EST. 0.5%; Q4 +0.9%

SOUTH KOREA MAY MANUFACTURERS' CONFIDENCE 94.7; APR. 93.1

SOUTH KOREA MAY NON-MANUFACTURERS' CONFIDENCE 88.1; APR. 84.5

SOUTH KOREA APR RETAIL SALES +7.0% Y/Y; MAR. +9.2%

SOUTH KOREA APR DEPT STORE SALES -2.9% Y/Y; MAR. -2.1%

SOUTH KOREA APR DISCOUNT STORE SALES -3.1% Y/Y; MAR. -0.2%

SOUTH KOREA SHORT-TERM DEBT Q1 $149.3B; Q4 $146.5B

MARKETS

US TSYS: Asia Wrap - 2s10s Steepens

The TYM5 range has been 110-09 to 110-15 during the Asia-Pacific session. It last changed hands at 110-09, down 0-07 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.965%, down 0.02 from its close.

- The US 10-year yield has edged higher, dealing around 4.467%, up 0.02 from its close.

- This has seen the yield curve steepen in Asia - 2s10s +3.73 at 49.583.

- (Bloomberg) “The JGB 40-year sale has come in weak after all. The bid-to-cover dropped back to 2.21, the weakest since July. And the yield of 3.135% is above the poll estimate of 3.085%. That global bond bounce may fade.”

- “The Fed’s Tom Barkin said elevated uncertainty has led businesses to freeze hiring and hold off on future investment decisions. Neel Kashkari said there’s a “healthy debate” among policymakers about whether to look through the inflation effect of tariffs as a transitory shock, or a lasting issue.”(BBG)

- " FED'S WILLIAMS: WE HAVE TO BE VERY AWARE THAT INFLATION EXPECTATIONS COULD SHIFT IN ANY WAYS THAT COULD BE DETRIMENTAL - [RTRS]

- The 10-year look likely to see supply on any dips in yield in the short-term, should yields hold above 4.35/40% the target looks to be the 4.75% area. Watch for any announcements though relating to the SLR, this could have an impact on a market that is already quite short.

JGBS: Aggressive Bear-Steepener After Poor 40Y Auction

JGB futures are sharply weaker and at Tokyo session lows, -68 compared to settlement levels, after today’s 40-year auction displayed poor demand metrics.

- Demand for today’s 40-year bond issuance was notably weak, with the high yield clearing well above dealer expectations. According to a Bloomberg survey, the market anticipated a yield of 3.085%, while the actual result came in at 3.135%.

- The auction’s cover ratio declined sharply to 2.2114x, down from 2.9203x at the previous issuance and marking the weakest demand since July 2024.

- Given the combination of elevated yield and weak demand metrics, today’s result is likely to be regarded as very poor. In afternoon trading, the 40-year yield is dealing 8bps higher versus pre-auction levels.

- Cash US tsys have modestly bear-steepened in today's Asia-Pac session, with yields flat to 3bps higher.

- Cash JGBs are 2-8bps cheaper, with a steeper curve.

- The swaps curve has bear-steepened, with rates 3-8bps higher. Swap spreads are wider.

- Tomorrow, the local calendar will see International Investment Flow and Consumer Confidence data alongside BoJ Rinban Operations covering 3-25-year JGBs.

AUSSIE BONDS: Cheaper But Limited Reaction To CPI Data

ACGBs (YM -4.0 & XM -3.0) are modestly mixed after the release of April CPI data.

- April headline inflation was unchanged at 2.4% y/y, slightly higher than expected, while the trimmed mean picked up 0.1pp to 2.8% y/y. The focus is on the latter as the headline is likely to be impacted by government electricity rebates until year-end. Underlying inflation has been sitting around 2.7/2.8% since December, and the RBA expects 2.6% for Q2, which is released on July 30.

- Cash US tsys have bear-steepened in today's Asia-Pac session, with yields flat to 3bps higher.

- Cash ACGBs are 3bps cheaper on the day, with the AU-US 10-year yield differential at -14bps.

- Swap rates are 1-3bps higher after the CPI data.

- The bills strip has cheapened after the data, leaving pricing -3 to -6 across contracts.

- RBA-dated OIS pricing is 1-4bps firmer across meetings after the data. A 25bp rate cut in July is given a 64% probability (70% pre-data), with a cumulative 73bps (70bps pre-data) of easing priced by year-end.

- Tomorrow, the local calendar will see Q1 Private Capital Expenditure data.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Friday.

BONDS: NZGBS: Bear-Flatter After RBNZ Hawkish Cut

NZGBs closed 4-9bps cheaper, with a flatter curve.

- The RBNZ cut rates 25bp to 3.25% following a vote that included an option to leave rates unchanged. The vote wasn’t unanimous, with one dissenter. Despite this, the OCR path was revised down to show a trough 25bp below February’s at 2.85%.

- In his first press conference as Governor, Hawkesby noted that this was the first vote on the direction of rates in two years—something that typically occurs at inflection points and highlights the current high level of uncertainty. With policy rates now in the “neutral zone,” he emphasised that the MPC is positioned to “respond to developments as they occur,” indicating that further easing is not guaranteed and future moves will depend on incoming data and the evolving outlook.

- Swap rates closed 7-10bps higher.

- RBNZ-dated OIS pricing closed 6-10bps firmer across meetings versus pre-RBNZ levels. Markets had fully priced in today’s 25bp cut ahead of the decision. A total of 32bps of easing is now expected by November 2025.

- Tomorrow, the local calendar will see the RBNZ Governor in front of the Parliament Select Committee on MPS. ANZ Business Confidence is also scheduled for release.

- The NZ Treasury also plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-36 bond.

NZD: Asia Wrap - NZD Bounces On A Hawkish Cut

The NZD/USD had a range of 0.5924 - 0.5980 in the Asia-Pac session, going into the London open trading around 0.5960. The NZD has bounced pretty hard with the RBNZ being surprisingly hawkish suggesting that they are pretty close to neutral now.

- The RBNZ decision, has aided NZD, with the 25bps cut and lowered OCR projection offset by the non-unanimous decision. This hints further cuts may be harder to come by, while Governor Hawkesby wouldn't be drawn on the policy bias at the next meeting, with central bank well placed to respond to developments. RBNZ officials also note the new OCR of 3.25% is in the neutral zone.

- "RBNZ GOV HAWKESBY: HAVE LOWERED RATES A CONSIDERABLE WAY, STILL WORKING WAY THROUGH - [RTRS]"

- "RBNZ'S CONWAY: OCR AT 3.25% IS `INTO NEUTRAL ZONE'" - BBG.

- The NZD has bounced across the board on the back of this and expect this price action to continue as shorts that had been added to hoping for a more dovish outcome are pared back.

- The NZD continues to trade in a 0.5850/0.6050 range, another failure above 0.6000 and with corporate month-end in play be on the lookout for more demand of USD’s over the next day or 2.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here could provide the spark for the next leg higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5725(NZD1.09b). Upcoming Close Strikes : 0.5975(NZD400m May 29)

AUD/NZD range for the session has been 1.0779 - 1.0851, currently trading 1.0790. A sustained break above 1.0930 is needed to turn the focus higher, until then expect supply on bounces. It traded up to a high around 1.0851 just before the RBNZ, but has subsequently dropped lower as the RBNZ suggests they are close to neutral. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone today and AUD/NZD should now see supply on bounces. The first target is around 1.0650.

Fig 1: AUD/NZD Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - AUD Stays Under Pressure

The AUD/USD has had a tight range of 0.6426 - 0.6454 in the Asia- Pac session, it is currently trading around 0.6430 drifting down back towards the days lows.

- April headline inflation was unchanged at 2.4% y/y, slightly higher than expected, while the trimmed mean picked up 0.1pp to 2.8% y/y. The focus is on the latter as headline is likely to be impacted by government electricity rebates until year end.

- We head into the corporate month-end and this could see more demand for USD’s over the next day or 2.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6325(AUD430m). Upcoming Close Strikes : 0.6400(AUD 556m June 2), 0.6500(AUD 532m May 30)

AUD/JPY - Today's range 92.75 - 93.23, it is trading currently around 93.00. The pair has again found supply above the 93.00 area in today's session, a break back above 93.50 could see the focus return once more to the 95/96 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

JPY: Asia Wrap USD/JPY - A Whippy Session With An Underlying Bid

The Asia-Pac USD/JPY range has been 143.85 - 144.77, Asia is currently trading around 144.35. USD/JPY has had a very whippy session with a big spike seen into the Japanese Fix, it drifted lower from there but bounced again in our afternoon to make a new high around 144.77.

- " Regarding a recent spike in super-long yields on government debt, market participants cited the unwinding of existing positions and a drop in demand, Bank of Japan Governor Kazuo Ueda says. Moves in short- and long-term yields tend to affect the economy more than those in super long-term yields. Will monitor market developments closely along with their economic impact by keeping in mind that major moves in super long-term yields can affect shorter-term yields." (per BBG)

- "A Japanese government advisory panel is urging authorities to intensify fiscal consolidation efforts, according to Bloomberg News on Tuesday, citing a proposal submitted to Finance Minister Katsunobu Kato on the same day. This comes as the Bank of Japan's ongoing monetary tightening increases the risk of higher debt-servicing costs for the nation, said the news wire." (per MTN)

- (Bloomberg) - “The JGB 40-year sale has come in weak after all. The bid-to-cover dropped back to 2.21, the weakest since July. And the yield of 3.135% is above the poll estimate of 3.085%. That global bond bounce may fade.”

- This move yesterday would have caught out a few shorts, but we are approaching resistance back towards 145.00/146.00 which should see some sellers emerge.

- It is worth noting though we are heading into the corporate month-end and this could see some USD demand over the next day or 2 making it uncomfortable for the considerable JPY longs that have been built up.

- The market has been very confident of a move lower in USD/JPY but with positioning quite large now the risk of pullbacks does increase. Resistance is now back towards 145.00/146.00 area first up.

Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($2.14b), 143.00($1.98b), 144.00($1.67b). Upcoming Close Strikes : 143.00($3.34b May 30), 140.00($2.78b May 30).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

FOREX: Asia FX Wrap - USD Keeps Its Bid Tone

The BBDXY has had a range of 1215.25 - 1219.21 in the Asia-Pac session, it is currently trading around 1218. “The Fed’s John Williams said policymakers should focus on anchoring not just long-term price expectations, but “the whole curve” to prevent inflation from becoming persistent or permanent”(BBG). “The ECB’s Philip Lane said inflation will hover around 2% for the rest of the year. The impact of US tariffs on medium-term price pressures will determine monetary policy, he told the FAZ.”(BBG)

- EUR/USD - Asian range 1.1301 - 1.1345, Asia is currently trading 1.1305. EUR has drifted lower for most of the Asian session. It is worth noting that we are heading into the corporate month-end and this could see some USD demand over the next day or 2. Dips back to 1.1200 are expected to be supported.

- GBP/USD - Asian range 1.3473 - 1.3522, Asia is currently dealing around 1.3470. The GBP is struggling to hold above the pivotal 1.3500 area for now, looking for support to return back towards the 13300/3400 area which could be seen if the corporate USD demand materializes.

- USD/CNH - Asian range 7.1868 - 7.1993, the USD/CNY fix printed 7.1894. Asia is currently dealing around 7.1950. Sellers should be found on a bounce back towards the 7.2200 area again. Andreas Steno Larsen on X : The elephant in the room. USDCNH needs to go to 6.80 at least. https://x.com/AndreasSteno/status/1926115935200440525

- Cross asset : SPX -0.10%, Gold $3297, US 10-Year 4.47%, BBDXY 1218, Crude oil $61.19

Data/Events : Fra GDP & PPI, Ger Unemployment, ECB CPI Expectations

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: KOSPI Leads the Way whilst Others are in Holding Pattern

Ahead of tomorrow’s decision by the BOK, the Kospi in South Korea was the regional outperformer as it achieves new highs for 2025 as large cap chipmakers join value stocks in the run up to next week’s election. Shares of holding companies continue to perform as pushes to reform the corporate structure grow louder.

Chinese bourses did very little today as volatility remains low in the region's largest economy as investors wait for the next update on tariff discussions. BYD fell in Hong Kong for a third day straight on concerns of discounting. BYD is down over -2.00% today and down over 12% for the week, weighing heavy on the Hang Seng and other EV related stocks.

- The Hang Seng is down today by -0.55% and trading very heavy for the week. The CSI 300 is up a mere +0.09%, Shanghai Comp +0.07% and Shenzhen down -0.12%.

- The KOSPI is the regional outperformer today, rising +1.66% easily wiping out yesterday's modest losses.

- The fact that the FTSE Malaysia KLCI was flat today will come as welcome relief given falling nine of the last 12 trading days.

- The Jakarta Composite did very little today also yet remains up over 6% month to date making it the best performer of the major markets.

- In Singapore the Straits Times is up +0.50% whilst the PSEi in the Philippines is up +1.40%.

- The NIFTY 50 closed lower by -0.70% yesterday and carried that over to today and is currently down -0.25%

OIL: Crude Range Trading Ahead Of Key Events, FOMC Minutes Later

Oil prices are moderately higher today after falling around 0.7% on Tuesday. They are range trading as the market waits for key US data on Friday and the outcome of OPEC’s May 31 meeting. WTI is up 0.5% to $61.20/bbl after a high of $61.43, while Brent is 0.5% higher at $64.40/bbl off the intraday low of $64.32. The US dollar continues to strengthen with the USD index up 0.15%.

- With OPEC expected to increase output again in July adding to global excess supply, attention will remain on US inventory data with industry-based figures out later today and the official EIA report on Friday, delayed because of Monday’s US holiday which marked the start of the driving season. Gasoline demand will be especially monitored during this time.

- OPEC’s Joint Ministerial Monitoring Committee meets virtually today to discuss quotas for July and then a smaller group led by Saudi Arabia will decide on May 31.

- It seems that sanctions on Russia’s fossil fuel exports are not only going to stay but may tighten with Europe already increasing restrictions and considering others, while the US is also seriously thinking about adding to its list. Russian attacks on Ukraine have intensified despite calls for a truce.

- Later the Fed’s Williams and Kashkari speak as well as the May FOMC meeting minutes are released. US May Richmond & Dallas Fed indices as well as German April unemployment and French April consumption are released. BoE’s Pill also speaks.

GOLD: Stronger Greenback Continues To Pressure Gold

Gold prices are down slightly during today’s APAC trading after falling 1.3% on Tuesday. They are down 0.1% to $3296.60 as the strengthening US dollar continues to weigh (USD BBDXY +0.1%) while equity and commodity prices are mixed. Bullion rose to $3315.81 early in the session before falling to $3291.79.

- Gold is trading in a narrow range as markets wait for news on the progress of trade negotiations and key US data out on Friday, especially PCE prices. US April durable orders were better than expected and the Dallas Fed manufacturing index improved substantially. It is also sensitive to geopolitical developments that may shift safe-haven flows.

- Equities have been mixed with the S&P e-mini down 0.1% and Hang Seng -0.6% but Nikkei up 0.3% and Kospi +1.7%. Oil prices are higher with the WTI +0.6% to $61.24. Copper is down 0.6% though. Silver is little changed at around $33.26.

- Later the Fed’s Williams and Kashkari speak as well as the May FOMC meeting minutes are released. US May Richmond & Dallas Fed indices as well as German April unemployment and French April consumption are released. BoE’s Pill also speaks.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 28/05/2025 | 0600/0800 | ** | Retail Sales | |

| 28/05/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 28/05/2025 | 0645/0845 | ** | PPI | |

| 28/05/2025 | 0645/0845 | *** | GDP (f) | |

| 28/05/2025 | 0645/0845 | ** | Consumer Spending | |

| 28/05/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/05/2025 | 0755/0955 | ** | Unemployment | |

| 28/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kahkari | ||

| 28/05/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/05/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/05/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/05/2025 | 1500/1600 | BOE's Pill on monetary policy panel at Austria National Bank / SUERF | ||

| 28/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 28/05/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/05/2025 | 1800/1400 | FOMC Minutes | ||

| 28/05/2025 | 1800/1400 | *** | FOMC Minutes | |

| 28/05/2025 | 0000/2000 | New York Fed's John Williams | ||

| 29/05/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 29/05/2025 | 0900/1000 | BOE's Breeden opening remarks at conference on non-bank financial sector and financial stability | ||

| 29/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 29/05/2025 | 1230/0830 | * | Current account | |

| 29/05/2025 | 1230/0830 | * | Payroll employment | |

| 29/05/2025 | 1230/0830 | *** | GDP | |

| 29/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin |