MNI EUROPEAN OPEN: JGB Yield Curve Breaking Down

EXECUTIVE SUMMARY

- MARIO DRAGHI'S CALL FOR "PRAGMATIC FEDERALISM" AMONG VARYING SUBSETS OF EUROPEAN UNION STATES - MNI

- CBO PROJECTS RISING US DEFICITS ON INTEREST COSTS - MNI

- FED’S SCHMID - POLICY SHOULD KEEP PRESSURE ON INFLATION - MNI

- JAPAN JAN CGPI RISES 2.3% Y/Y; IMPORT PRICE RISES - MNI

- RBA'S BULLOCK SEES NAIRU AT 4.6% - MNI BRIEF

Fig 1: JGB Yield Curve Breaking Flatter

Source: MNI - Market News/Bloomberg

UK

FX (BBG): “Britain has moved closer to becoming the first G7 country to issue a sovereign bond on the blockchain, after the Treasury appointed a bank and law firm to handle a digital gilt pilot this year.”

HOUSE PRICES (BBG): "For the first time in more than a year, property agents expect house prices to rise in London, a survey revealed Thursday."

EU

POLITICS (MNI): Draghi's 'Pragmatic Federalism' Gains Support- Official: Mario Draghi's call for "pragmatic federalism" among varying subsets of European Union states in order to accelerate the completion of the Single Market is finding support among some EU leaders ahead of Thursday's "brainstorming" session in Belgium, a senior EU official said.

FRANCE (BBG): "French President Emmanuel Macron returned to his “Made in Europe” push on the eve of a key European Union meeting, putting him at odds with German Chancellor Friedrich Merz over how best to tackle Europe’s economic woes."

US

FISCAL (MNI BRIEF): CBO Projects Rising US Deficits On Interest Costs: The nonpartisan Congressional Budget Office warned again Wednesday that the U.S. is on an unsustainable fiscal path, increasing its estimate of the 10-year deficit by USD1.4 trillion as rising rising interest costs boost the shortfall.

FED (MNI): Fed’s Schmid - Policy Should Keep Pressure On Inflation: Federal Reserve Bank of Kansas City President Jeff Schmid said Wednesday interest rates should stay at a level where they continue to put some pressure on the economy so that inflation can cool further, while also advocating further efforts to shrink the central bank's balance sheet.

TARIFFS (BBG): "Donald Trump’s tariff policies suffered their strongest political blow yet with the Republican-led US House passing legislation aimed at ending the president’s levies on Canadian imports."

IRAN (BBG): "US President Donald Trump said he told Israeli Prime Minister Benjamin Netanyahu he intended to press ahead on talks with Iran, and that his preference was to reach a deal with the Islamic Republic despite reservations from the visiting leader."

JAPAN

PRICES (MNI BRIEF): Japan Jan CGPI Rises 2.3% Y/Y; Import Price Rises: Japan's corporate goods price index rose 2.3% y/y in January, easing from 2.4% in December, while import prices increased for a second straight month, Bank of Japan data showed Thursday. The index rose 0.2% m/m, marking a fifth consecutive increase after a revised 0.1% rise in December.

BOJ (MNI POLICY): MNI discusses the BOJ's appetite for a March hike. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

OTHER

CANADA (MNI): BOC Discussed `Optionality,' Broader Tariff Spillover Risk: Bank of Canada officials discussed the need to keep their options open amid higher geopolitical risks and the potential for heavy U.S. tariffs on a few industries to create wider economic damage, minutes from a decision two weeks ago to keep a 2.25% policy rate showed.

CANADA (MNI): Canada's Immigrant Clampdown Deepens BOC Conflicts: Canada faces weakened output and labor market tightening because of foreign work permit reductions, adding to risks for its central bank which is already low weak growth and danger from U.S. tariffs.

AUSTRALIA (MNI BRIEF): RBA's Bullock Sees NAIRU At 4.6%: Reserve Bank of Australia has lifted its NAIRU estimate by around 10 basis points to 4.6%, Governor Michele Bullock told a Senate estimates hearing Thursday. Her comments follow the Board’s decision last week to raise the cash rate 25bp to 3.85% and updated forecasts showing higher inflation and weaker potential growth.

SILVER (BBG): “Silver jumped, extending a run of elevated volatility, as an industry body pointed to stronger investment buying and weaker industrial demand in the year ahead. The silver market will be in deficit for a sixth consecutive year, according to a report published by the Silver Institute, as surging investment outweighs wilting demand for jewelry and efforts to curb use in the solar sector.”

CHINA

POLITICS (SCMP): "Trump and Xi expected to extend trade truce at Beijing summit. Leaders may roll back tariffs for up to a year as China resumes soybean buys and officials seek short-term economic wins before US midterms."

GOLD (MNI): China Gold Demand Robust, Despite Volatility: Demand for Chinese gold ETFs is expected to continue robust growth in 2026 despite official concern over the exposure of retail investors to volatility and speculation, local analysts told MNI. Geopolitical risk, persistent domestic growth challenges and continued weakness in the property sector are likely to keep Chinese investors drawn to the metal’s safe-haven appeal following a record-breaking 2025, said Ray Jia, Research Head APAC (ex-India) and Deputy Head of Trade Engagement, China, at the World Gold Council.

MNI: PBOC Net Injects CNY448 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY166.5 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The PBOC conducted another CNY400 billion via 14-day reverse repos today. The operation led to a net injection of CNY448 billion after offsetting the maturity of CNY118.5 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.5004% at 09:31 am local time from the close of 1.5388% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Wednesday, the same as the close on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 6.9457 Thurs; +5.31% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 6.9457 on Thursday, compared with 6.9438 set on Wednesday. The fixing was estimated at 6.9129 by Bloomberg survey today.

MARKET DATA

AUSTRALIA FEB CONSUMER INFL EXPN 5.0%; 4.6% PRIOR

JAPAN JAN PPI YOY 2.3%; 2.3% ESTIMATE; 2.4% PRIOR

JAPAN JAN TOKYO OFFICE VACANCIES 2.15%; 2.2% PRIOR

MARKETS

US TSYS: Yields Range Bound, US CPI Friday Next Focus

A quiet day post NPF with US futures barely moving and yields range bound. TYH6 has traded in a 112-07 to 112-11 range today, but remains unchanged at 112-09.

Cash was marginally better in the front end with yields modest lower, though volumes were extremely light.

- The 2-yr is down -0.6bps to 3.508%

- The 5-Yr is down -0.5bps to 3.739%

- The 10-Yr is down -0.2bps to 4.172%

- The 30-Yr is up +0.3bps to 4.811%

There is more jobs data out tonight with Initial Jobless Claims (est. 223k, prior 231k), continuing claims (est. 1850k, est 1844k prior) and existing home sales. Friday's CPI will be the next major release for bond markets with January CPI forecast to moderate to 2.5% from 2.7% in December. Yields are highly reactive to data at present given very little priced in in terms of rate moves and a miss either way could see decent swings in yields.

The auction schedule tonight sees US$95bn 8-week, US$105bn 4-week and US$25bn 30-Yr.

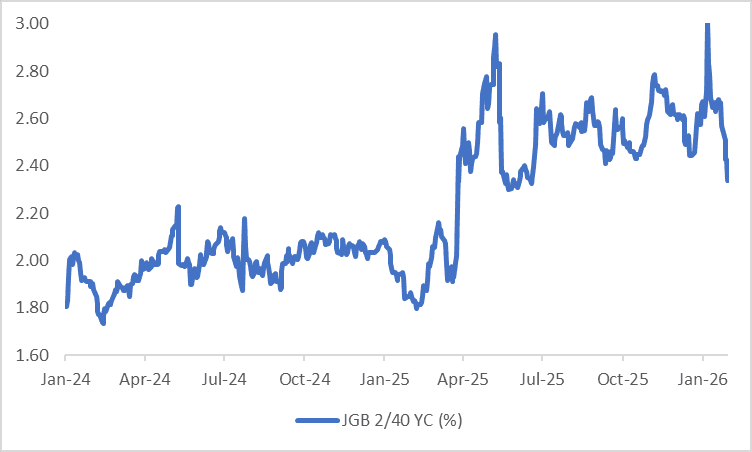

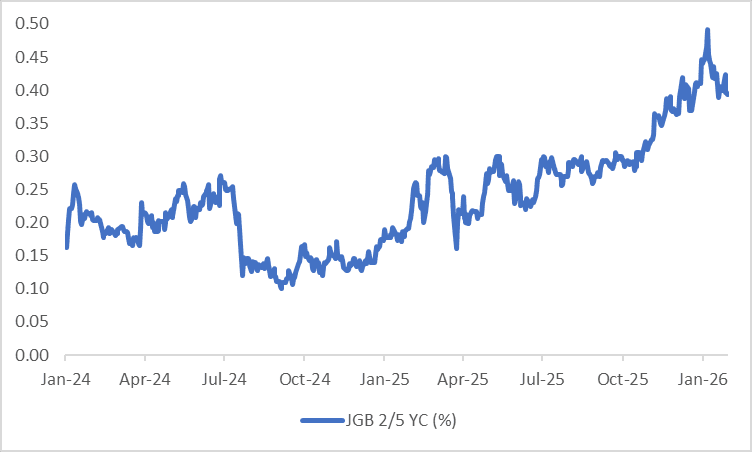

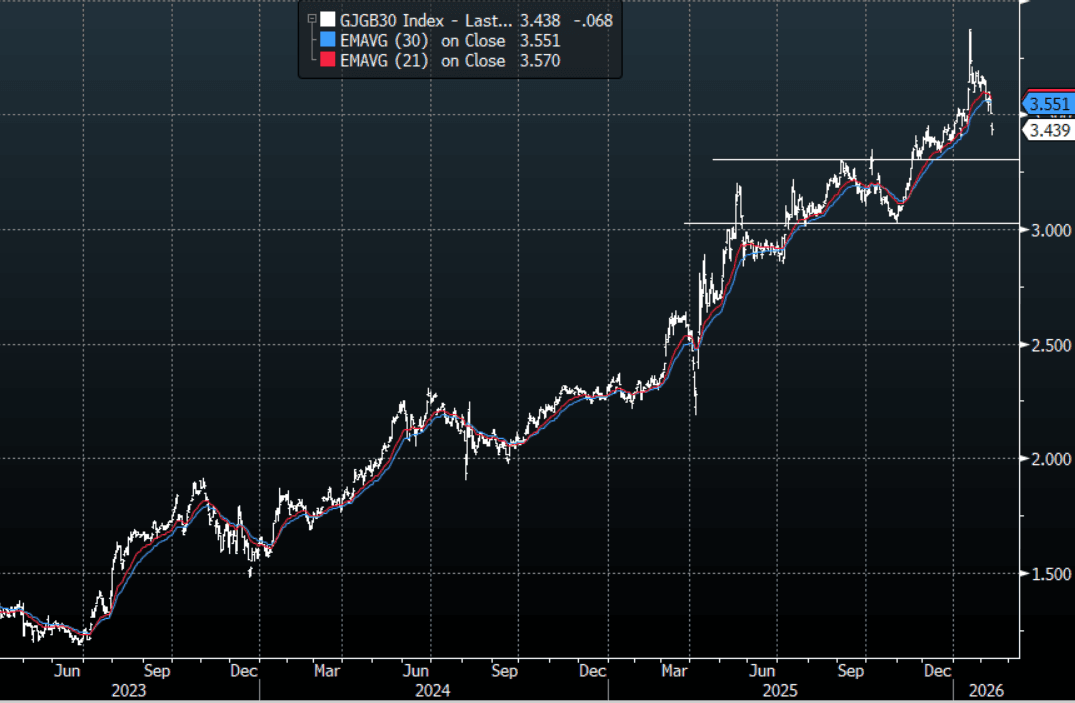

JGBS: Yield Curve Breaking Flatter As Fiscal Concerns Fade

JGB futures are stronger, +20 compared to settlement levels, but at session lows.

- The Japan Jan PPI was in line with market forecasts.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's post-payrolls sell-off.

- Cash JGBs have bull-flattened, with yields 1-9bps lower across benchmarks.

- After reaching a record steepness in mid-January, the 2/40 yield curve is now testing the lower bound of the well-defined range that has contained price action since mid-year.

- Since late last year, steepening has been most pronounced in the 2/5 segment, leaving the 5-year sector relatively unattractive on the curve. Into the recent election, expectations of fiscal expansion under a Takaichi administration implied heavier debt supply, reinforcing pressure on intermediates.

- In recent days, however, those fiscal concerns appear to have moderated following Prime Minister Sanae Takaichi's historic election victory.

- Notably, while the 2/5 segment has flattened, it is the 5/40 curve which has broken through the bottom of the range it has traded in since June last year.

- Swap rates are flat to 5bps lower, with a flatter curve.

- Tomorrow, the local calendar will see Weekly International Investment Flow data alongside an Auction for Enhanced-Liquidity 5-15.5 YR and BOJ Board Member Tamura Speech in Kanagawa.

Source: Bloomberg Finance LP

AUSSIE BONDS: Cheaper, RBA: Ready To Raise Rates Further, Infl Expns Up

ACGBs (YM -4.0 & XM -4.0) are weaker after dealing in relatively narrow ranges in today’s session.

- (Bloomberg) “Australia’s central bank stands ready to raise interest rates further if inflation proves persistent, Governor Michele Bullock said, stressing that the board remains cautious and is yet to decide whether further tightening is warranted. The Reserve Bank chief told a panel of senators on Thursday at Parliament House in Canberra that inflation running “with a three in front of it” is unacceptable."

- RBA Hunter is due to give a speech at a CEDA event in Perth (15:45 AEST).

- MI’s inflation expectations rose to 5% in February from 4.6% in January.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's post-payrolls sell-off.

- Cash ACGBs are 4bps cheaper with the AU-US 10-year yield differential at +63bps, just below its recent high.

- The bills strip has bear-steepened, with pricing -1 to -5.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 95% by June and 154% by December 2026.

- Tomorrow, the local calendar will be empty.

- The AOFM plans to sell A$1000mn of the 2.50% 21 May 2030 bond tomorrow.

Bloomberg Finance LP

BONDS: Modestly Cheaper Ahead Of Heavy Local Calendar Tomorrow

NZGBs closed showing a modest bear-steepener, with benchmark yields 2-3bps higher.

- NZ-US and NZ-AU 10-year yield differentials closed little changed.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday’s post-payrolls sell-off. US jobless claims highlight a lighter calendar on Thursday, before the focus turns to Friday’s release of US CPI.

- Nevertheless, today’s weekly supply auction exhibited solid demand characteristics, with cover ratios ranging from 3.77x (May-35) to 4.12x (May-31).

- Swap rates closed 3-4bps higher, with wider implied swap spreads.

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 44bps.

- The local calendar has been light this week ahead of tomorrow’s release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

Bloomberg Finance LP

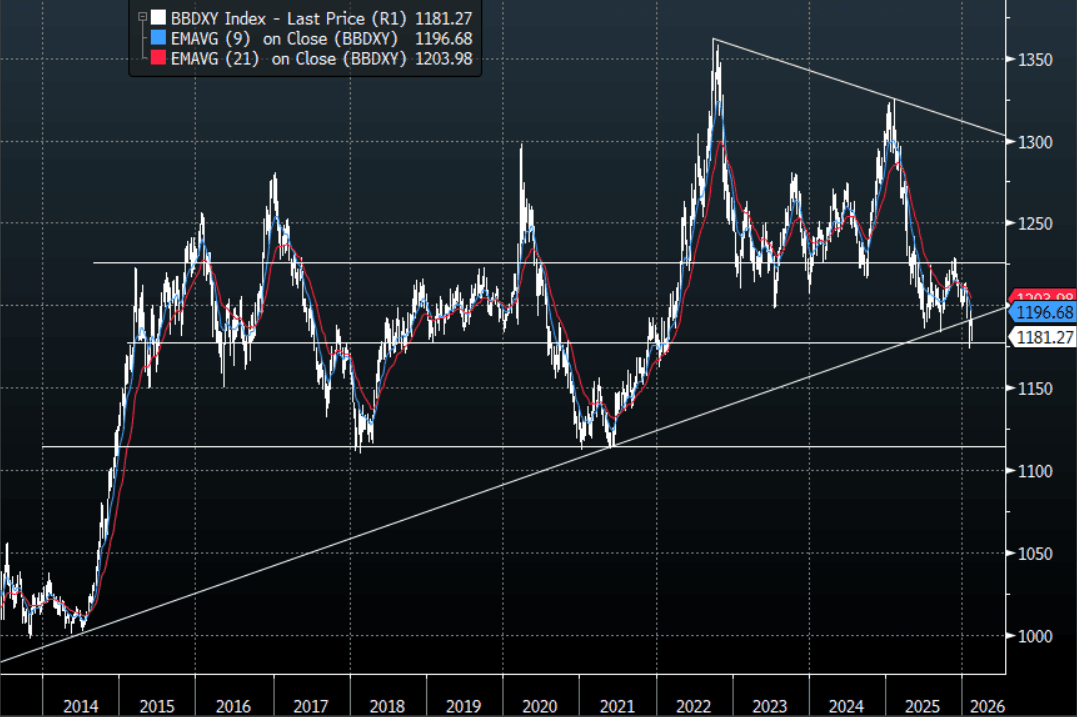

FOREX: USD - Trades Heavy Even After A Strong Payrolls

The BBDXY has had a range today of 1180.12 - 1182.72 in the Asia-Pac session; it is currently trading around 1181. The USD has drifted lower for most of our session as the market tries to interpret its inability to react to the better Payrolls data. The market is very bearish the USD and it does not take a lot for the sellers to come back to market as nobody wants to miss out on this trade. Even the significant bounce in US yields as cuts were priced out did little to aid it. On the day, the first resistance is toward the 1185-1187 area and then 1195 where I suspect we could see buyers return. A sustained break below 1175-1180 could potentially signal the start of another leg lower targeting 1150 first and then potentially 1115, see graph below.

- EUR/USD - Asian range 1.1864-1.1885, Asia is currently trading 1.1865. The pair found buyers back toward 1.1800 as the USD initially got bought, but unlike other currencies the EUR has not quite got back to its highs from yesterday. Price action remains constructive, can it now build some momentum from that base to push on? On the day, the first support is back toward 1.1820-1.1850 and then the 1.1750 area. A sustained move back above 1.1925-1.1940 could give it the thrust it needs to have another look toward the 1.2000 area.

- GBP/USD - Asian range 1.3616-1.3642, Asia is currently dealing around 1.3625. The pair is trading pretty poorly considering how weak the USD is. GBP continues to look like 1.3580-1.3730 to me for now as we wait to see if the big USD could potentially break lower, could CPI Friday give it the nudge it needs ?

- Cross asset : SPX +0.30%, Gold $5055, US 10-Year 4.175%, BBDXY 1181, Crude Oil $65.01

- Data/Events : Germany Current Account Balance

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY-Moves Through Overnight Lows As USD Struggles & JGB Yields Sink

The USD/JPY range today has been 152.27-153.45 in the Asia-Pac session, it is currently trading around 152.55, -0.45%. USD/JPY has remained under pressure all through our session as JGB long-end yields came crashing lower, putting in a nice bearish shadow on the daily chart. USD/JPY tried higher overnight as US yields spiked but very quickly reversed and made new lows. Is this just a case of short-term positioning still getting squeezed or does the FX market just not believe the data? Regardless of the reasons, leveraged Yen shorts are being pressured and no doubt are once again being pared back. This price action does look messy but I still believe dips back toward the 149-152 will probably provide solid support again should we see it, until then it looks like we chop around albeit with a heavy tone. On the day, the first resistance is back towards 153.50-154.00 and then 154.80-155.20 area as the market pares back its overextended USD longs and looks for another base to form from which to move higher again.

- "JAPAN TOP CURRENCY DIPLOMAT MIMURA: CLOSELY WATCHING MARKETS WITH A HIGH SENSE OF URGENCY. WON'T COMMENT ON FOREX LEVELS. WILL KEEP COMMUNICATING WITH US AUTHORITIES, WE'RE NOT LOWERING OUR GUARD AT ALL" - RTRS

- Bloomberg - “JGB Yields Falling More About BOJ Hike Bets Than Fiscal Stance. Long-end JGB yields are extending their decline, with the move looking far more about Bank of Japan’s policy expectations than the government’s fiscal restraint.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.00($735m), 154.00($2.4b). Upcoming Close Strikes : 156.00($1.87b Feb 17), 159.00($1.91b Feb 13),160.00($3.06b Feb 13) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 164 Points

Fig 1 : JGB 30-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

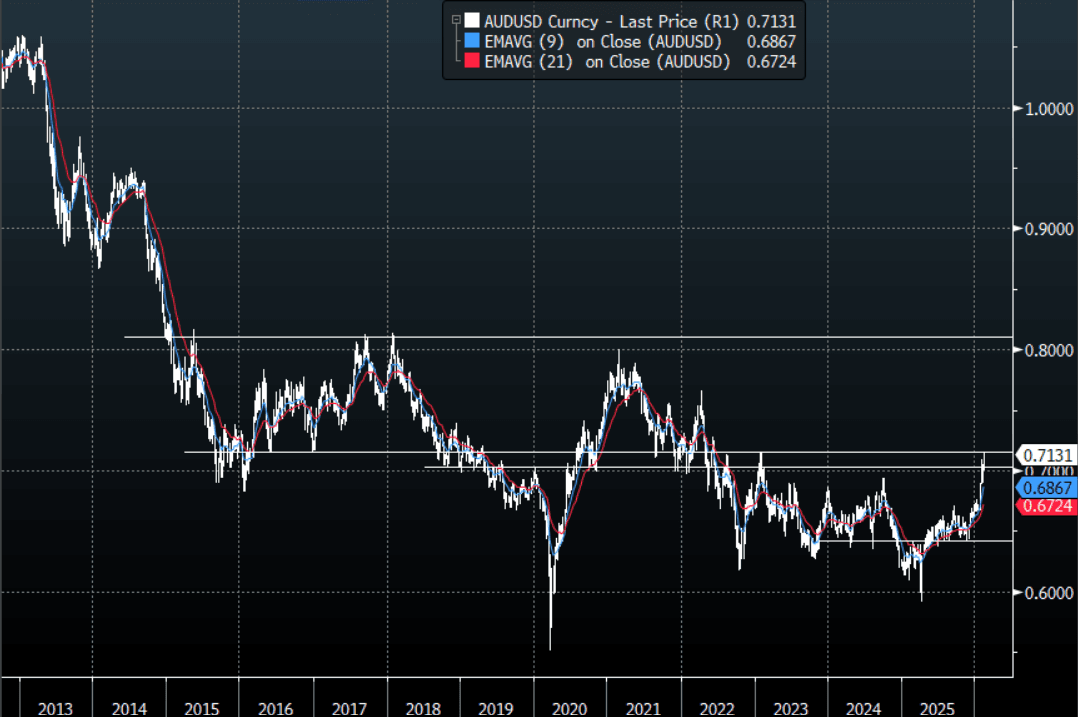

AUD/USD - Drifts Higher As The USD Continues To Struggle

The AUD/USD has had a range today of 0.7119 - 0.7147 in the Asia- Pac session, it is currently trading around 0.7130. The AUD has remained well supported in our session as the USD continues to struggle. The AUD after a brief drop overnight is back above its recent highs, the AUD remains a favourite vehicle to express a long at the moment. The AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is back toward the 0.7060–0.7090 area, and then the 0.7000 area. The bulls will be looking for dips to remain supported in order to regain the momentum to challenge the pivotal 0.7100-0.7200 area. A sustained break above here targets 0.7600-0.7800 first and then 0.8000-0.8200.

- MNI BRIEF: RBA's Bullock Sees NAIRU At 4.6%. Bullock said returning inflation to the 2.5% midpoint target may or may not require further hikes, adding that a stronger Australian dollar and higher interest rates will help dampen demand. Australia's unemployment rate tightened to 4.1% in December.

- Bloomberg - “Australia’s central bank stands ready to raise interest rates further if inflation proves persistent, Governor Michele Bullock said, stressing that the board remains cautious and is yet to decide whether further tightening is warranted.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7080(AUD342m). Upcoming Close Strikes : 0.6800(AUD1.55b Feb 13), 0.6825(AUD791m Feb 13) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 79 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

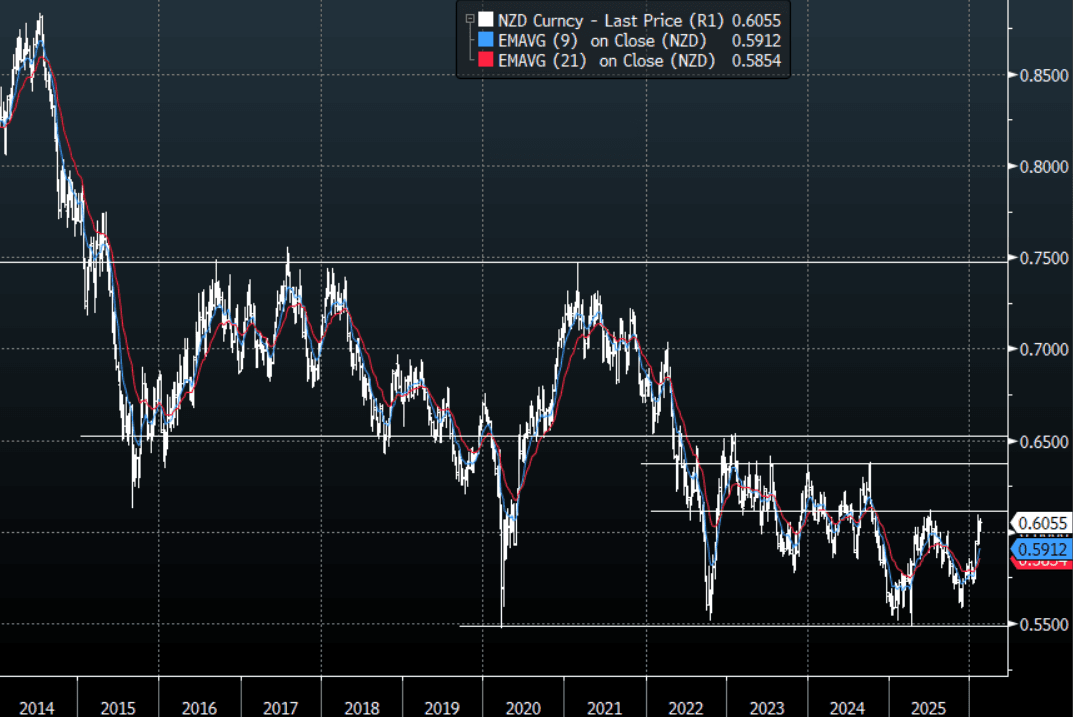

NZD/USD - Consolidating Around 0.6050, Eyes 0.6100 As USD Trades Heavy

The NZD/USD had a range today of 0.6044-0.6062 in the Asia-Pac session, it is currently trading around 0.6055, +0.12%. The NZD is consolidating its recent gains around the 0.6050 area. The NZD is back around where it started the day yesterday. I am a little surprised by the lack of reaction to the strong payrolls, but the bulls will be very happy with the constructive price action. On the day, the NZD bulls will be hoping the pair can regain its upward momentum to test the pivotal 0.6100 area. The first support is back toward 0.5990-0.6020 and then the 0.5900-0.5950 area. A sustained break back above 0.6100 could potentially open up a move back toward the 0.6400-0.6600 area and then beyond.

- MNI AU - USD/CNH Breaks Under 6.9000, Fresh Lows Since 2023, Onshore CNY Gains Aid Move.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5900(NZD301m Feb16), 0.6000(NZD308m Feb 16), 0.6200(NZD430m Feb 16) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 59 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

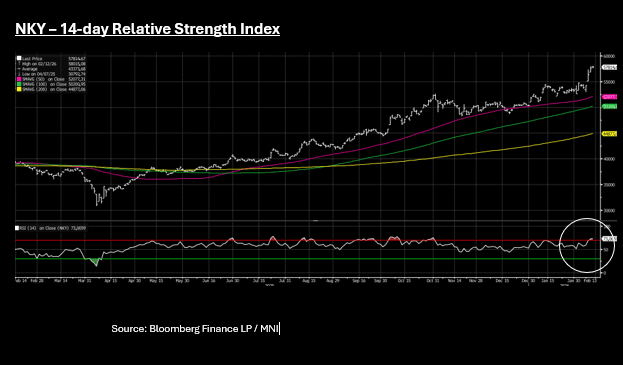

ASIA STOCKS: KOSPI & NKY Hit New Highs; NKY Reaches Overbought on 14RSI

The Nikkei returned from holiday today but couldn't replicate the gains from earlier in the week. Up just +0.25% today it takes the index to over 6% higher for the week on a day when the long end of the JGB curve rallied strongly, retracing losses from January February. Currently at 57,800 the NKY has reached yet another new high, having delivered year to date gains over 10%. The gains have seen the NKY reach Overbought on the 14RSI - which could dampen near term further gains.

News that a potential rescue package could be announced by the Shenzhen government to the tune of CNY80bn did little to impact China's major equity markets Thursday with the HSI down -0.85 and onshore bourses posting only modest gains. Other key real estate names in HK did however receive a boost with Sun Hung Kai Properties one of the main gainers for the index.

Ongoing strength of inflows is a fundamental support for the TAIEX in Taiwan with gains of +1.6% today ahead of LNY, as TSMC rose over 2% to a new record of TWD1,915. The KOSPI had a strong day also with key AI names SK Hynix up +2.5% and Samsung up +6.00% contributing to the KOSPI's gain of +2.6%. Earlier the KOSPI hit a new high of 5,515 only to moderate back to 5,498

The JCI sits on gains of over 4% for the week despite modest falls Thursday, as President Prabowo's heads to the US where it is intended he signs the US trade deal.

Oil Tight Ranges in Near Term, Pending Further News from US Iran Talks

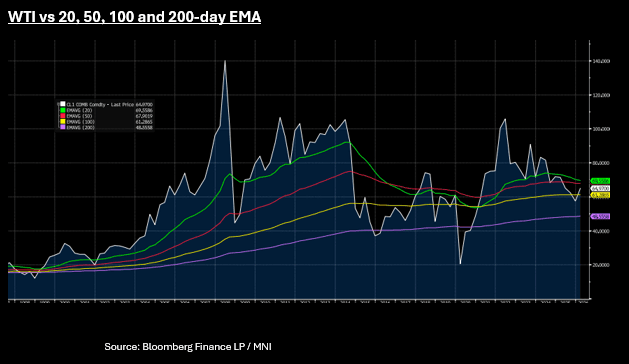

- Oil's steady ascent continued in Asia today with WTI up +0.5%, nearing $65. WTI has traded in a $64.78 - $65.10 range, currently at US$64.97bbl. WTI is at the mid point of its upper resistance via the 50-day EMA of $67.90 and downside via the 100-day EMA at 61.28. Momentum indicators are weak, leaving oil susceptible to US Iran headlines. This suggests prices are likely to stay rangebound in the near term as political progress remains slow.

- Brent is up +0.4% at US$69.70bbl - having traded in a very tight range of $69.54 - 69.85.

- Oil markets continue to wait for further new on the next US Iran meeting whilst digesting the myriad of news out on stockpiles and potential new oil sources.

- Chevron, Eni , QatarEnergy, Repsol won rights to explore for oil in Libya, the latest sign that the nation that holds Africa's largest crude reserves is opening up for investments following years of civil war. (per BBG)

The well known longer term oversupply issue is not a key driver in the short term as uncertainty remains as to any outcome of US Iran talks. The bar is high for a clear outcome with both sides stoic in their views as to their preferred outcome.

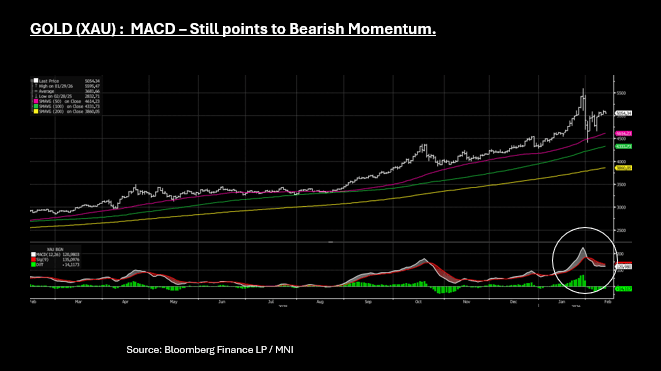

GOLD: Bearish Momentum Remains in Prices, $5,000 Could be Re-Tested

- Demand for Chinese gold ETFs is expected to continue robust growth in 2026 despite official concern over the exposure of retail investors to volatility and speculation, local analysts told MNI.

https://www.mnimarkets.com/articles/mni-china-gold-demand-robust-despite-volatility-1770859956330 - Geopolitical risk, persistent domestic growth challenges and continued weakness in the property sector are likely to keep Chinese investors drawn to the metal’s safe-haven appeal following a record-breaking 2025, said Ray Jia, Research Head APAC (ex-India) and Deputy Head of Trade Engagement, China, at the World Gold Council.

- This follows news out earlier this week showing that even during the time of volatility for gold, the PBOC still added to its holdings.

- This underpins the narrative that many investors now hold that gold's rise is a function of the long term decline in the US, suggesting it could hit US$6,000 sooner rather than later.

- Gold has traded below the opening price of US$5,095.35 all day, touching lows of $5,045.54 currently, for losses of -0.6%. Today's moves re-affirm the MACD which shows the MACD line (white) below the Signal line (red), which suggests that bearish momentum remains in the price action.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 12/02/2026 | 0700/0700 | *** | UK Monthly GDP | |

| 12/02/2026 | 0700/0700 | ** | Trade Balance | |

| 12/02/2026 | 0700/0700 | ** | Index of Production | |

| 12/02/2026 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/02/2026 | 0700/0700 | ** | Index of Services | |

| 12/02/2026 | 0700/0700 | *** | GDP First Estimate | |

| 12/02/2026 | 0900/1000 | ECB's Cipollone At Commissione Europa Conference | ||

| 12/02/2026 | - | BOE MPG Meeting | ||

| 12/02/2026 | - | *** | New Loans | |

| 12/02/2026 | - | *** | Money Supply | |

| 12/02/2026 | - | *** | Social Financing | |

| 12/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 12/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 12/02/2026 | 1345/0845 | BOC's Rogers panel talk on productivity | ||

| 12/02/2026 | 1500/1000 | *** | NAR existing home sales | |

| 12/02/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 12/02/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/02/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/02/2026 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/02/2026 | 1830/1930 | ECB's Lane At The World Ahead 2026 Gala Dinner | ||

| 12/02/2026 | 0000/1900 | Fed's Lorie Logan, Stephen Miran | ||

| 13/02/2026 | 0700/0800 | * | Wholesale Prices | |

| 13/02/2026 | 0730/0830 | *** | CPI | |

| 13/02/2026 | 0800/0900 | *** | HICP (f) | |

| 13/02/2026 | 1000/1100 | *** | EZ GDP 2nd (Flash) | |

| 13/02/2026 | 1000/1100 | * | Employment | |

| 13/02/2026 | 1000/1100 | * | Trade Balance | |

| 13/02/2026 | 1000/1100 | ECB's de Guindos Lecture At Academia Europea Leadership | ||

| 13/02/2026 | 1200/1300 | ECB's de Guindos Remarks and Q&A At Círculo de Confianza | ||

| 13/02/2026 | 1200/1200 | BOE's Pill Fireside Chat At Santander Macro Event |