MNI EUROPEAN OPEN: Fresh US-China Tensions Hits Risk Appetite

EXECUTIVE SUMMARY

- CHINA HITS BACK AT US ON SHIPPING WITH HANWHA CURBS, NEW PROBE - BBG

- PAULSON SAYS FED SHOULD MOVE CAUTIOUSLY IN DEBUT SPEECH - MNI

- RBA SEES STRONGER Q3 CPI - MINUTES - MNI BRIEF

- RBNZ TO ADJST LVR SETTINGS - MNI BRIEF

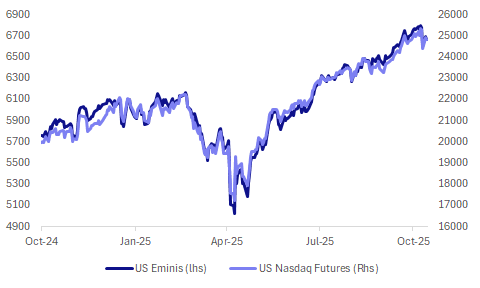

Fig 1: US Equity Futures

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

ECONOMY (TIMES): “The BRC blamed lacklustre consumer confidence amid fervent speculation about tax increases at the budget on November 26 for the decline in consumption growth. Wet and windy weather is likely to have also played a role.”

POLITICS (TIMES): “Wes Streeting: I’m glad we can now admit that Brexit is a problem. Health secretary delighted by Times report saying the PM and chancellor are planning to pin blame on Nigel Farage for tax hikes in the budget.”

EU

TECH (BBC): “The Dutch government has taken control of Nexperia, a Chinese-owned chipmaker based in the Netherlands, in a bid to safeguard the European supply of semiconductors for cars and other electronic goods and protect Europe's economic security. The Hague said it took the decision due to "serious governance shortcomings" and to prevent the chips from becoming unavailable in an emergency.”

TECH (POLITICO): “Right on the Russian border, Europe’s first commercial-scale rare-earth magnet factory is starting to supply automotive and green tech customers from a forgotten corner of Estonia. The project represents an act of defiance against Russian aggression. It’s a bid to counter China’s chokehold over critical minerals.”

FISCAL (MNI BRIEF): Reduced Euro Area fiscal space is a good reason why banks need to reinforce their resilience, ECB Supervisory Board Chair Claudia Buch said Monday. "One of the things we see is that risk premia are relatively compressed right now and valuations are also relatively high and this is why we have been arguing we need sufficient resilience in case market sentiment changes," she told the European Parliament's ECON Committee.

UKRAINE/US (BBG): “Ukrainian President Volodymyr Zelenskiy plans to meet with US President Donald Trump in Washington this week to discuss air defense, long-range weaponry and energy as Russia intensifies strikes on the war-battered nation’s energy system.”

US

FED (MNI BRIEF): Federal Reserve Bank of Philadelphia President Anna Paulson said Monday in her first speech as an FOMC member the central bank should move cautiously and the median projection for two more cuts this year is appropriate if economic and financial conditions evolve as expected.

TECH (BBG): “Broadcom Inc. became the latest chipmaker to forge a blockbuster data center deal with OpenAI, triggering a rally that added more than $150 billion to its market value.”

OTHER

AUSTRALIA (MNI BRIEF): The Reserve Bank of Australia Board judged that September quarter inflation could be higher than expected and that the combination of stronger inflation and a steady labour market might imply staff had underestimated demand relative to supply, minutes of the September meeting showed Tuesday.

NEW ZEALAND (MNI BRIEF): The Reserve Bank of New Zealand will ease mortgage loan-to-value ratio (LVR) restrictions from Dec 1, increasing the share of new lending allowed at higher LVRs, the central bank said in a statement Tuesday.

JAPAN (BBG): "Japan’s main opposition parties are likely to meet Tuesday as they weigh the possibility of rallying behind Yuichiro Tamaki as a unified candidate to take on ruling party leader Sanae Takaichi in a parliamentary vote to decide the prime minister. "

ARGENTINA (BA TIMES): “President Javier Milei visits the White House on Tuesday, banking on a high-profile show of political and economic support from his US ally President Donald Trump ahead of key midterm elections. Trump's administration has already promised US$20-billion to prop up Argentina's economy and repeatedly voiced political support for Milei.”

CHINA

US/CHINA (BBG): "China has imposed curbs on the American units of Hanwha Ocean Co., one of South Korea’s biggest shipbuilders, as it targets US measures against the Chinese shipping sector."

US/CHINA (BBG): "China dismissed complaints from the US that it didn’t respond to inquiries over its latest export curbs on rare earths, saying Beijing has been maintaining communications over trade issues despite recent tensions.

SHIPPING (MINISTRY OF TRANSPORT): "Beijing has begun imposing special port fees on vessels that are U.S.-built or U.S.-flagged when calling at Chinese ports, according to an announcement from the Ministry of Transport."

MNI: PBOC Net Injects CNY91 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY91 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY91 billion as no reverse matures today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4220% at 09:57 am local time from the close of 1.4495% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 45 on Monday, compared with the close of 46 on Saturday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1021 Tues; -0.30% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1021 on Tuesday, compared with 7.1007 set on Monday. The fixing was estimated at 7.1354 by Bloomberg survey today.

MARKET DATA

UK SEPT. BRC LIKE-FOR-LIKE RETAIL SALES +2% Y/Y; EST. +2.5%; AUG. +2.9%

NEW ZEALAND SEPT. RETAIL CARD SPENDING -0.5% M/M; AUG. +0.6%

NEW ZEALAND SEPT. TOTAL CARD SPENDING -0.4% M/M; AUG +0.4%

AUSTRALIA SEPT. NAB BUSINESS CONDITIONS +8; AUG. +8

AUSTRALIA SEPT. NAB BUSINESS CONFIDENCE +7; AUG. +4

JAPAN SEPT. M3 MONEY STOCK +1.0% Y/Y; AUG. +0.8%

JAPAN SEPT. M2 MONEY STOCK +1.6% Y/Y; AUG. +1.3%

MARKETS

US TSYS: Move Higher in Yields Stalls in the Afternoon

- As treasuries began trading in the Asia trading day, yields across the curve opened 1-3bps higher before taking back some of the early moves.

- The US 2-Yr traded up at 3.515%, but rallied back to again test a near term support of 3.50% that it has been unable to hold below.

- The US 5-Yr is back to flat at 3.63% having been +2bps higher in the morning session.

- The US 10-Yr is up +1bps to 4.04%, having opened at 4.06%. Last week it failed to test 4.00% and looks likely to remain in the 4.00% - 4.20% range for now, seeking a fresh catalyst to break out. With FED speakers in coming days and the FEDs Powell's economic address at the NABE meeting, treasury traders will be looking for signals for monetary policy that could challenge this current range.

- The US 30-Yr is up +2bps at 4.64% just off the Tuesday morning high of 4.65%.

- Futures are edging lower too as TYZ5 is has not traded too far from where it started the day and is currently +01 at 113-06

JGBS: Futures Bid On Risk Aversion, But Sub Resistance, Tamaki PM Odds Firm

Like elsewhere, JGB futures have caught a bid as fresh US-China tensions (this time centered on the shipping sector), drive safe haven flows into bonds. The 10yr future was last 136.39, +.49, versus settlement levels. Key short-term resistance has been defined at 137.30, the Sep 8 high, so we are still some distance away but this bounce is challenging the recent bearish break of 136.19, the Sep 4 low.

- The China announcement targets US shipping entities via Hanwha Ocean, a large South Korean shipbuilder. The authorities also provided details on a broader probe into the impact of the US investigation into China shipping (mkt jitters with be heightened given the potential for escalation from here).

- In the cash JGB yield space, shifts lower have accelerated, led by the 7yr down 5bps. to 1.41%. The 10yr is back to 1.66%, while the 30 and 40yr tenors are holding around 2bps higher.

- The 2/30s curve is maintaining a steepening bias, last +234bps, +5.5bps.

- The other focus point remains domestic politics. "*TAMAKI: WILL HOLD 3-WAY DPP, ISHIN, CDP SEC-GEN MEETING TODAY" (via BBG). There is a possibility of former LDP coalition partner Komeito backing a non-LDP candidate for PM (based off comments yesterday). Tamaki's, the leader of the DPP, PM odds have risen to +17.5, per Polymarket. Note earlier this year Tamaki "urged the BOJ to loosen, not tighten, monetary policy to keep the yen from rising and hurting the export-reliant economy." (via Asahi).

- Note tomorrow has a 20yr debt auction.

AUSSIE BONDS: Futures Bid Fresh On US-China Tensions, AU-US 10yr Spread Lower

Futures have caught an afternoon bid amid renewed risk aversion centred on US-China tensions. 10yr futures (XM) were last +4bps to 95.73, while 3yr (YM) were at 96.505, +3bps. Upside focus will rest on Sep 12 highs, 95.78 for the 10yr and 96.615 for the 3yr. Broader risk aversion is higher, as China imposed curbs on the US units of Hanwha Ocean, a large South Korean shipbuilder. It also provided details on a broader probe into the impact of the US investigation into China shipping).

- AUD/USD is the weakest performed in the FX space, and will remain quite sensitive to US-China related developments, particularly from a proxy/risk standpoint.

- ACGB yields are lower across the board, off 2-3.5bps. As we noted yesterday, fresh US-China tensions, with no off ramp, could bring RBA easings back to play if it impacts the global/China growth outlook enough.

- The AU-US 10 spread is off recent highs, last +22bps (from +33bps on Friday).

- Earlier, the September NAB business survey showed the gradual recovery in the Australian economy continued. While, the RBA minutes clearly reflected the Board’s caution at the 30 September decision to keep rates unchanged. Its “decisions”, ie. not just last month’s, “remain cautious and data dependent”. Thus the outcomes of releases between now and 4 November are very important and the tone of the minutes was clear that a rate cut at that meeting is not a given.

BONDS: NZGBS: Softer Yields, Sep Card Spend Down, RBNZ Eases LVR

NZGB yields have held modestly softer across most of the benchmarks as Tuesday's session unfolded. Outside of a steady 2yr at 2.60%, most other parts of the curve are close to 1bps (although the 10yr is little changed at 4.075%). This comes despite US Tsys resuming cash trading with a firmer bias, this has faded as the session progressed, with fresh China shipping curbs on the US weighing on risk appetite (10yr back under 4.04%). Earlier data showed card transactions falling in Sep, while the RBNZ adjusted loan regulations (essentially easing NZ financial conditions), helping relative NZ yield trends.

- The NZ-US 10yr rate differential is slightly lower, last at +5bps, up a touch from recent lows sub 0bps. So far in Oct, this spread hasn't been able to sustain +10bps levels.

- New Zealand 2yr swap is near 2.37%, little changed for the session, but still close to recent lows near 2.35% and maintaining a downtrend bias.

- September retail card transactions fell 0.5% m/m after rising 0.6%, the first negative after three consecutive increases. Annual growth slowed to 1.2%. Despite the soft end to Q3, the quarter saw a 0.6% q/q increase in nominal retail spending.

- The Reserve Bank of New Zealand will ease mortgage loan-to-value ratio (LVR) restrictions from Dec 1, increasing the share of new lending allowed at higher LVRs, the central bank said in a statement Tuesday. For owner-occupiers, the limit on loans with an LVR above 80% will rise to 25% from 20%, while for investors, the limit on loans with an LVR above 70% will increase to 10% from 5%.

- Looking ahead, Thursday delivers Sep food prices, ahead of the all important Q3 CPI, out next Monday.

FOREX: AUD/USD Testing Friday Lows Amid Fresh US-China Tensions

Higher beta FX, most notably AUD, has underperformed in the Asia Pac afternoon session, particularly against yen. AUD/USD is at 0.6475/80, down 0.60%, and challenging lows from late Friday (when Trump announced a fresh tariff threat against China). NZD/USD is near 0.5700, which is fresh multi month lows. USD/JPY is back under 152.00, against earlier highs of 152.61. Risk aversion has returned after The China announcement targets US shipping entities via Hanwha Ocean, a large South Korean shipbuilder. The authorities also provided details on a broader probe into the impact of the US investigation into China shipping.

- US equity futures are lower, off 0.35% for Eminis, while Bitcoin losses sit close to 2% for the session. Bond markets have seen a safe haven bid. Sentiment has been whipsawed after more positive comments from the US over the week and yesterday (while China tried to play down its rare earth export controls) aided a risk rebound on Monday.

- For AUD/USD, it is likely to remain particularly sensitive to US-China developments. Today's softness undermines the recent bullish theme and instead signals scope for a deeper retracement, potentially towards key support at 0.6415, the Aug 21 and 22 low. Initial resistance to watch is 0.6560, the 50-day EMA.

- AUD/JPY is back close to 95.40, still above Friday lows sub 98.00.

- For NZD/USD we haven't been sub 0.5700 since April of this year.

- USD/JPY has also been aided by further jawboning from FinMin Kato, although it didn't appear to represent a step up on recent FX rhetoric. Japan politics remains in focus as minor parties meet to potentially put forward a candidate for PM.

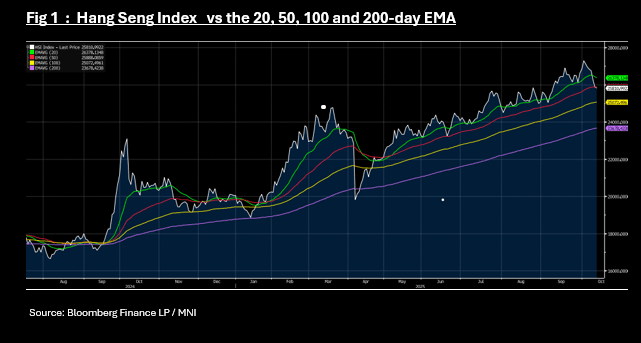

ASIA STOCKS: Equities Remain Weak as HSI Breaks Through Key Technical

With Japan back today playing catch up from yesterday's weakness, most key markets in the region have moved lower Tuesday. This comes despite the better global risk tones on Monday, as Trump softened his language around China (after tariff threats late on Friday).

Having closed at new highs Thursday, the NIKKEI's falls started Friday on apparent profit taking which was then over ran by Trump's comments as risk appetite declined. Out yesterday for a public holiday, Japanese investors continued to sell today taking the NIKKEI lower by -1.30%.

In Hong Kong the Hang Seng fell -0.45% today, despite trying to open stronger and traded through the 50-day EMA of 25,886. Were the HSI to hold below the 50-day EMA it would be the first time since the trade war induced sell off from April which then resulted in a near on five month rally to new highs. Other key Chinese bourses did little holding near to opening levels.

The KOSPI was a regional exception jumping +0.50% today as the 19% constituent - Samsung - beat profit estimates for its most recent quarter and its biggest quarterly profit in three years.

Following a terrible end to September for the NIFTY 50, it has rallied seven out of nine trading days in October. Against the regionally weak backdrop yesterday, the NIFTY 50's fall of -0.23% was a relative outperformance and in opening trade Tuesday it has recovered yesterday's falls.

OIL: Crude Range Trading As Watching US-China & Supply/Demand Developments

Oil prices are slightly higher but have been trading within a narrow range during today’s APAC session with no new developments to give it direction. Later on Tuesday though, the IEA’s October report, US industry-based inventory data and Fed Chair Powell comments on the economy have the potential to move crude. Brent is up 0.4% to $63.56/bbl off the intraday low of $63.41 following a peak of $63.63. WTI is 0.4% higher at $59.72/bbl after reaching $59.82. The USD index is slightly lower.

- OPEC left its oil market outlook unchanged with demand forecast to rise by 1.3mbd in 2025 and 1.4mbd in 2026. The IEA releases its monthly report Tuesday and tends to be less optimistic than OPEC. It has been projecting a record market surplus for 2026.

- US-China working-level trade talks occurred on Monday and China reiterated today its right to control rare earth exports and that the US should negotiate. Oil is likely to sell off if there is any deterioration in the situation as it remains concerned about the impact on energy demand from increased protectionism.

- Later Fed Chair Powell speaks on the economic outlook and monetary policy. The Fed’s Bowman, Waller and Collins, ECB’s Machado, Cipollone and Donnery, and BoE’s Bailey and Taylor also appear. US September NFIB small business optimism, UK labour market data and German September HICP and euro area October ZEW print.

Gold Continues Rally Without New Drivers

Gold has continued to rally today despite a flat US dollar, 2-year yields and S&P e-mini as it appears to be carried by momentum with no new fresh catalysts. It is now up 7.8% in October and currently 1.3% higher at $4164.0/oz today, around the record high of $4164.24, above resistance at $4161.7. US-China working-level trade talks occurred on Monday and China reiterated today its right to control rare earth exports and for the US to negotiate. Gold & silver are looking even more stretched.

- After rising over 4% on Monday, silver continued to rally Tuesday driven by momentum and significant liquidity issues in London. The metal is up 1.6% to $53.20 today after an all-time high of $53.465 earlier in the APAC session, above the fourth resistance level at $52.689, a Fibonacci projection. It is now up over 14% this month.

- Societe Generale revised up its gold forecast to $5000/oz for end-2026, according to Bloomberg, due to strong ETF and central bank flows, which had exceeded its expectations.

- The ongoing US government shutdown is also supporting precious metals with no apparent progress to end the impasse. Wednesday military personnel will miss their first pay but President Trump has said money will be found. It would be the first time in modern US history if it occurs.

- US September CPI was scheduled for 15 October but has now been delayed to 24 October contributing to difficulty in gauging where the economy is ahead of the 29 October Fed decision.

- Later Fed Chair Powell speaks on the economic outlook and monetary policy. The Fed’s Bowman, Waller and Collins, ECB’s Machado, Cipollone and Donnery, and BoE’s Bailey and Taylor also appear. US September NFIB small business optimism, UK labour market data and German September HICP and euro area October ZEW print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0750/0950 | ECB Cipollone Speech on Digital Euro | ||

| 14/10/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 14/10/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 14/10/2025 | - | *** | Money Supply | |

| 14/10/2025 | - | *** | New Loans | |

| 14/10/2025 | - | *** | Social Financing | |

| 14/10/2025 | - | ECB Lagarde and Cipollone at G20 Meeting | ||

| 14/10/2025 | 1200/1300 | BOE Taylor Remarks and Fireside Chat at University of Cambridge | ||

| 14/10/2025 | 1230/0830 | * | Building Permits | |

| 14/10/2025 | 1245/0845 | Fed Governor Michelle Bowman | ||

| 14/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/10/2025 | 1610/1210 | BOC Sr Deputy Rogers fireside talk in Vancouver | ||

| 14/10/2025 | 1620/1220 | Fed Chair Jerome Powell | ||

| 14/10/2025 | 1700/1800 | BOE Bailey Fireside Chat at Institute of International Finance | ||

| 14/10/2025 | 1925/1525 | Fed Governor Christopher Waller | ||

| 14/10/2025 | 1930/1530 | Boston Fed's Susan Collins | ||

| 15/10/2025 | 0130/0930 | *** | CPI | |

| 15/10/2025 | 0130/0930 | *** | Producer Price Index | |

| 15/10/2025 | 0430/1330 | ** | Industrial Production | |

| 15/10/2025 | 0600/0800 | *** | Final Inflation Report | |

| 15/10/2025 | 0600/0800 | *** | Final Inflation Report | |

| 15/10/2025 | 0645/0845 | *** | HICP (f) | |

| 15/10/2025 | 0700/0900 | *** | HICP (f) | |

| 15/10/2025 | 0740/0940 | ECB de Guindos at Single Resolution Mechanism Conference | ||

| 15/10/2025 | 0800/0900 | BOE Ramsden in Panel at Resolution Mechanism Conference | ||

| 15/10/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 15/10/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 15/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 15/10/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/10/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/10/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/10/2025 | 1330/0930 | Fed Governor Stephen Miran |