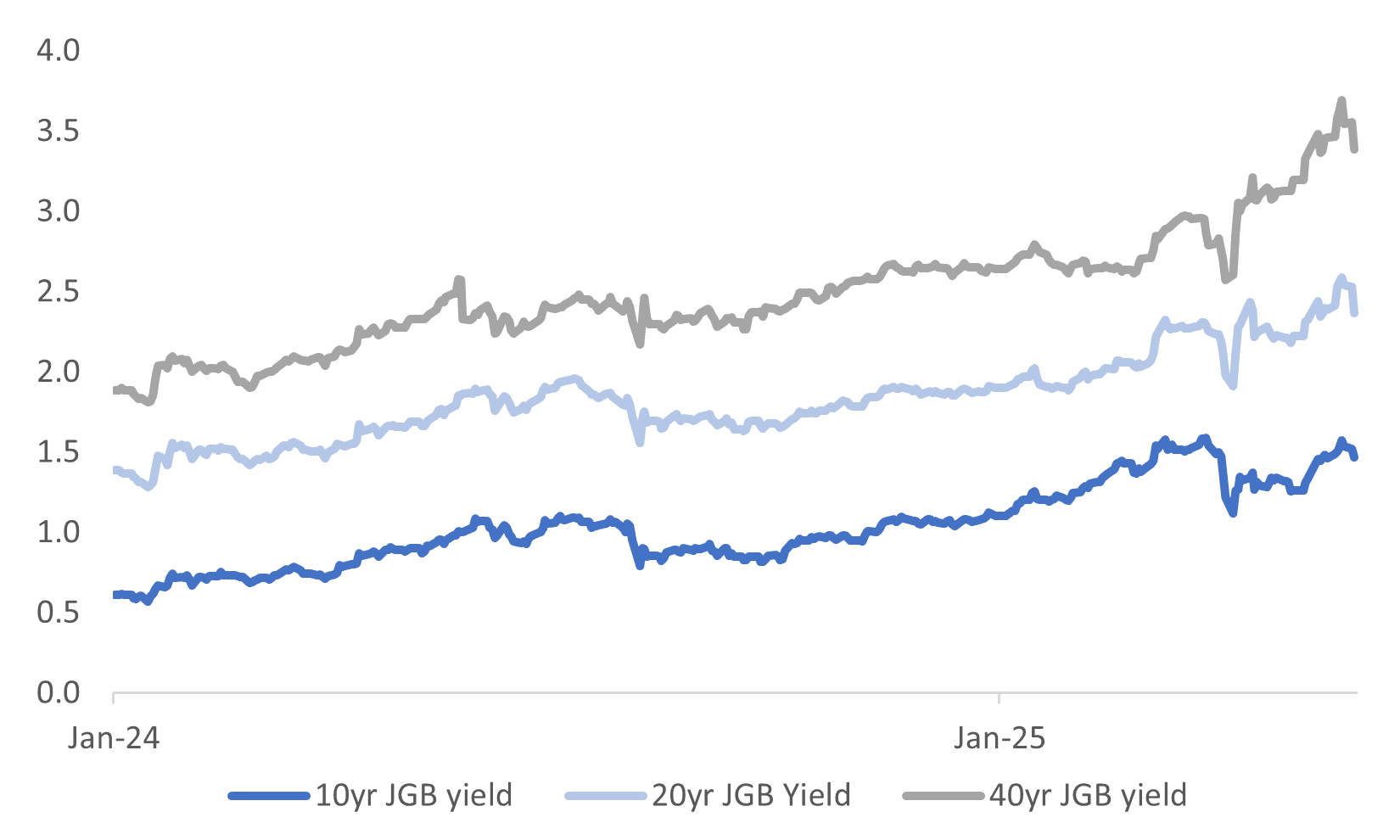

MNI EUROPEAN OPEN: Long End JGB Yields Off Recent Highs

EXECUTIVE SUMMARY

- EU TRADE CHIEF TOUTS ‘GOOD CALLS’ WITH LUTNICK, GREER - BBG

- LAGARDE SEES OPPORTUNITIES TO RAISE EURO’S GLOBAL PROFILE - BBG

- BOJ’S UEDA SEES INFLATION NEAR 2%, EASING STILL NEEDED - MNI

- JAPAN TO CLOSELY MONITOR BOND MARKET, FINANCE MINISTER SAYS - RTRS

- CHINA INDUSTRIAL PROFITS INCREASE IN APRIL - MNI BRIEF

Fig 1: JGB Yields Back Off Recent Highs

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

PRICES (BBG): “ UK's British Retail Consortium-Nielsen Shop Price Index fell 0.1% y/y in May versus -0.1% in April, according to the British Retail Consortium.”

EU

TRADE (RTRS): “The European Union may have won a reprieve from U.S. President Donald Trump's threatened 50% tariffs, but it remains unclear how the bloc will square its push for a mutually beneficial trade deal with Washington's demands for steep concessions.”

TRADE (POLITICO): “Top US, EU trade chiefs ‘in constant contact’ after Trump tariff reprieve.”

EUR (BBG): “ President Donald Trump’s erratic policies offer a “prime opportunity” to strengthen the euro’s international role and allow the currency bloc to enjoy more of the privileges so far reserved for the US, European Central Bank President Christine Lagarde said.”

UKRAINE/RUSSIA (BBG): “German Chancellor Friedrich Merz said Ukraine has been given permission to use weapons supplied by its allies to launch strikes deep inside Russia. “

NATO (BBG): “NATO Secretary General Mark Rutte confirmed the alliance will seek to adopt a new defense spending target of 5% of GDP at a June summit, meeting a demand by US President Donald Trump that had originally seemed unrealistic.”

UKRAINE (RTRS): “Russia has attacked Ukraine for a third night in a row, Ukrainian regional officials and emergency services said, a day after the biggest aerial attack of the war so far killed at least 12 people and drew condemnation from U.S. President Donald Trump.”

EU (POLITICO): “The ministers, led by Italy and Greece, used their monthly summit in Brussels on Monday to push back hard against any attempt to fold the bloc’s €386.6 billion Common Agricultural Policy into a broader, more flexible EU funding model.”

US

EU/US (BBG): “EU Trade Commissioner Maros Sefcovic said he had “good calls” with US Commerce Secretary Howard Lutnick and Trade Representative Jamieson Greer.”

OTHER

OIL (BBG): “OPEC+ brought forward a video-conference that will decide July oil production levels for eight key members by one day to May 31, delegates said.”

JAPAN (MNI): “Inflation expectations remain below the Bank of Japan's 2% target, despite reaching their highest levels in 30 years, which suggests that the BOJ must maintain accommodative policy for now, said Governor Kazuo Ueda said Tuesday.”

JAPAN (MNI BRIEF): “Japan’s services producer price index (SPPI) rose 3.1% y/y in April, easing from March’s revised 3.3%, suggesting that while corporate pass-through of cost increases remains solid, momentum is slowing, preliminary Bank of Japan data showed Tuesday.”

JAPAN (RTRS): "Japanese Finance Minister Katsunobu Kato said on Tuesday that the government will closely monitor the bond market ahead of the auction of super-long debt this week, warning that higher interest rates could put pressure on state finances."

CANADA (MNI): The Bank of Canada will lower interest rates later this year as the tariff war drags down growth more than it sparks inflation according to an OECD report Monday.

NEW ZEALAND (BBG): “Soft labor market conditions will mean weaker economic activity, the Treasury Dept says in Fortnightly Economic Update released on website Tuesday in Wellington.”

CHINA

PROFITS (MNI BRIEF): China saw profits of large-scale industrial enterprises increase by 1.4% y/y from January to April, an acceleration of 0.6 percentage points compared to Q1, the National Bureau of Statistics announced on Tuesday.

YUAN (YICAI): "The People’s Bank of China has taken a moderating approach to the yuan’s appreciation momentum rather than actively pushing for substantial gains, Yicai.com reported, citing market insiders' analysis."

LAND (CSJ): “China is likely to accelerate the issuance of local government special bonds used for purchase of idle land as part of efforts to stabilize its real estate market, according to a report by China Securities Journal.”

EVs (RTRS): “China's commerce ministry will meet industry bodies and automakers including BYD and Dongfeng Motor to discuss an emerging trend of sales of "used cars" that were never driven, a person with direct knowledge of the matter said.”

CHINA MARKETS

MNI: PBOC Net Injects CNY91 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY448 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY91 billion after offsetting the maturities of CNY357 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.5716% at 09:43 am local time from the close of 1.6545% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 46 on Monday, the same as the close on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1876 Tues; +0.83% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1876 on Tuesday, compared with 7.1833 set on Monday. The fixing was estimated at 7.1869 by Bloomberg survey today.

MARKET DATA

UK MAY BRC SHOP PRICE INDEX -0.1% Y/Y; EST. -0.1%; APR. -0.1%

SOUTH KOREA MAY CONSUMER CONFIDENCE 101.8; APR. 93.8

JAPAN APRIL SERVICES PRODUCER PRICES +3.1% Y/Y; EST. +3.0%; MAR. +3.3%

CHINA JAN.-APRIL INDUSTRIAL COMPANIES' PROFIT +1.4% Y/Y; MAR. +0.8%

CHINA APRIL INDUSTRIAL COMPANIES' PROFIT +3% Y/Y; MAR. +2.6%

MARKETS

US TSYS: Asia Wrap - Long-End Leads Yields Lower

The TYM5 range has been 110-01 to 110-07+ during the Asia-Pacific session. It last changed hands at 110-07, up 0-04 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.976%, down 0.01 from its close.

- The US 10-year yield has moved lower, dealing around 4.483%, down 0.03 from its close.

- The move was led by the long-end, the yield curve has flattened as a result - 2s10s -1.50 at 50.054.

- FT - "Quasi-governmental entities like Japan Post, Norinchukin, and GPIF together own over a trillion dollars of foreign bonds. The government could urge them to support the Japanese bond market. But that would likely involve selling their foreign bond holdings — most likely Treasuries — to buy JGBs. With Japan-US tariff negotiations under way, does Japan really want to be seen as the reason Treasury yields keep rising?" https://x.com/elerianm/status/1926273166520746139

- Bloomberg - “Donald Trump’s erratic policies offer a “prime opportunity” to strengthen the euro’s international role as a reserve currency, letting the EU enjoy lower borrowing costs and protections from sanctions, Christine Lagarde said.”

- The 10-year look likely to see supply on any dips in yield in the short-term, should yields hold above 4.40% the target looks to be the 4.75% area. Watch for any announcements though relating to the SLR, this could have an impact on a market that is already quite short.

- Data/Events : Durable Goods, FHFA House Price Index, Conference Board, Dallas Fed Man Activity.

JGBS: Massive Bull-Flattener, MoF May Tweak Long-End Issuance

JGB futures are stronger and approaching session highs, +30 compared to settlement levels, after reversing almost all of early weakness.

- A headline late in our session: "Japan's Ministry of Finance will consider tweaking the composition of its bond issuance plan for the current fiscal year ending in March 2026, which could involve trimming the issuance of super-long bonds, two sources with direct knowledge of the plan told Reuters".

- MNI: BOJ's Ueda Sees Inflation Near 2%, Easing Still Needed (See here)

- Robin Brooks on X: Japan is at the heart of the global rise in long-term yields. To be honest, I'm surprised the rise has been allowed to be as rapid as it has. At 240% debt to GDP, Japan really can't allow long-term yields to keep rising the way they have. This is where fiscal dominance is acute. (See here)

- Cash US tsys are 2-5bps richer, with a flattening bias, in today's Asia-Pac session after yesterday's holiday.

- Cash JGBs are 1-16bps richer across benchmarks, with the curve flatter. The benchmark 40-year yield is 16.3bps lower at 3.393% ahead of tomorrow's supply. ICYMI, last week's 20-year auction saw poor demand metrics.

- Swaps have twist-flattened, with rates 1bp higher to 12bps lower. Swap spreads are wider.

AUSSIE BONDS: Stronger Ahead Of Tomorrow's CPI Data

ACGBs (YM +4.0 & XM +6.0) are stronger with US tsys 2-4bps richer in today's Asia-Pac session after yesterday's holiday.

- Cash ACGBs are 4-6bps richer with the AU-US 10-year yield differential at -16bps.

- The bills strip richer, with pricing +1 to +4.

- RBA-dated OIS pricing is showing a 25bp rate cut in July as a 72% probability, with a cumulative 75bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar has been light.

- The focus remains on tomorrow's April CPI, which is forecast to moderate to 2.3% y/y from 2.4%. The trimmed mean has been around 2.7% y/y for four consecutive months. There will be limited updates to the services components being the first month of the quarter.

- Some of the components of Q1 GDP are also released this week, namely construction (Wed) and private capex (Thu).

- April retail sales print on Friday and are projected to rise 0.3% m/m after increasing the same amount in March.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Friday.

BONDS: NZGBS: Closed On A Strong Note Ahead Of Tomorrow’s RBNZ Policy Decision

NZGBs closed richer and at session bests, with benchmark yields 3-4bps lower.

- Swap rates closed 2-4bps lower, with the 2s10s curve flatter.

- The RBNZ decision is announced tomorrow with the OCR widely expected to be cut 25bp to 3.25%, bringing total easing this cycle to 225bp.

- 23 out of 24 analysts surveyed by Bloomberg are forecasting this outcome.

- Given heightened uncertainty, the MPC is likely to retain its easing bias again, stating it has “scope” to cut rates further if required and its updated OCR path will be scrutinised to this end. A downward revision bringing the terminal to below 3%, estimated 'neutral', would signal a need for accommodation.

- The attention will be on the medium-term which is likely to show a softer outlook driven by weaker trading-partner growth due to recent global uncertainty. The RBNZ said in April that “on balance, these developments create downward risks to the outlook for economic activity and inflation in New Zealand”. See MNI RBNZ Preview here)

- Markets continue to price in 25bps of easing for tomorrow's meeting, with 64bps expected by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-36 bond.

FOREX: Asia FX Wrap - Quiet Asian Session

The BBDXY has had a range of 1208.48 - 1210.80 in the Asia-Pac session, it is currently trading around 1210. “The ECB’s Gediminas Simkus says there’s a growing danger that inflation will fall short of the central bank’s 2% target due to trade friction and a stronger euro, adding there’s scope for a rate cut next month”(BBG). “Donald Trump’s erratic policies offer a “prime opportunity” to strengthen the euro’s international role as a reserve currency, letting the EU enjoy lower borrowing costs and protections from sanctions, Christine Lagarde said.”(BBG)

- EUR/USD - Asian range 1.1383 - 1.1407, Asia is currently trading 1.1390. EUR has had a quiet day in the Asian session. What stood out from the price action on Friday was how well the EUR held up in the face of a potential 50% increase in tariffs, and it was again the USD that took the brunt of the impact. This clearly shows the market's current outlook and leans into the growing “sell America “ theme. Dips back to 1.1200/1300 should be supported.

- GBP/USD - Asian range 1.3557 - 1.3587, Asia is currently dealing around 1.3565. The GBP is breaking the Pivotal Weekly Resistance in the 1.3500 area, all eyes will be on how the market reacts up here as most participants return. A sustained break though would signal a potential acceleration of the trend higher.

- USD/CNH - Asian range 7.1712 - 7.1851, the USD/CNY fix printed 7.1876. Asia is currently dealing around 7.1840. Sellers should be found on a bounce back towards the 7.2200 area again. Andreas Steno Larsen on X : The elephant in the room. USDCNH needs to go to 6.80 at least. https://x.com/AndreasSteno/status/1926115935200440525

- Cross asset : SPX +0.89%, Gold $3340, US 10-Year 4.48%, BBDXY 1210, Crude oil $61.31

- Data/Events : Ger Gfk Consumer Confidence, France CPI, EZ Consumer Confidence

JPY: Asia Wrap - USD/JPY Back Under Pressure

The Asia-Pac USD/JPY range has been 142.12 - 142.96, Asia is currently trading around 142.55. USD/JPY was under pressure early in our session as BOJ Governor Ueda sounded confident the central bank would meet its inflation target. A headline late in our session: "Japan's Ministry of Finance will consider tweaking the composition of its bond issuance plan for the current fiscal year ending in March 2026, which could involve trimming the issuance of super-long bonds, two sources with direct knowledge of the plan told Reuters". The long end in the JGB's extended their move lower late in our session and USD/JPY is attempting to bounce off its lows.

- MNI: BOJ's Ueda Sees Inflation Near 2%, Easing Still Needed https://www.mnimarkets.com/articles/mni-bojs-ueda-sees-inflation-near-2percent-easing-still-needed-1748306760883

- “The upcoming 40-year JGB auction tomorrow will be closely watched following a lackluster 20-year sale last week — a sign of the caution that still runs deep among long-end investors.”(BBG)

- Robin Brooks on X : Japan is at the heart of the global rise in long-term yields. To be honest, I'm surprised the rise has been allowed to be as rapid as it has. At 240% debt to GDP, Japan really can't allow long-term yields to keep rising the way they have. This is where fiscal dominance is acute. https://x.com/robin_j_brooks/status/1926991620370522435

- USD/JPY again struggled to hold onto any gains above 143.00, can Ueda’s comments get it to break below 142.00 or does this level hold again.

- The price action last week shows the market is still much more comfortable selling rallies, resistance is now back towards 144.00/145.00. The focus will turn once more to the pivotal 140.00 area, a break of which will open a much deeper move lower.

Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 143.00($1.81b May 28), 143.00($3.06b May 30), 140.00($2.68b May 30).

Fig 1 : JGB 30 Year Daily Chart

NZD: Asia Wrap - Struggling To Hold Above 0.6000

The NZD/USD had a range of 0.5986 - 0.6007 in the Asia-Pac session, going into the London open trading around 0.5995. The NZD has drifted a little lower in a quiet Asian session, with US Stocks giving back their small overnight gains.

- (Bloomberg) - “Data since the April meeting have shown a softer labor market. Inflation has perked up but not enough to stop the RBNZ from proceeding with a 25-bp rate cut.”

- “There is significant downside risk to the growth outlook stemming from the global trade war. Even so, the 1Q CPI outcome is likely to see the RBNZ maintain its current OCR projections for only modest rate cuts.”

- Markets continue to price in 25bps of easing for tomorrow's meeting, with 64bps expected by November 2025.

- The NZD continues to trade in a 0.5850/0.6050 range, can it find the momentum to break this week, as the “sell America” trade gathers pace.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here could provide the spark for the next leg higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5725(NZD1.09b May 28)

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community added a decent clip back to their own short.

AUD/NZD range for the session has been 1.0803 - 1.0824, currently trading 1.0820. A sustained break above 1.0930 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: AUD/NZD Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - Drifts Lower in The Crosses

The AUD/USD has had a tight range of 0.6475 - 0.6495 in the Asia- Pac session, it is currently trading around 0.6485. A very quiet session in Asia with AUD weakness coming through in the crosses, and the USD continuing to be sold against an Asian basket.

- The AOFM sells A$400mn of the 4.25% 21 June 2034 Green Bond: Average Yield (%): 4.2162 (prev. 4.1725), Bid/Cover: 5.1625x (prev. 4.8875x).

- The AUD range has been pretty muted during the Asian session. The AUD continues to hold up pretty well against the USD so If you want to express a short it looks best to do that in the crosses for now.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6510(AUD1.55b), 0.6550(AUD 610m), 0.6500(AUD 443m). Upcoming Close Strikes : none

- CFTC Data shows Asset managers have continued to add to their shorts, the Leveraged community also added to shorts though still a very small position.

AUD/JPY - Today's range 92.14 - 92.76, it is trading currently around 92.30. The pair could not hold back above 93.00 overnight. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA: Major Bourses Down in Weak Day Across Region

Following yesterday's decline of -8.60%, China's BYD fell again today dragging the Hang Seng lower and impacting sentiment in the region. BYD is down -3.6% today as concerns grow that its sales success hides the scale of discounting in China. BYD announced price cuts of over 30% to stabilise the performance. BYD stock had risen over 70% this year, putting the recent falls in context.

In Korea holding companies are rallying with some up over 10% as expectations that a new president may be more shareholder friendly. One of Malaysia's biggest banks Maybank quarterly earnings showed solid loan growth and a 4% rise in income for the first quarter. With net foreign inflows of over $250m in May, Indonesia's Jakarta Composite is set to continue its recent run of good performance.

- China's major bourses were all lower today with the Hang Seng down -0.18%, CSI 300 -0.55%, Shanghai -0.33% and Shenzhen down -0.65%

- The KOSPI fell -0.66% today as markets hold their breath ahead of the BOK this week.

- The FTSE Malay KLCI fell again today, down -0.52% eighth day of losses out of the the last eleven trading days.

- The Jakarta Composite did very little today but remains over 6% better for the week.

- The Straits Times in Singapore eked out modest gains of +0.13% and the PSEi in the Philippines was flat.

- The NIFTY 50 is down -0.88% yet is holding on to a +1.8% gain for the month to date.

OIL: Crude Expects Another Large OPEC Output Increase, Meeting May 31

- Oil prices are down slightly today after finishing little changed yesterday. WTI is 0.5% lower at $61.24/bbl after reaching a high of $61.74 earlier. Brent is down 0.3% to $64.56 off the peak of $64.98. The market continues to monitor US trade talks especially with the EU but the focus now is on the May 31 OPEC meeting where another large output increase is expected to be agreed. The USD index is up 0.1%, which is probably moderately weighing.

- While energy markets remain concerned that the imposition of outsized tariffs would weigh on global energy demand, it is currently focussed on the impact of OPEC’s production plans on an already expected market surplus. The group increased output by over 400kbd in both April and June, more than expected. Apparently, a rise of a similar size is being discussed for July.

- There is key US data this week to gauge the strength of demand including orders (Tues), Q1 GDP revision (Thus), PCE (Fri), Trade (Fri) and Uni Michigan consumer confidence (Fri). There are also US crude & product data.

- Later the Fed’s Kashkari and Barkin appear. US April durable orders, May consumer confidence & Dallas Fed manufacturing index, March US house prices, French preliminary May CPI and euro area EC May survey are released.

GOLD: Bullion Under Pressure As Trade Talks Continue

Gold prices are slightly lower today down 0.3% to $3334.00 off the intraday low of $3331.99. Flight-to-quality flows continue to recede as trade negotiations continue with the current focus on US-EU.

- With the US appearing more open to reaching trade deals ahead of its July deadline, Bloomberg estimates that gold-backed ETFs have seen five consecutive weeks of outflows. However, the market remains nervous about the US’ fiscal position and any perception of a further deterioration would be supportive for bullion.

- Equities are mixed with the Hang Seng down 0.2% but S&P e-mini up 0.9% and ASX +0.3%. US 10yr yields are lower. Oil prices are down with WTI -0.3% to $61.34/bbl. Copper is 0.9% lower and iron ore has tested $95.80/t. Silver is down 0.7% to $33.25, close to the intraday low.

- Later the Fed’s Kashkari and Barkin appear. US April durable orders, May consumer confidence & Dallas Fed manufacturing index, March US house prices, French preliminary May CPI and euro area EC May survey are released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 27/05/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 27/05/2025 | 0645/0845 | *** | HICP (p) | |

| 27/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kashkari | ||

| 27/05/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 27/05/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 27/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 27/05/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 28/05/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 28/05/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 28/05/2025 | 0130/1130 | *** | Quarterly construction work done | |

| 28/05/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 28/05/2025 | 0600/0800 | ** | Retail Sales | |

| 28/05/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 28/05/2025 | 0645/0845 | ** | PPI | |

| 28/05/2025 | 0645/0845 | *** | GDP (f) | |

| 28/05/2025 | 0645/0845 | ** | Consumer Spending | |

| 28/05/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/05/2025 | 0755/0955 | ** | Unemployment | |

| 28/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kahkari | ||

| 28/05/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index |