MNI EUROPEAN OPEN: Official Comments Drive USD/JPY Lower

EXECUTIVE SUMMARY

- ECB TO HOLD AGAIN, STILL IN ‘GOOD PLACE’ - MNI ECB WATCH

- BESSENT, JAPAN'S KATAYAMA DISCUSSED FISCAL MEASURES, VOLATILITY - BBG

- MNI DISCUSSES THE BOJ’S HIKE PATH AMID SLUGGISH UNDERLYING CPI - MNI POLICY

- CHINA SIGNS UPGRADED ASEAN 3.0 FTA - MNI BRIEF

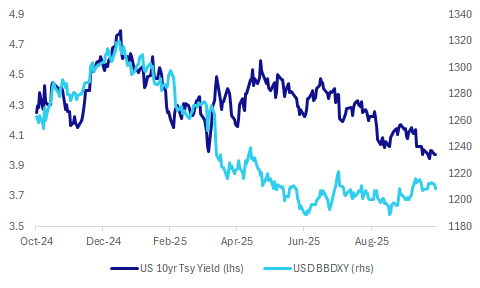

Fig 1: USD BBDXY & 10yr US Tsy Yield Trends

Source: Bloomberg Finance L.P./MNI

UK

BUDGET (BBC): “Reeves did not rule out the possibility of tax rises when asked if she was considering them ahead of the Budget, adding that economic growth would be "a big part of the Budget story".”

ECONOMY (TIMES): “Ministers will not row back on Labour’s workers’ rights overhaul before new laws come into force, as businesses fear they will be betrayed by promises that changes could be made at a later date.”

FOOD PRICES (BBG): “ UK food bills have dropped at their sharpest rate in almost five years, dragged down partly by the global easing in sugar prices.”

UKRAINE (BBG): “ UK Prime Minister Keir Starmer said the prospects for Ukraine are improving after President Donald Trump imposed sanctions on Russian oil, a sign Kyiv’s allies are cautiously optimistic that a hardening US stance could damage the Kremlin’s ability to sustain its war.”

GROWTH (BBG): “Chancellor of the Exchequer Rachel Reeves’ attempt to boost growth by luring in private investment through the National Wealth Fund will be held back by its limited size, according to an influential group of British lawmakers.”

EU

ECB (MNI ECB WATCH): The European Central Bank is set to hold its deposit rate at 2% for a third consecutive meeting on Thursday, continuing in wait and see mode with only limited new sets of data available ahead of the gathering.

FRANCE (BBG): “- France’s National Assembly adopted an amendment on Monday that would increase taxes on the country’s largest companies next year, part of the government’s effort to rein in the deficit and find compromises with opposition lawmakers.”

RUSSIA (POLITICO): “In a statement on Monday evening, Moscow-headquartered energy giant Lukoil confirmed it had begun looking for buyers for its foreign ventures. The decision, it said, had been taken "owing to introduction of restrictive measures against the Company and its subsidiaries by some states.”

NETHERLANDS (DUTCHNEWS): “Opinion polls suggest the Dutch general election on Wednesday will be an extremely close-run thing, with five parties all within a few seats of each other. The latest EenVandaag/Verian poll has the far-right PVV on 34 seats in the 150-seat lower house of parliament, while Peil.nl, compiled by Maurice de Hond, puts the party on 29 seats and Ipsos/I&O on 26. The three polling organisations give the GroenLinks-PvdA alliance 25, 24 and 23 seats respectively, and the Christian Democrats 23, 22 and 20.”

SPAIN (POLITICO): “Catalan separatists voted to sever ties with Spanish Prime Minister Pedro Sánchez’s Socialists, further weakening his minority government. The break is dire for Sánchez, whose government has no hope of passing legislation without the support of Junts’ lawmakers. The prime minister has not been able to get a new budget approved since the start of this term and has instead governed with extensions of the 2022 budget and EU recovery cash.”

US

JOBS (RTRS): “Amazon is planning to cut as many as 30,000 corporate jobs beginning on Tuesday, as the company pares expenses and compensates for overhiring during the peak demand of the pandemic, according to three people familiar with the matter.”

FED (MNI INTERVIEW): The positive U.S. growth surprise and above-target inflation may discourage the Federal Reserve from lowering interest rates for a third straight meeting in December, former Atlanta Fed President Dennis Lockhart told MNI.

US/JAPAN (BBG): “President Donald Trump hailed the US’s alliance with Japan, reaffirming ties with a longstanding partner and praising new Prime Minister Sanae Takaichi on her plans to ratchet up defense spending as the pair met in Tokyo.”

OTHER

JAPAN (MNI POLICY): MNI discusses the BOJ's hike path amid sluggish underlying CPI. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (BBG): "Treasury Secretary Scott Bessent “was glad to hear the Minister’s perspective on Japanese fiscal measures under consideration, and expressed his eagerness to learn more as the full package is worked out so as to better understand the potential impact.”"

JAPAN (BBG): "US Treasury Secretary Scott Bessent refrained from weighing deeply into Bank of Japan monetary policy in talks, according to his Japanese counterpart Satsuki Katayama, despite having previously describe the BOJ as “behind the curve” on inflation."

SOUTH KOREA (BBG): “The Bank of Korea plans to consider additional gold purchases from a medium- to long-term perspective,” said Heung-Soon Jung, director of the Reserve Investment Division, Reserve Management Group.”

CHINA

TRADE (MNI BRIEF): China has officially signed an upgraded Free Trade Agreement (FTA) with ASEAN nations, according to the Ministry of Commerce on Tuesday. The FTA 3.0 upgrade encompasses nine key areas such as the digital economy, green economy, supply chain connectivity and customs procedures and trade facilitation. The upgraded agreement reflects a shared resolve among members to collaborate on addressing global trade and economic challenges, the ministry said.

HOUSING (SECURITIES DAILY): "More than 20 cities have introduced supportive measures since October to boost housing demand and promote the stable, healthy development of the real estate market, according to a report by Securities Daily."

MNI: PBOC Net Injects CNY315.8 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY475.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY315.8 billion after offsetting maturities of CNY159.5 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.4781% at 09:52 am local time from the close of 1.5818% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Monday, compared with the close of 53 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0856 Tues; -0.19% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0856 on Tuesday, compared with 7.0881 set on Monday. The fixing was estimated at 7.1031 by Bloomberg survey today.

MARKET DATA

UK OCT. BRC SHOP PRICE INDEX +1% Y/Y; EST. +1.6%; SEP. +1.4%

NEW ZEALAND SEPT. FILLED JOBS +0.3% M/M; AUG. +0.1%

SOUTH KOREA Q3 GDP +1.2% Q/Q; EST. +1.0%; Q2 +0.7%

SOUTH KOREA Q3 GDP +1.7% Y/Y; EST. +1.5%; Q2 +0.6%

SOUTH KOREA OCT. CONSUMER CONFIDENCE 109.8; SEP. 110.1

MARKETS

US TSYS: Quiet Day as Curves Modestly Flatter

Despite weakness across major equity bourses, US bond futures didn't see a lead in with TYZ5 posting only modest gains. Up +02 at 113-15+ the the 10-Yr price action was muted as volumes remained modest throughout the trading day.

Cash volumes were light also, capping yield moves.

- The US 2-Yr is 3.499% (+0.4bp)

- The US 5-Yr is 3.607% (+0.3bp)

- The US 10-Yr is 3.979% (-0.4bps) as it consolidates below the 4.00% recent range bottom.

- The US 30-Yr is 4.551% (-0.3bp)

Focus for markets tonight will be US$69bn 2-Yr auction, US$70bn 5-Yr auction and various bill auctions.

Economic Data focus is on :

10/28/2025 9:00 FHFA House Price Index MoM (-0.1%, -0.1%)

10/28/2025 9:00 S&P Cotality CS 20-City MoM (-0.07%, -0.10%), YoY (1.82%, 1.40%)

10/28/2025 10:00 Richmond Fed Mfg Index (-17, -10)

10/28/2025 10:00 Conf. Board Consumer Confidence (94.2, 93.4)

10/28/2025 10:30 Dallas Fed Services Activity (-5.6, --)

JGBS: Futures Firmer But Under Resistance Level, Back End Yields Off 1-2bps

JGB futures have drifted a little higher, last 136.17, +.21, versus settlement levels, but recent ranges continue to prevail. Dips under 136.00 continue to be supported, but we remain comfortably sub key short term resistance (137.30). A positive bias from US Tsy futures has helped, although likewise in this space, we continue to track within recent ranges (as markets await the FOMC). Cash JGBs are biased lower, led by the 10 and 20yr tenors.

- There has been a lot of focus today on US-Japan meetings, with US President Trump & Japan PM Takaichi headlines crossing today, although remarks were mostly high level. Takaichi reiterated intentions around increased defense expenditure (2% of GDP by March next year), which is a potential fiscal pressure point but hasn't impacted sentiment today.

- The US Tsy also gave a read out of the Tsy Secretary and Japan FinMin meeting, with Bessent emphasizing the need for sound monetary policy to keep inflation expectations anchored and avoid FX volatility. These remarks have helped the yen today.

- Our policy team noted that even with a sluggish underlying inflation backdrop, hike risks are still on the cards from Dec of this year.

- Cash JGB yields see the 10yr back to 1.65% (off 2bps), while the 30yr is again flirting with the 100-day EMA support point, last around 3.07%.

AUSSIE BONDS: Front End Yields Up, Nov RBA Easing Risks Pared, Q3 CPI Tomorrow

Aussie 3yr (YM) bond futures underperformed, last 96.545, off 3.5bps. 10yr futures were up a touch to 95.815. The bias in US Tsy futures has been to nudge higher, support the Aussie 10yr but the 3yr is likely reflecting near term uncertainties around the RBA outlook, with tomorrow's Q3 CPI print in focus. ACGB yields are mixed, as the curve flattens, the front end 3yr establishing itself back above 3.40% (last 3.44%), while the 10yr has drifted lower to 4.165%. This leaves the 3/10s curve at +72bps, flatter by 5bps.

- The AU-US 10yr spread is near +19bps, so back towards the upper ends of its recent range. We see spread compression trades re-emerge above +30bps, but a lot depends on tomorrow's Australian Q3 CPI print.

- Key watch points for CPI tomorrow are as follows: Bloomberg consensus expects trimmed mean to print at 0.8% q/q & 2.7% y/y, which would see a pickup in the 2q/2q annualised rate to 2.8% from 2.6%. This outcome could argue for a hold or a cut dependent on the revised outlook and services inflation result. This week Bullock reiterated that labour data are volatile and while the 0.2pp rise in the September unemployment rate to 4.5% was surprising, it could fall again in October. Thus she would like more information.

- Market pricing has around 10bps of easing priced in for Nov, we were around 16bps at the end of last week. A full cut is priced by the Feb meeting next year.

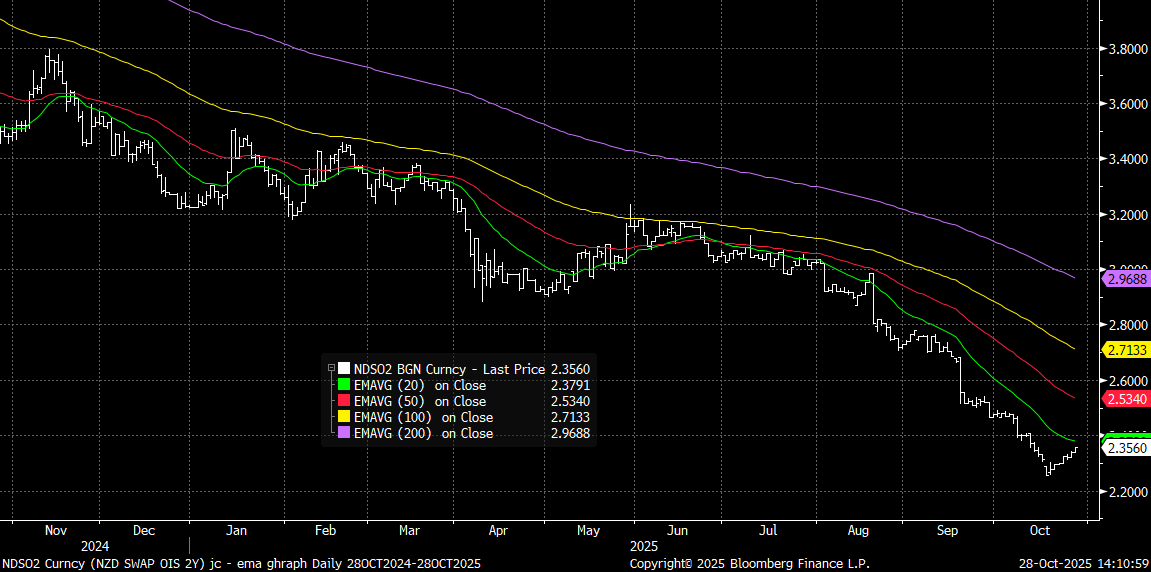

BONDS: NZGBS: 2yr Swap Close To 20-day EMA Resistance, Better Data Helps

NZGB yields have been biased higher as Tuesday trade unfolded, supported by earlier data outcomes. The 2yr is up nearly +2bps to 2.54%, while the 5yr is up near 3bps. The 10yr has seen a more modest rise and is still sub 4.00% at this stage. We are still sub key EMAs, but focus will rest on whether we can test higher. The 2yr swap rate is close to 2.36%, closing in on a test of its 20-day EMA resistance point, see the chart below.

- Earlier data showed Q3 NZ filled jobs rose 0.1% q/q signalling that employment likely stabilised in the quarter after falling 0.1% q/q in Q2. Q3 labour market data print on 5 November and will be an important input into the 26 November RBNZ decision.

- Other data showed NZ’S household living-costs price index (HLPI) for Q3 rose 2.4% y/y, below the CPI at 3.0%, down from 2.6% in Q2 and 3.8% in Q3 2024. It tends to lead real private consumption growth by two to six quarters. The recent trend signals that the tentative recovery in spending growth should continue after Q2’s 1.5% y/y rate.

- RBNZ pricing still has a 25bps cut priced in for the Nov meeting, but OIS dated contracts for 2026 are slightly firmer. For July 2026 we are around 2.18%, against mid Oct lows near 2.00%.

- The NZ 2/10s curve has flattened today, off around 2bps to +146bps. The NZ-US10yr spread is holding above flat, last +3bps.

- Tomorrow, the local data calendar is empty.

Fig 1: NZ 2yr Swap Rate & Key EMAs

Source: Bloomberg Finance L.P/MNI

FOREX: US & Japan Comments Aid USD/JPY Dip, Still Above Key EMAs

Yen has outperformed so far in Tuesday trade, with USD/JPY back testing under 152.00 and up around 0.60% in yen terms so far today. US-Japan meetings have dominated the headlines (with Bessent remarks aiding yen gains), while we also saw some verbal FX jawboning from Japan's economic minister, which has also likely helped at the margins. The BBDXY index is down 0.205 to 1209.15.

- The readout from the meeting between the US Tsy Secretary and the Japan FinMin highlighted: ""Bessent highlighted the “important role of sound monetary policy formulation and communication in anchoring inflation expectations and preventing excess exchange rate volatility, as conditions are substantially different twelve years after the introduction of Abenomics,” (via BBG). So, whilst the upcoming Thursday monetary policy meeting wasn't discussed, Bessent is stating the different macro landscape between now and when Abenomics and that FX volatility will pick up if monetary policy is not conducted properly, which will likely concern the US authorities.

- Still, USD/JPY is some distance from the 50-day EMA, which is still back under 150.00.

- CHF has also risen, last 0.7930/35, up 0.25%. Lower US yields from Monday have also likely aided safe haven gains today. US equity futures are little changed.

- AUD and NZD are higher, although more so the Kiwi. NZD/USD was last 0.5780, looking to establish a base above the 20-day EMA. NZ front yield ends are drifting a little higher, with some data outcomes helping these trends. AUD/USD is a little higher last 0.6560, still above all key EMAs, as focus shifts to tomorrow's key Q3 CPI outcome.

- Later August US S&P Cotality & FHFA house prices, October Richmond & Dallas Fed indices and October Conference Board consumer confidence as well as German November GfK consumer confidence and ECB bank lending survey are released.

ASIA STOCKS: Markets Mixed as Investors Wait for News from APEC Summit

The record period for Asia's major bourses took a breather today ahead of the APEC summit as the world awaits to see what 'deals' are announced. With the focus on a US China pact and further news on the USD$350bn investment fund for Korea investment in the US, China and Korea were among the fallers today. The hopes of a US China trade pact has seen flows into EM funds strengthen with the Vanguard FTSE Emerging Markets ETF has had over $400m of net inflows in recent days with investors seeking to benefit from a cooling of the trade war. This comes despite key markets hitting new all time highs in advance of the APEC summit.

- The KOSPI was one of the biggest fallers of the major markets down -1.25% and back below 4,000.

- The NIKKEI has done very little whereas the major bourses in China have all delivered modest gains with onshore indexes +0.20 - 0.40% higher whilst the HSI did very little.

- The Jakarta Composite fell heavily yesterday and the weakness carried on into today with falls of -0.18%. The losses sees the JCI at 8,106 and dip below the 20-day EMA of 8,126. It has traded below the 20-day EMA only once in the last month, failing to hold losses as buyers returned.

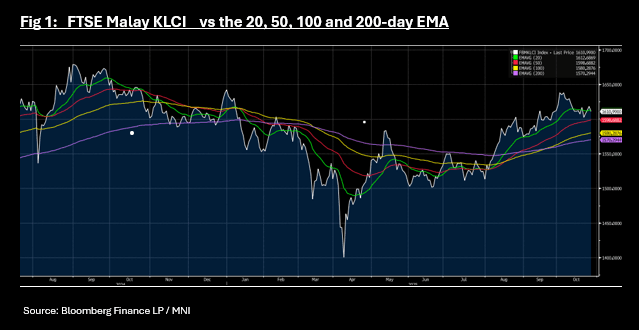

- The FTSE Malay KLCI is one of the biggest fallers, despite the potential for a trade deal that could be imminently announced with the US, as President Trump visits. Malaysia and the US upgraded ties to the highest rung possible, and the two sides pledged to deepen maritime security cooperation at a time when the US and China are competing for influence across the region (per BBG). Down -0.45% today sees the index break below the 20-day EMA which it has tried unsuccessfully to hold below on several occasions this month.

OIL: Crude Steady On Excess Supply Concerns But Monitoring Sanctions Impact

Oil prices are steady in today’s APAC session after being little changed on Monday as the market looks to Wednesday’s Fed decision and Sunday’s OPEC meeting. There are conflicting forces with the market continuing to worry about excess supply with seaborne crude elevated but also aware that the latest US/EU sanctions on Russia could cause disruption as well as increase demand for non-Russian crude. Thus oil could range trade while waiting for new supply/demand developments. Both Brent and WTI are down only slightly in October.

- WTI is down 0.1% to $61.24/bbl after reaching an intraday low of $61.10. Initial support is at $59.64, 23 October low, and resistance at $62.59, 24 October high. Moves higher appear to be corrective.

- Brent has been trading between initial support at $63.86, 24 October low, and resistance at $66.78, 24 October high. The benchmark is little changed at $65.64/bbl after falling 0.5% on Monday but remains above the 50-day EMA at $65.15.

- Russia’s Lukoil is looking to sell its overseas interests following the latest sanctions and Germany has asked for a delay to allow Rosneft to deal with its German assets.

- OPEC meets on Sunday to decide the December output target which could rise again, although there is little spare capacity outside Saudi Arabia. With supply an ongoing concern inventory data will continue to be monitored. US industry-based figures are released on Tuesday.

- Later August US S&P Cotality & FHFA house prices, October Richmond & Dallas Fed indices and October Conference Board consumer confidence as well as German November GfK consumer confidence and ECB bank lending survey are released.

Gold Range Trading Ahead Of October Fed Decision

Gold range traded during today’s APAC session with breaks above $4000 continuing to be temporary. Prices have just dipped and are down 0.3% to $3970.0 after a high of $4019.68 and intraday low at $3964.01. It found some support from the weaker US dollar (BBDXY -0.2%) while US yields are steady. There was little news to drive safe-haven flows in either direction ahead of Wednesday’s Fed decision.

- Gold has held above support at $3944.9, 9 October low, but remains well below initial resistance at $4186.4, 17 October low. Bullion continues to be in overbought territory despite the recent correction.

- Central bank buying, especially from the PBoC, has provided medium-term support to gold prices and this is generally expected to continue. In line with this, the Bank of Korea said today that it is considering extra purchases for its reserves over the medium- to long-term which would be the first time in 10 years.

- Silver is down 0.3% to $46.68 and has also been in a narrow range between $46.620 and $47.227, below initial support at $47.55, 22 October low. The trend also remains overbought and the current decline is seen as corrective.

- Equities are mixed with the S&P e-mini flat, KOSPI down 1.2% but CSI 300 up 0.2%. Oil prices are lower with WTI -0.2% to $61.16/bbl. Copper is down 0.6%.

- Later August US S&P Cotality & FHFA house prices, October Richmond & Dallas Fed indices and October Conference Board consumer confidence as well as German November GfK consumer confidence and ECB bank lending survey are released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 28/10/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 28/10/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 28/10/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 28/10/2025 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 28/10/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 28/10/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 28/10/2025 | - | FOMC Meeting | ||

| 28/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/10/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 28/10/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/10/2025 | 1400/1000 | ** | housing vacancies | |

| 28/10/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 28/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/10/2025 | - | Bank of Japan Meeting | ||

| 29/10/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 29/10/2025 | 0030/1130 | *** | CPI Inflation Monthly | |

| 29/10/2025 | 0030/1130 | *** | CPI inflation | |

| 29/10/2025 | 0700/0800 | Flash Quarterly GDP Indicator | ||

| 29/10/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 29/10/2025 | 0800/0900 | *** | GDP (p) | |

| 29/10/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 29/10/2025 | 0930/0930 | ** | BOE M4 | |

| 29/10/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 29/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 29/10/2025 | 1100/1200 | ** | PPI | |

| 29/10/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/10/2025 | 1345/0945 | *** | Bank of Canada Policy Decision |