MNI EUROPEAN OPEN: Japan FX Jawboning Returns

EXECUTIVE SUMMARY

- SCHMID SAYS FED MUST MAINTAIN CREDIBILITY ON INFLATION - MNI

- TRUMP OPEN TO HEALTHCARE TALKS WITH DEMOCRATS AMID SHUTDOWN - WSJ

- TRUMP PUSHES FOR ISRAEL, HAMAS DEAL AS TALKS KICK OFF - BBG

- JAPAN'S KATO: WILL CLOSELY WATCH ANY EXCESSIVE FX MARKET MOVES - BBG

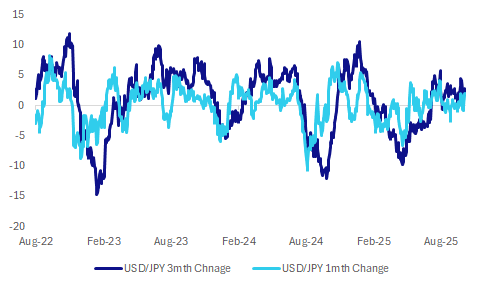

Fig 1: USD/JPY 1mth & 3mth Rate Of Change, Below Recent Peaks

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

UKRAINE (BBC): “British microcomputers were among more than 100,000 foreign-made parts contained in Russian missiles and drones used in Sunday's deadly strikes on Ukraine, Volodymyr Zelensky has said.”

POLITICS (TIMES): “The Conservatives have likened Nigel Farage to Jeremy Corbyn as part of an attempt to brand Reform UK as “the party of more spending and more debt”. Sir Mel Stride, the shadow chancellor, accused Farage of “marching to the left” on economics.”

GOVERNMENT (TIMES): “Britain’s most senior civil servants have told ministers their pledge to oversee a “digital revolution” in Whitehall is stalling because the government is “spectacularly bad” at rapidly harnessing the potential of new technology.”

EU

FRANCE (BBC): “Hours after quitting, Lecornu accepted a request from French President Emmanuel Macron to work on a plan for the "stability for the country" by Wednesday evening.”

EU (POLITICO): “The European Commission president faces another set of no-confidence votes on Thursday. She hopes that by listening more, she’ll bolster her support.”

GERMANY/RUSSIA (DW): “"He is waging an information war against us. He is waging a military war against Ukraine and this war is directed against all of us," Merz told broadcaster NTV on Monday. He said Putin aims to undermine Europe’s political order and that supporting Ukraine is in Germany’s interest to defend open, liberal societies.”

UKRAINE (DW): “The International Atomic Energy Agency (IAEA) has reported that its team at Ukraine’s Zaporizhzhia nuclear power plant heard multiple rounds of incoming and outgoing shelling near the site on Monday.”

UKRAINE (MNI BRIEF): EU member states' guarantees for a proposed EUR140bn reparations loan to Ukraine is unlikely to add to their budget deficits and debt levels, a senior EU official said Monday, although noting that a final decision would rest with Eurostat.

US

GOVERNMENT (WSJ): “ President Trump signaled a willingness to strike a deal on funding healthcare subsidies demanded by Democrats, as the government shutdown entered its second week.”

FED (MNI): Kansas City Fed President Jeff Schmid said Monday that monetary policy must remain restrictive in the face of an inflation path that remains unacceptably elevated.

TARIFFS (BBG): " President Donald Trump said 25% duties on medium- and heavy-duty trucks would begin Nov. 1, the latest expansion of his tariff regime aimed at protecting domestic industries."

OTHER

MIDDLE EAST (BBC): “Indirect talks aimed at reaching a final agreement on a US peace plan to end the war in Gaza have begun in the Egyptian city of Sharm El-Sheikh.”

MIDDLE EAST (BBG): " US President Donald Trump is pressing Israel and Hamas to secure a settlement to the two-year conflict that’s devastated Gaza and destabilized the Middle East, with the warring sides starting mediated negotiations.

GOLD (BBG): "Citadel’s Ken Griffin said investors are starting to view gold as a safer asset than the dollar, a development that’s “really concerning” to the billionaire investor."

JAPAN (BBG): " The Japanese ruling party’s new Secretary-General attempted to quell concerns over its long-standing coalition with junior party Komeito as it tries to navigate new partnerships."

JAPAN (BBG): "Japan’s Finance Minister Katsunobu Kato says he will closely watch any excessive moves in the forex market."

CANADA (MNI BRIEF): Canada's Finance Minister Francois-Philippe Champagne on Monday responded to an opposition question at a committee hearing about Canada's deficit reaching CAD90 billion to meet a higher NATO target by saying: “Are you suggesting that we should not meet our NATO commitments?”

CHINA

GOLD (BBG): "The People’s Bank of China added to its gold holdings in September for an 11th consecutive month, extending its buying streak as bullion climbed to fresh record levels."

MARKET DATA

AUSTRALIA OCT. WESTPAC CONSUMER CONFIDENCE 92.1; SEP. 95.4

AUSTRALIA OCT. WESTPAC CONSUMER CONFIDENCE -3.5% M/ML SEP. -3.1%

AUSTRALIA SEPT. ANZ JOB ADVERTISEMENTS -3.3% M/M; AUG. -0.3%

JAPAN AUG. HOUSEHOLD SPENDING ROSE 2.3% Y/Y; AUG. +1.4%

MARKETS

US TSYS: Yields Unchanged In A Quiet Session

The TYZ5 range has been 112-12+ to 112-15 during the Asia-Pacific session. It last changed hands at 112-14, up 0-01+ from the previous close.

- The US 2-year yield is trading 3.586%.

- The US 10-year yield is trading around 4.15%.

- 10-Year yields bounced on the back of global politics but remains subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around 4.20% initially and look to fade the move higher.

- Bloomberg - “Global Long Bonds Can Breathe Easier After 30-Year JGB Sale. Japan’s thirty-year auction went off smoothly with a higher bid-to-cover ratio than the previous sale, which will be a relief for investors across G-10 long-term debt. Traders will also be reassured with MUFJ-MS taking up the biggest slice of the bonds, along with Japan’s other big primary dealers.”

- Gavekal on X: “With the Bureau of Labor Statistics temporarily dark due to the US government shutdown, investors and the Federal Reserve must rely on other employment data. Worryingly, ADP’s private payroll estimate showed its most significant contraction of this cycle. That could be the result of the immigration crackdown reducing the supply of available workers. It is also possible that slack is starting to appear in the labor market, perhaps due to the temporary fiscal contraction from tariffs or AI causing unemployment, especially among young graduates. The recent decline in jobless claims is encouraging, but it is worth noting that many young graduates do not have prior work history and thus may not be eligible to claim unemployment benefits.”

JGBS: 30Y Auction Result Sparks A Massive Long-End Rally

JGB futures remain weaker, -6 compared to settlement levels, but well off lows after today’s less weak than feared 30-year auction.

- The 30-year JGB auction delivered mixed results. However, the 30-year has rallied strongly following the result, suggesting that the recent bear-steepening was overdone. Although newly elected Liberal Democratic Party leader Sanae Takaichi is perceived to have an expansionary fiscal and monetary policy stance, a lot of these expectations appear to have been priced into the market.

- MNI - Japan household spending for August was stronger than forecast (+2.3%y/y, versus 1.2% forecast, 1.4% prior). We are below earlier 2025 highs from a y/y momentum standpoint, but the trend has steadily improved from late 2024 lows. It should add, albeit at the margins, to the case for a further BoJ rate hike, although little is priced for the Oct meeting.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs have twist-flattened across benchmarks after today’s 30-year auction. The benchmark 30-year yield is 3.9bps lower at 3.267% after setting a fresh cycle high of 3.351% earlier in the session.

- Swap rates are flat to 7bps lower, with swap spreads tighter.

- Tomorrow, the local calendar will see Cash Earnings, BoP Current Account Balance and Trade Balance data.

AUSSIE BONDS: Modestly Richer After Weak Data, Mar-36 Supply Tomorrow

ACGBs (YM +1.5 & XM +0.5) sit modestly higher after today’s weak data.

- "Australia's consumer confidence slipped to a six-month low this month on renewed doubts about hopes of future interest rate cuts given recent strength in inflation." - BBG

- ANZ-Indeed job advertisements dropped 3.3% from a month earlier in September, the largest monthly decline since February 2024.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after today’s 30Y JGB auction sparked a relief rally in global bonds. Cash US tsys had been 1bp cheaper earlier. Although newly elected Liberal Democratic Party leader Sanae Takaichi is perceived to have an expansionary fiscal and monetary policy stance, a lot of these expectations appear to have been priced into the market.

- Cash ACGBs are 2-6bps cheaper, after being closed yesterday, with the AU-US 10-year yield differential at 24bps.

- The bills strip is +1 to +2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in November is given a 39% probability, with a cumulative 13bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond tomorrow.

- Tomorrow, the local calendar will also see Foreign Reserves data.

BONDS: NZGBS: Solid & Relative Performance Ahead Of Tomorrow’s RBNZ Decision

NZGBs closed just off session bests, 1-2bps richer, ahead of tomorrow’s RBNZ Policy Decision.

- On a relative basis, NZGBs' performance was even more impressive with the NZ-US and NZ-AU 10-year yields differentials finishing 4bps tighter on the day.

- Cash US tsys are flat in today's Asia-Pac session after yesterday's modest sell-off.

- After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October.

- The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting, but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. (See MNI RBNZ Preview here)

- RBNZ dated OIS pricing closed slightly softer across meetings. 36bps of easing is priced for tomorrow, with a cumulative 63bps by November 2025.

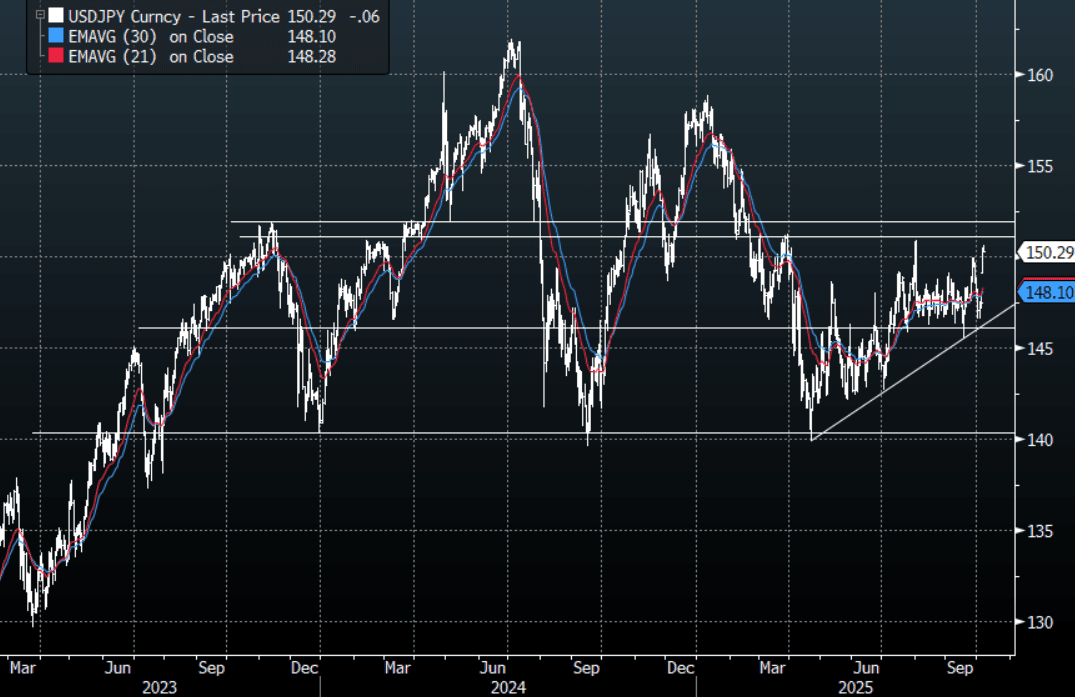

JPY: Asia Wrap - USD/JPY Consolidates Gains Above 150.00

The USD/JPY range has been 150.24 - 150.62 in the Asia-Pac session, it is currently trading around 150.30, -0.03%. The pair looks to be consolidating its gains above 150.00 after the surge higher in reaction to Sanae Takaichi’s victory. The market's attention has quickly returned to a potential looser fiscal and monetary policy on this outcome and looks to be pushing back the likelihood of an imminent rate hike. With risk roaring higher this all feeds further into the carry trade, the focus will now turn toward the pivotal 151/152 area a break of which could potentially start another leg higher. Expect dips to now find support unless there is push back on the market's views of Takaichi’s policies. There was some jaw-boning today about FX moves but realistically I would not expect any action until we cross back above the 155 area.

- The last CFTC data available showed Asset Managers remained significantly long JPY, should these moves begin to gather momentum, they could be forced to first pare back their longs and then if significant levels are broken begin to rebuild JPY shorts. Many crosses are breaking through some pivotal areas(CNH/JPY Above 21.00) and unless the government says something to contradict the markets thinking these could begin to gather momentum.

- MNI - Household Spending Above Forecasts, Supports BoJ Hike Plans : Japan household spending for August was stronger than forecast (+2.3%y/y, versus 1.2% forecast, 1.4% prior). We are below earlier 2025 highs from a y/y momentum standpoint, but the trend has steadily improved from late 2024 lows. It should add, albeit at the margins, to the case for a further BoJ rate hike, although little is priced for the Oct meeting (implied rate of 0.52%, versus a current effective rate of 0.477%).

- "KATO: KEY FOR FX TO MOVE STABLY WHILE REFLECTING FUNDAMENTALS, REFRAINING FROM COMMENTING SPECIFICALLY ON MARKET MOVES" - BBG

- "SUZUKI: CAN'T IGNORE FISCAL DISCIPLINE, CAN'T ACHIEVE JAPAN GROWTH WITHOUT INVESTMENT” - BBG

Options : Close significant option expiries for NY cut, based on DTCC data: 149.75($895m), 150.00($796m), 151.00($776m). Upcoming Close Strikes : 147.00($1.47b Oct 8) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

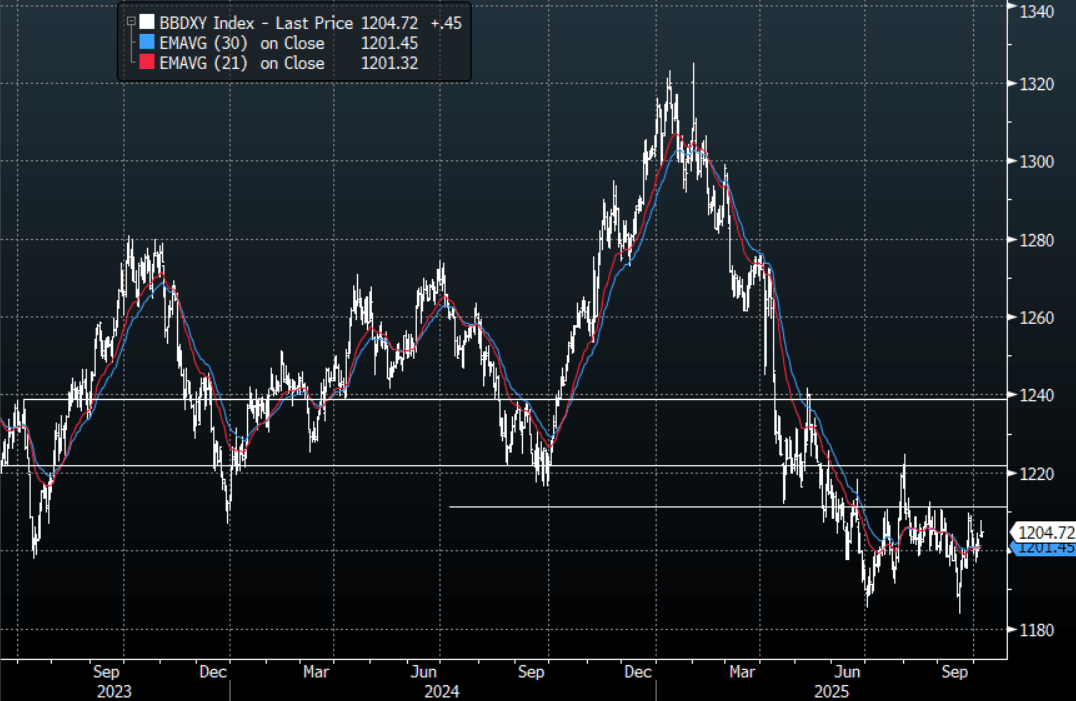

FOREX: Asia FX Wrap - The BBDXY Consolidates Gains Back Above 1200

The BBDXY has had a range of 1203.59 - 1204.88 in the Asia-Pac session; it is currently trading around 1204, -0.02%. The USD got a welcome reprieve from the surge in USD/JPY, after failing to build any downward momentum below 1200 once more can the USD build on this? The USD has historically not done well during shutdowns, but tends to bounce back quite hard when they eventually end so the market will be waiting for any signs of a breakthrough. The 1215-1225 area remains tough resistance, only a close back above 1230 would start to get USD shorts to challenge their conviction.

- EUR/USD - Asian range 1.1697 - 1.1716, Asia is currently trading 1.1700. The pair found bids back toward 1.1650 overnight. The EUR remains stuck in a range with no clear direction, 1.1550-1.1850 has captured most of the move in the last few months.

- GBP/USD - Asian range 1.3473 - 1.3487, Asia is currently dealing around 1.3470. The pair could not break through its support around the 1.3300 area, price has bounced back into the range. The market should find supply towards the 1.3500 area initially, the wider 1.3300-1.3700 range continues to dominate.

- USD/CNH - Asian range 7.1361 - 7.1445, Asia is currently dealing around 7.1370. The area around 7.1500/1600 has proved to be solid resistance for now, it looks likely we could consolidate 7.09-7.16 for the moment.

- Cross asset : SPX -0.05%, Gold $3975, US 10-Year 4.148%, BBDXY 1204, Crude Oil $61.77

- Data/Events : Germany Factory Orders, France Trade Balance, Italy Istat Releases Data on Households Consumptions in 2024

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

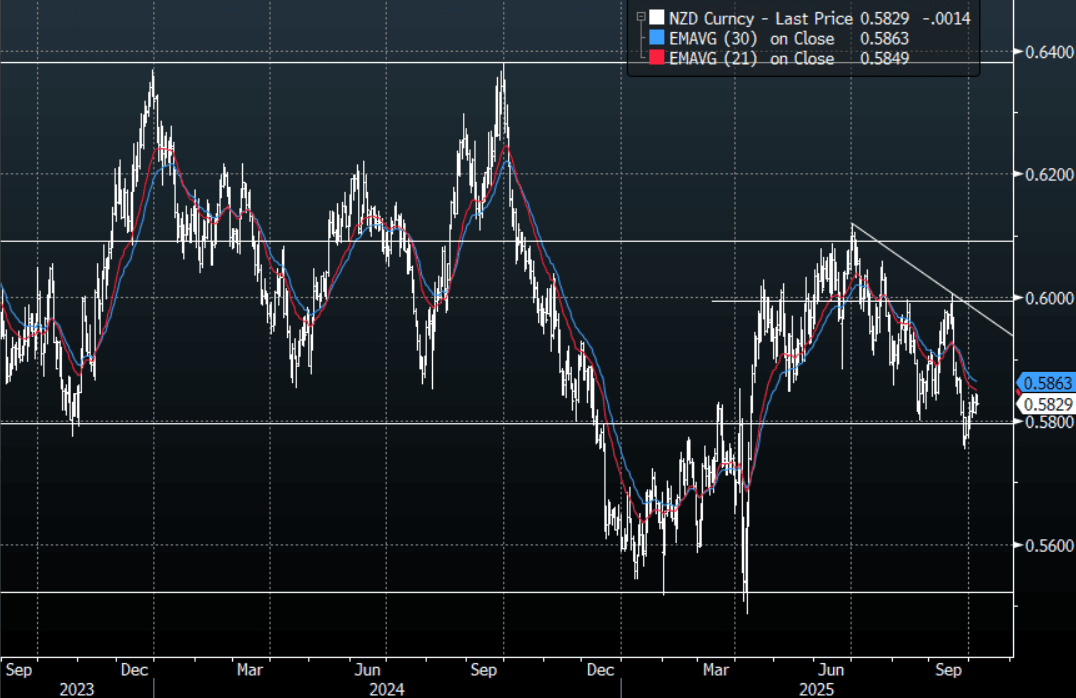

NZD: Asia Wrap - NZD/USD Trades Heavy Toward 0.5850

The NZD/USD had a range of 0.5824 - 0.5843 in the Asia-Pac session, going into the London open trading around 0.5830, -0.25%. US stocks continue to shrug off global politics and the US shutdown, the USD though got a boost from the reaction in USD/JPY. The NZD drifted higher, helped by the way risk continues to push up and probably some NZD/JPY demand as the JPY crosses turn back higher. The first sell zone should be between the 0.5850/0.5900 area for those still wanting to express a short.

- MNI - RBNZ Preview-October 2025: How Much To Ease? After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October. The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. 36bps of easing is priced for Wednesday’s meeting, with a cumulative 63bps by November 2025.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5820(NZD305m). Upcoming Close Strikes : none - BBG

- AUD/NZD range for the session has been 1.1324 - 1.1354, currently trading around 1.1350. The Cross has seen some selling to cap the move above 1.1400 for now, price action suggests we could potentially see more reversion back to the mean but expect dips back towards 1.1200 to now be supported.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Tech Related Plays Continue To Rally, Thailand Up Ahead Of BoT

Regional equity markets are still disrupted by holidays with China and South Korea remaining out, while Hong Kong markets are also out today. For those markets which are open, the tone is mostly positive, particularly tech sensitive plays. The on-going rally in US tech related indices amid AI/chip related gains is a positive for the region. The SOX rose 2.89% in Monday US trade, as AMD, the chip maker, announced a deal with OpenAI.

- Japan markets are tracking higher, with the NKY 225 up a further 0.75%, while the Topix is up 0.40%. There have been lots of headlines today, as the government looks to provide of cost of living relief but is also mindful of fiscal constraints (high debt to GDP the country faces). We also had stronger than expected household spending data, while FinMin Kato jawboned recent FX weakness. USD/JPY is little changed at this stage.

- The Topix Transport sub index is up a further 1.05%, while the banks index is down 0.49% (following yesterday's 1.89%). Incoming advisors to new PM Takaichi stated an Oct hike could be too soon for the BoJ.

- The Taiex index in Taiwan is up close to 2%, the fresh record highs. Chip bellwether TSMC continues to surge in local trade.

- In South East Asia the nest performer is Thailand up over 1.4%. This puts the index back above the 1300 level, back close to mid Sep highs. We ahve the BoT meeting tomorrow, where a rate cut is expected. Via the Bangkok Post: "The first set of measures focuses on simplifying initial public offering (IPO) rules to streamline listing procedures, reduce regulatory barriers and make the Thai market more competitive compared with regional peers." (announced by a Capital market taskforce) is also potentially helping sentiment.

- Other markets in the region are higher, although Malaysia is a laggard, down around 0.75%.

GOLD: Political Instability Supportive, Tuesday Sees Numerous Fed Speakers

Gold made another record high during Tuesday’s APAC trading despite little change in either the US dollar or yields. Safe-haven flows continue to push bullion towards psychological round number support at $4000 given ongoing government instability in the US, Japan and France. Gold reached $3977.44/oz earlier but then fell to $3956.02. It is currently up 0.3% to $3974.5.

- The US shutdown appears no closer to a resolution although both sides are willing to talk but the issue may be forced as 14 October approaches, when military personnel will miss their first paycheck. Polymarket has higher odds of the shutdown lasting 10-29 days rather than more than 30. The impasse is delaying key US data increasing opacity at a time of economic uncertainty and as the Fed resumes easing.

- With no political group having a majority in the French parliament and an unwillingness to cooperate, instability is likely to continue. The latest PM, Lecornu, resigned on Monday but President Macron has asked him to find a solution. The situation has unsettled markets given France’s high deficit and debt positions.

- Policy under Japan’s new PM Takaichi is also uncertain given her desire to reduce the consumption tax and previous comments against BoJ rate hikes.

- ETF inflows and central bank purchases have driven a $600 upward revision to Goldman Sachs’s end-2026 gold projection to $4900/oz, according to Bloomberg.

- Silver is little changed at $48.55 after reaching $48.653 below Monday’s high of $48.767.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.

OIL: Crude Holds Onto Post-OPEC Gains, US EIA Energy Report Out Later Today

Oil prices have continued their post-OPEC relief rally during today’s APAC session following Monday’s 1.5% rise as it unwinds some of last week’s sharp sell off. The market had worried that the November increase would exceed October’s but in the end it was in line. There was also another strike on a Russian refinery, a trend that may pick up pace as Ukraine tries to impact funds for Russia’s war and it receives more US intelligence.

- WTI moved in a narrow range and is up 0.3% to $61.87/bbl slightly off the intraday high of $61.94. It had fallen to $61.65 early in the session. Brent is 0.3% higher at $65.67/bbl after reaching $65.73.

- The market has been driven by geopolitical developments, especially related to Ukraine-Russia, and excess supply worries, which have diverging effects on oil prices. Later today the EIA short-term energy outlook will be published with the IEA and OPEC’s monthly reports next week.

- The EIA has said that it is continuing its normal schedule for now despite the US shutdown, which also includes its weekly energy data. Industry-based inventories will be released on Tuesday. Stock data remain important as builds are expected as the market shifts into surplus.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 07/10/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/10/2025 | 0645/0845 | * | Foreign Trade | |

| 07/10/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 07/10/2025 | 1400/1000 | * | Ivey PMI | |

| 07/10/2025 | 1405/1005 | Fed's Miki Bowman | ||

| 07/10/2025 | 1430/1030 | Fed Governor Stephen Miran | ||

| 07/10/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/10/2025 | 1530/1130 | Minneapolis Fed's Neel Kashkari | ||

| 07/10/2025 | 1610/1810 | ECB Lagarde Speech at Business France Event | ||

| 07/10/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 07/10/2025 | 1900/1500 | * | Consumer Credit | |

| 07/10/2025 | 2005/1605 | Fed Governor Stephen Miran | ||

| 08/10/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 08/10/2025 | 2330/0830 | ** | average wages (p) | |

| 08/10/2025 | 2350/0850 | Balance of Payments | ||

| 08/10/2025 | 0100/1400 | *** | RBNZ official cash rate decision | |

| 08/10/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/10/2025 | 0600/0800 | ** | Industrial Production | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 08/10/2025 | 1030/1230 | ECB Elderson In Panel at Finance Conference | ||

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr |