MNI EUROPEAN OPEN: China PPI Deflation Continues, CPI Edges Up

EXECUTIVE SUMMARY

- TRUMP SAYS STEEP COPPER TARIFFS IN STORE AS HE BROADENS HIS TRADE WAR - RTRS

- TWO KEVINS BATTLE TO BE NEXT FED CHAIR IN TRUMP’S ‘APPRENTICE’ -STYLE CONTEST - WSJ

- TRUMP DELAYED RECIPROCAL TARIFFS AFTER BESSENT WANTED MORE TIME ON DEALS -WSJ

- CHINA JUNE CPI RISES TO FIVE MONTH HIGH - MNI BRIEF

- CHINA'S PRODUCER DEFLATION WORSENS AS WEAK DEMAND PERSISTS - BBG

- RBNZ LEAVES OCR AT 3.25% - MNI BRIEF

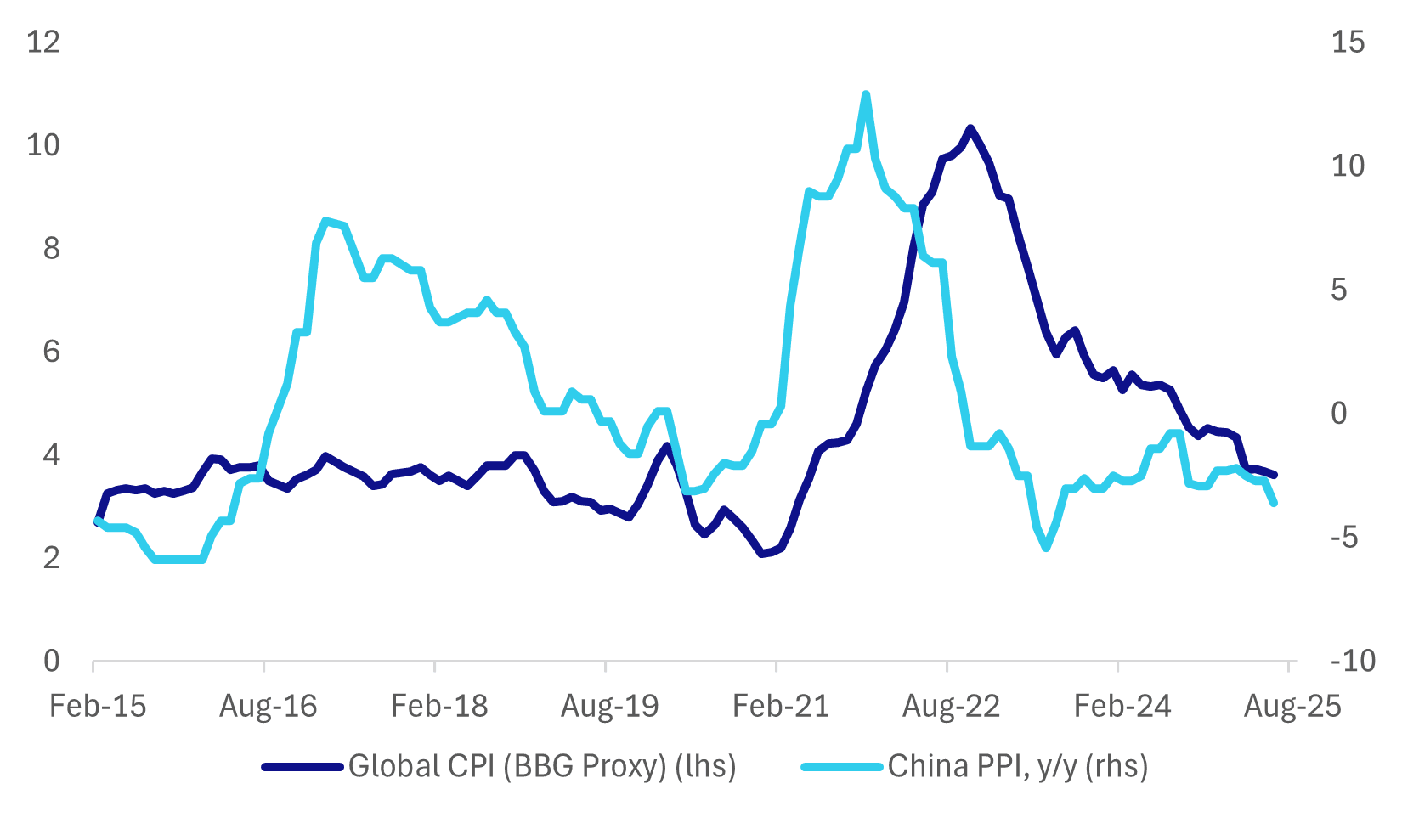

Fig 1: China PPI Y/Y & Global CPI Y/Y

Source: Bloomberg Finance L.P./MNI

UK

SHIPPING (BBG): “ The cost of shipping goods from China to the UK has surged due to ripple effects of the US trade war, threatening to push up consumer prices and complicate the Bank of England’s plan to keep nudging down interest rates.”

EU

DEBT (MNI INTERVIEW): Germany would be prepared to consider new joint European borrowing to boost defence in return for reforms of EU spending and state aid, with talks possible once the country’s federal budget has passed in September, the recently-appointed personal advisor to Finance Minister Lars Klingbeil told MNI.

UKRAINE/RUSSIA (BBG): “ President Donald Trump reiterated his displeasure with Vladimir Putin over the war in Ukraine and confirmed he’s sending more defensive weapons to President Volodymyr Zelenskiy’s government, sweeping aside an earlier pause by the Pentagon.”

UKRAINE (BBG): “The European Union is considering setting up a €100 billion ($117 billion) fund to support Ukraine as its war with Russia following Moscow’s full-scale invasion shows no signs of ending.”

US

TARIFFS (RTRS): “U.S. President Donald Trump on Tuesday said he would impose a 50% tariff on imported copper and soon introduce long-threatened levies on semiconductors and pharmaceuticals, broadening his trade war that has rattled markets worldwide.”

FED (WSJ): “Kevin Hassett, one of Trump's closest economic advisers, is emerging as a serious contender to be the next Fed chair, according to people familiar with the matter. Hassett's rise threatens the other Kevin -- former Fed governor Kevin Warsh -- an early favorite for the job who has angled for the position ever since Trump passed him over for it eight years ago. Some people close to the president worry that Warsh, who isn't in Trump's inner circle, won't be a champion of lower rates.”

TRADE (WSJ): “President Trump decided to delay the implementation of his so-called reciprocal tariffs to Aug. 1 after advisers including Treasury Secretary Scott Bessent told him he could get trade deals with more time, according to people familiar with the matter.”

INFLATION EXPECTATIONS (MNI): American consumers' expectations of inflation a year ahead declined in June by 0.2 pp to 3.02%, while three-year-ahead and five-year-ahead measures held steady from the prior month, according to the latest survey from the New York Federal Reserve published Tuesday.

OTHER

NEW ZEALAND (MNI BRIEF): The Reserve Bank of New Zealand’s monetary policy committee held the Official Cash Rate at 3.25% on Wednesday, signalling that further easing is likely if medium-term inflation pressures continue to decline as projected.

JAPAN (BBG): "One of the Bank of Japan’s newest board members alluded to a possible upward revision to the central bank’s inflation view this month, an outcome that would keep open the possibility of another rate increase this year."

CHINA

CPI (MNI BRIEF): China’s Consumer Price Index rose 0.1% y/y in June, ending four consecutive months of decline and reversing May’s 0.1% drop, beating market expectations for a 0.1% fall, according to data from the National Bureau of Statistics released Wednesday.

CPI (MNI BRIEF): Pork prices in China’s Consumer Price Index declined in June, marking a shift from the positive trend over the first six months of the year, as the overall index rebounded to a 0.1% rise y/y, official data showed on Wednesday.

PPI (BBG): “ China’s producer prices fell the most in nearly two years, deepening the country’s factory-gate deflation and overshadowing a modest improvement in consumer prices.”

GDP (YICAI): “China’s economy is expected to grow 5.07% y/y in Q2, slowing from 5.4% in Q1, Yicai.com reported, citing the average forecast of economists. First-half growth was mainly driven by front-loaded exports, counter-cyclical infrastructure investment, and the consumer trade-in programme, the newspaper said.

JOBS (SECURITIES TIMES): “The National Development and Reform Commission has allocated an additional CNY10 billion in central budget investment to launch a work-for-relief campaign aimed at boosting employment and incomes, Securities Times reported.”

MNI: PBOC Net Drains CNY23 Bln via OMO Wednesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY75.5 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY23 billion after offsetting the maturity of CNY98.5 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4497% at 09:54 am local time from the close of 1.4635% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 47 on Tuesday, compared with the close of 49 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1541 Weds; +1.25% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1541 on Wednesday, compared with 7.1534 set on Tuesday. The fixing was estimated at 7.1820 by Bloomberg survey today

MARKET DATA

NEW ZEALAND RBNZ OFFICIAL CASH RATE 3.25%; MEDIAN 3.25%; PRIOR 3.25%

JAPAN JUNE MONEY STOCK M2 Y/Y 0.9%; PRIOR 0.6%

CHINA JUNE CPI Y/Y 0.1%; MEDIAN -0.1%; PRIOR -0.1%

CHINA JUNE PPI Y/Y -3.6%; MEDIAN -3.2%; PRIOR -3.3%

SOUTH KOREA JUNE BANK LENDING TO HOUSEHOLD TOTAL KRW1161.5trln; PRIOR KRW1155.3trln

MARKETS

US TSYS: Asia Wrap - Yields Edge Higher

The TYU5 range has been 110-24+ to 110-28 during the Asia-Pacific session. It last changed hands at 111-25, up unchanged from the previous close.

- The US 2-year yield has edged higher trading around 3.90%, up 0.01 from its close.

- The US 10-year yield has edged higher trading around 4.413%, up 0.01 from its close.

- The 10-year yield saw a strong bounce in reaction to the better NFP print. This 4.40% area offers those who would like to express a long the opportunity to fade. A sustained close back above the 4.45/50% area though would not be great for the bulls and could see more of the longs pared back.

- MNI FED: FOMC Minutes: Analysts Eye Discussion Of July Cut, Tariff Inflation. The minutes of the June 17-18 FOMC meeting (released Wednesday Jul 9 at 2pm ET) should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end.

- "Two Kevins Battle to Be Next Fed Chair in Trump's 'Apprentice'-Style Contest -- WSJ". "Two Republicans named Kevin are vying to be the next chairman of the Federal Reserve. One is rising to the top of the list of potential candidates, while the other is facing skepticism from President Trump's allies." - BBG

- Data/Events: Bond investors will be focusing on the Fed Minutes tonight and the demand for 10 & 30-year maturities this week.

JGBS: Futures Weaker, BOJ Koeda: Up Revision To CPI View, 20Y Supply Tomorrow

JGB futures are weaker, -17 compared to the settlement levels.

- (Bloomberg) - "Junko Koeda, one of the BOJ's newest board members, signaled a possible upward revision to the central bank's inflation view this month. Such a move would keep open the possibility of another rate hike this year."

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's modest sell-off.

- The minutes of the June 17-18 FOMC meeting (released today) should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end.

- The cash JGB curve has twist-flattened, with yields 1bp higher to 1bp lower, pivoting at the 10-year.

- (Bloomberg) There's little sign that longer-dated JGBs will rebound given concerns that the July 20 upper house election will lead to a surge in government spending. That's also spurring traders to pare back beta on BOJ rate hikes, as the rapid steepening of the yield curve acts to tighten monetary conditions.

- Swap rates 1bp higher to 1bp lower. Swap spreads are mostly tighter.

- Tomorrow, the local calendar will see PPI, Weekly International Investment Flow and Tokyo Avg Office Vacancies data alongside 20-year supply.

AUSSIE BONDS: Post-RBA Sell-Off Extends

ACGBs (YM -7.0 & XM -9.5) are weaker and near session cheaps as the fall-out from yesterday's surprising RBA decision continued.

- (Bloomberg) Former RBA Assistant Governor Luci Ellis said episodes of the RBA surprising market pricing "will be more common" due to fewer inter-meeting speeches and a reliance on post-decision briefings.

- (AFR, Stephen Miller) “Certainly, the July decision was “cautious” even if the bond market might not have found it “predictable”. However, there is an argument that the certainty with which the bond market regarded a policy rate reduction in July was a reflection of an unbalanced assessment of the evidence. Certainly, the labour market looks to be in robust good health.”

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's modest sell-off.

- Cash ACGBs are 7-9bps with the AU-US 10-year yield differential at -6bps.

- The bills strip are 3-7bps cheaper and steeper.

- RBA-dated OIS pricing is modestly firmer across meetings today after shunting higher yesterday. Currently, pricing across meetings is 10-20bps firmer than yesterday's pre-RBA levels. A cumulative 60bps of easing is priced by year-end versus 75bps before the RBA decision.

- Tomorrow, the local calendar will be empty.

- The AOFM plans to sell A$1000mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Closed With A Bear-Steepener After RBNZ’s On-Hold Decision

NZGBs closed 1-5bps cheaper, with a steeper curve, after the RBNZ left the cash rate unchanged at 3.25%. The decision was widely expected, with only 4bps of easing priced by the market.

- (RBNZ) "Annual consumers price inflation will likely increase towards the top of the Monetary Policy Committee's 1 to 3 percent target band over mid-2025. However, with spare productive capacity in the economy and declining domestic inflation pressures, headline inflation is expected to remain in the band and return to around 2 percent by early 2026."

- The RBNZ considered two options at this meeting: to cut by 25bps or hold policy steady. The case to ease largely reflected concerns around faltering economic momentum. The case to hold won out, amid high uncertainty: The RBNZ noted: "Some members emphasised that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve."

- Swap rates are 2-6bps higher on the day, flat to 4bps higher after the decision.

- RBNZ dated OIS pricing closed showing a cumulative 33bps of easing by November 2025.

- Tomorrow, the local calendar will see Net Migration data alongside the NZ Treasury's planned sale of NZ$250mn of the 3.00% Apr-29 bond and NZ$200mn of the 4.50% May-35 bond.

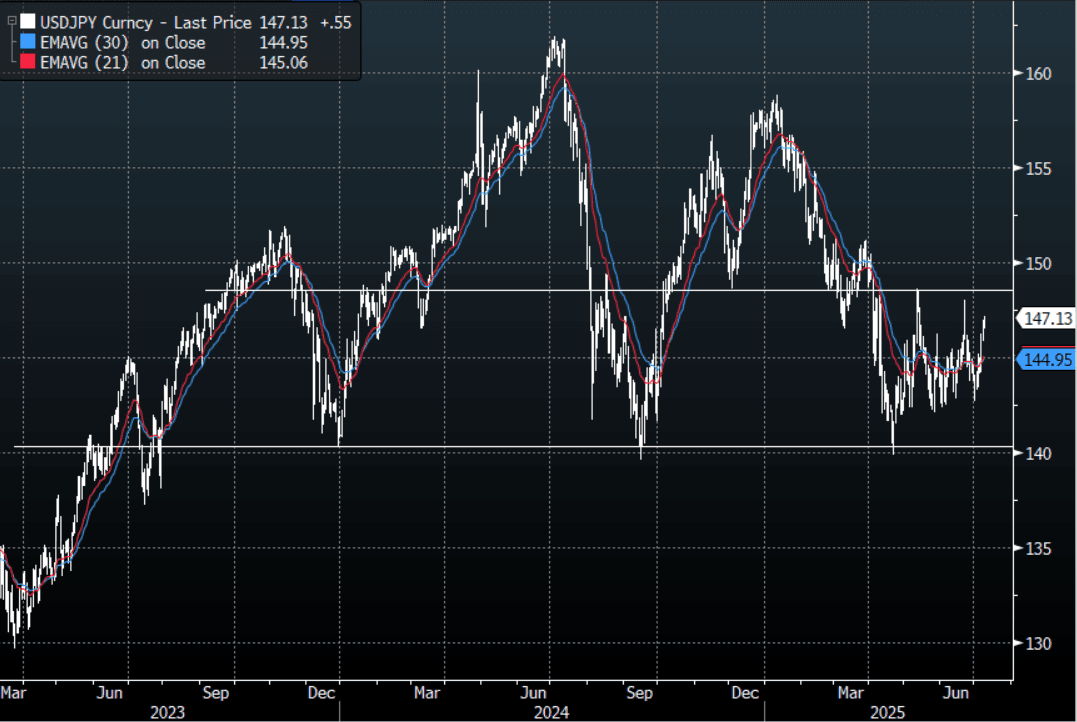

JPY: Asia Wrap - USD/JPY Continues To Challenge JPY Longs

The Asia-Pac USD/JPY range has been 146.53 - 147.18, Asia is currently trading around 147.10, +0.35% having found decent demand and staying better bid throughout our session. USD/JPY price action is telling as it marches relentlessly higher, challenging a market positioned the wrong way. Price is now pushing towards the upper boundary of its 142.00 - 148.00 range, the pair will probably continue to take its cue from the US rates market which is also approaching some key pivot areas.

- (Bloomberg) - As the dollar recovers from an extended slump, its Japanese counterpart is falling out of favor among traders. One-week dollar-yen risk reversals -- which gauge the premium traders are willing to pay for call versus put options -- now trade at some 37 basis points in favor of Japan’s currency. That’s the least bullish level since October, and reflects growing jitters over Japan’s spending outlook ahead of the key upper house election later this month.”

- (Bloomberg) - “Junko Koeda, one of the BOJ’s newest board members, signaled a possible upward revision to the central bank’s inflation view this month. Such a move would keep open the possibility of another rate hike this year.”

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to continue to correct higher the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.50($860m).Upcoming Close Strikes : none.

- CFTC data shows Asset managers increased their JPY longs slightly +94753, while leveraged funds maintained their longs they have tried to rebuild +15798.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: Asia FX Wrap - The USD Edges Higher

The BBDXY has had a range of 1196.17 - 1198.60 in the Asia-Pac session, it is currently trading around 1197. The USD has edged higher back towards the overnight highs in a quiet Asia-Pac session, +0.15%. CHINA CPI and PPI Weak Trend Continues: The decline in PPI entered its 33th month as June PPI declined -3.6%. This was the lowest print since July 2023. Manufactured goods prices declined further along with food and mining products. CPI in June inched up by +0.1% YoY as Core CPI rose +0.7% YoY. “With positioning so one-sided, Brent Donnelly says that even a modest pause in foreign hedging or a string of good US headlines could unleash a classic squeeze, dragging EURUSD back toward the 1.14–1.15 “pain zone” and lifting the DXY to its 50- and 100-day moving averages.” - BBG. "DONALD TRUMP DEAL TO LEAVE EU FACING HIGHER TARIFFS THAN UK- FT

- EUR/USD - Asian range 1.1702 - 1.1729, Asia is currently trading 1.1710. The pair failed to hold onto the gains it made on news of a proposed deal with the US, demand seen again just below the 1.1700 area. The price is starting to look a little stretched in the short term and is vulnerable to any correction in the USD, first support is back towards 1.1600 then more importantly the 1.1450 area.

- GBP/USD - Asian range 1.3565 - 1.3595, Asia is currently dealing around 1.3585. Strong demand was again seen on a 1.3500 handle. Price has rejected the move higher and with the USD looking constructive the risk for GBP/USD points to further downside in the short-term. First support around 1.3500 and then more importantly the 1.3350/1.3400 area.

- USD/CNH - Asian range 7.1794 - 7.1866, the USD/CNY fix printed 7.1541, Asia is currently dealing around 7.1850. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.06%, Gold $3295, US 10-Year 4.41%, BBDXY 1197, Crude oil $68.17

Data/Events : Germany CPI, Italy Industrial Production

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

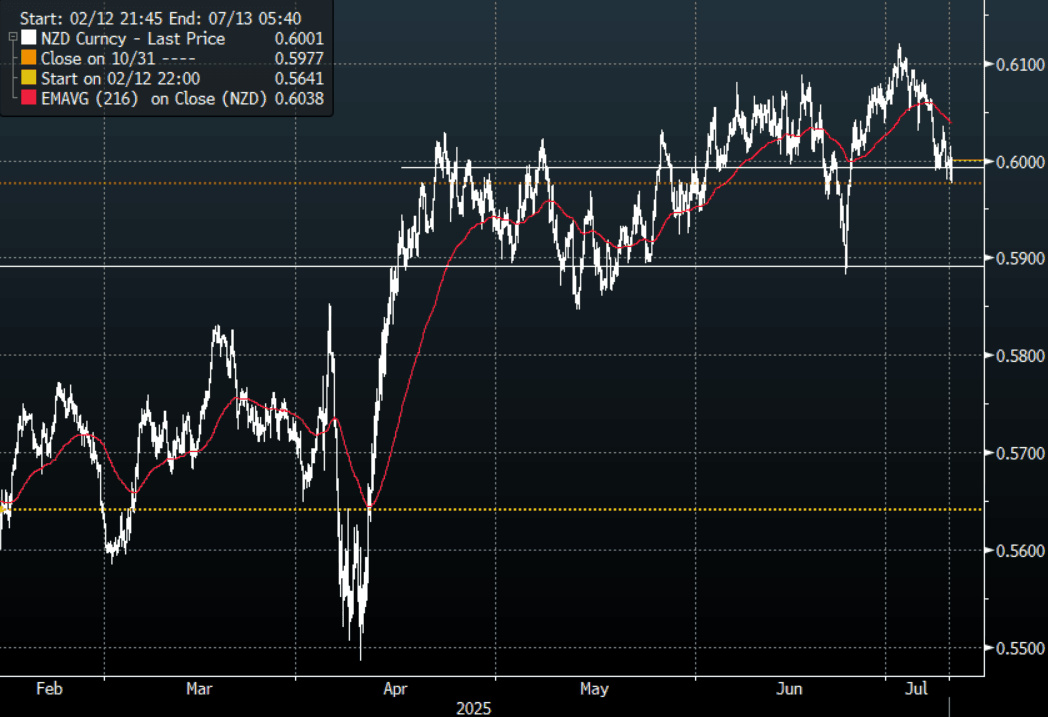

NZD: Asia Wrap - NZD/USD Tests Below 0.6000 Finds Bids As RBNZ Considered A Cut

The NZD/USD had a range of 0.5976 - 0.6014 in the Asia-Pac session, going into the London open trading around 0.6000, +0.03%. The pair was muted after the RBNZ left the benchmark rate unchanged, it initially tested higher but when the RBNZ said it had considered a cut the NZD dropped quickly in response. If there is a deeper correction in risk and the USD can squeeze higher then the risk to the NZD is a move back towards the 0.5850/0.5900 area, the bulls will be hoping the support just below 0.6000 continues to hold.

- RBNZ On Hold, Considered Cutting Rates By 25bps, Awaiting More Information : As widely expected, the RBNZ held the policy rate steady at 3.25%. This was in line with the sell-side consensus (although some forecasters saw risks of a 25bps cut), while market pricing only gave a very small chance to a cut today.

- The RBNZ considered two options at this meeting, to cut by 25bps or hold policy steady. The case to ease largely reflected concerns around faltering economic momentum. The case to hold won out, amid high uncertainty: The RBNZ noted: "Some members emphasized that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6075(NZD519m). Upcoming Close Strikes : 0.6000(NZD407m July 10), 0.6025(NZD373m July10).

- CFTC Data shows Asset Managers have reduced their newly built longs in NZD +8515, the Leveraged community reduced their short last week -8424.

- AUD/NZD range for the session has been 1.0868 - 1.0900, currently trading 1.0895. The cross has broken out of its recent range and focus will now turn to the more pivotal 1.0900/50 area.

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

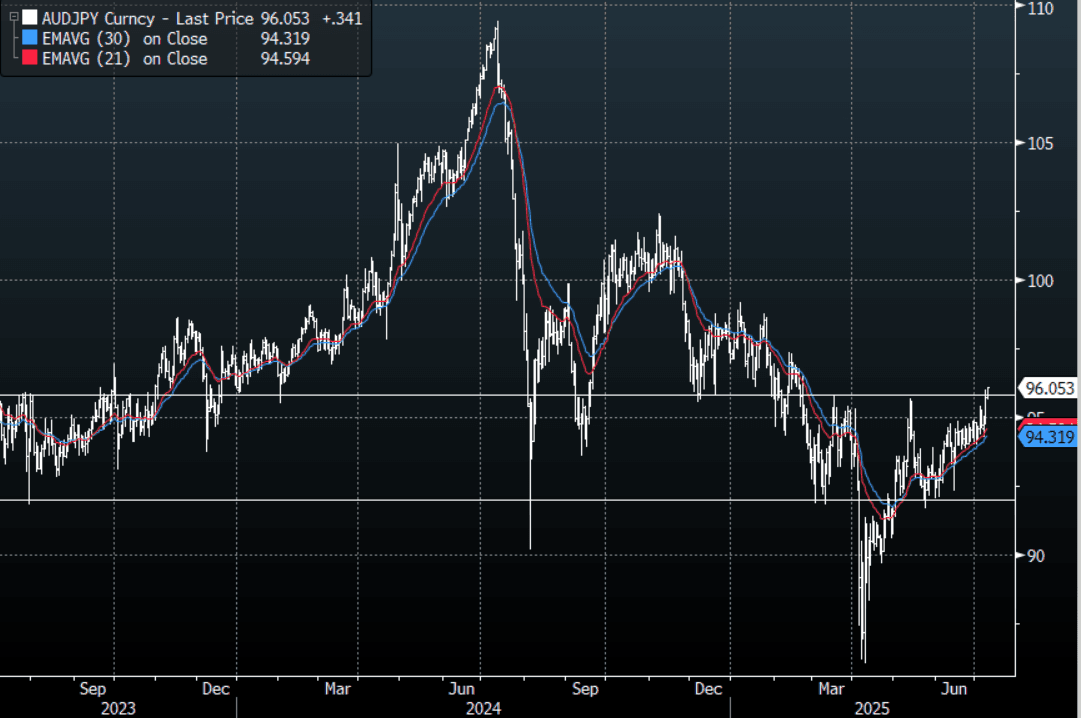

AUD: Asia Wrap - AUD/USD Trades Sideways Above 0.6500, AUD/JPY Breaking ?

The AUD/USD has had a range of 0.6510 - 0.6537 in the Asia- Pac session, it is currently trading around 0.6530, -0.03%. The pair has traded sideways in a tight range today as it consolidates the reaction to the RBA yesterday. The AUD needs to hold above its 0.6480/0.6500 support as a sustained move below there would see a deeper correction back to 0.6350/0.6400.

- MNI RBA Review - July 2025: Easing Bias Still Intact: The RBA surprised the market by keeping rates on hold at 3.85%. The central bank wants to see more evidence of inflation sustainably trending towards the 2-3% target before easing more.

- RBA Governor Bullock stated the central bank still has an easing bias, and the split vote decision (6 in favor of the hold, 3 in favor or a cut) reflected the timing of further easing rather than the direction of rates.

- AUSSIE BONDS ACGB Dec-35 Supply Digested But Less Demand: Expectations of sustained strong pricing at auctions proved accurate, with the latest round of ACGB Dec-35 supply seeing the weighted average yield print 0.58bp through prevailing mids (per Yieldbroker). Today's cover ratio fell to 2.6500x from 3.1042x.

- The AUD/USD bounced strongly off its support around 0.6500 overnight, looks like it's back to the 0.6500 - 0.6600 range and it should now take its cues from the USD. Watching to see if the support continues to hold as a move through there signals a deeper correction.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6425(AUD700m), 0.6550(AUD 607m). Upcoming Close Strikes : 0.6650(AUD857m July 10), 0.6600(AUD634m July 10), 0.6650(AUD599m July 11)

- CFTC Data shows Asset managers pared back their shorts slightly -35992, the Leveraged community maintained their shorts -22903..

- AUD/JPY - Today's range 95.62 - 96.05, it is trading currently around 96.04, +0.34%. The pair is attempting to break above 96.00, with the market positioned both short AUD and long JPY. A sustained break above this level could see another tranche of these shorts pared back and provide a tailwind to probe higher.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China's Bourses Reach YTD Highs

The rally today for China's mainland bourses saw the CSI 300 hit new highs for 2025. The release of weaker than expected PPI and ongoing weak CPI has seen investors speculating as to the possibility of further stimulatory measures to come from the government. As the July Politburo meeting approaches investors are thinking that this could be a meeting where further measures are enacted to support growth in the second half of the year.

- The Hang Seng was the long decliner of the China bourses, down -0.74% today whilst the CSI 300 gained +0.32%. The Shanghai Comp and the Shenzhen Comp rose by +0.30%.

- The KOSPI continues its good run, rising today by +0.58%.

- The FTSE Malay KLCI fell -0.18% whilst the Jakarta Composite rallied +0.40%.

- In Singapore the FTSE Straits Times was up +0.15% and the PSEi in the Philippines up +0.87%.

- The NIFTY 50 is doing very little today flat at the open having gained by +0.24%

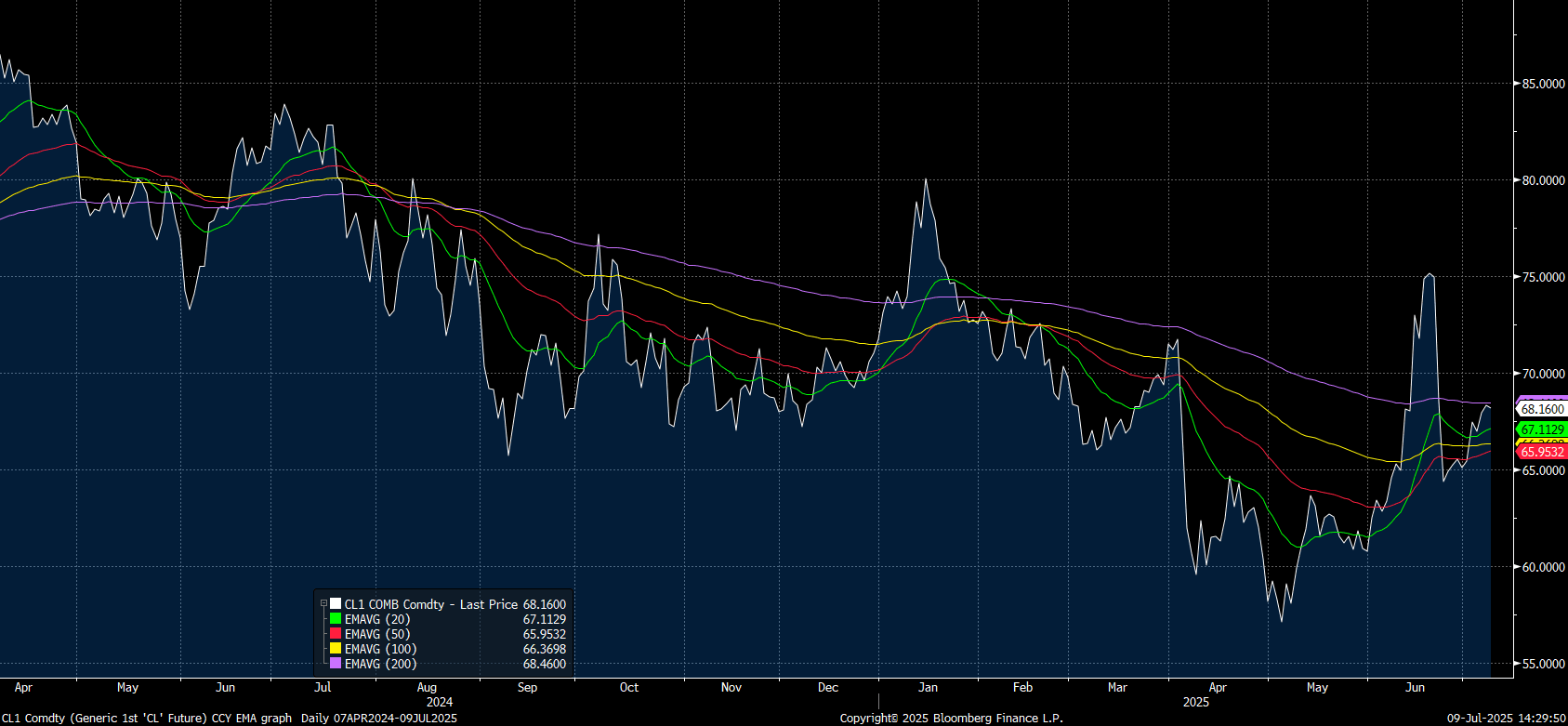

Oil Posts Modest Gains on Easing Trade Tensions

- Oil does not appear to have a firm trend in place with the weakness experienced seemingly done for now.

- Short-term fundamentals remain firm, with product tightness (given low oil inventories from the US and the potential for re-stocking) supporting crude demand. Whilst geopolitical headlines in the Middle East create some concerns about potential ongoing Houthi attacks in the Red Sea are creating modest caution.

- WTI moderated during the Asia trading day by -0.11% to US$68.22 bbl.

- The move leaves WTI just below the 200-day EMA of $68.46 which for now appears to be a reasonable resistance leve.

Source: Bloomberg Finance LP / MNI

- Brent has done very little today, hovering around US$70bbl to remain between the 200-day EMA of $71.57 and the 100-day EMA of $69.26

- A report out from the American Petroleum Institute shows that US stockpiles are on the rise from historic lows. Last week inventories rose by 7m barrels, the largest increase since January.

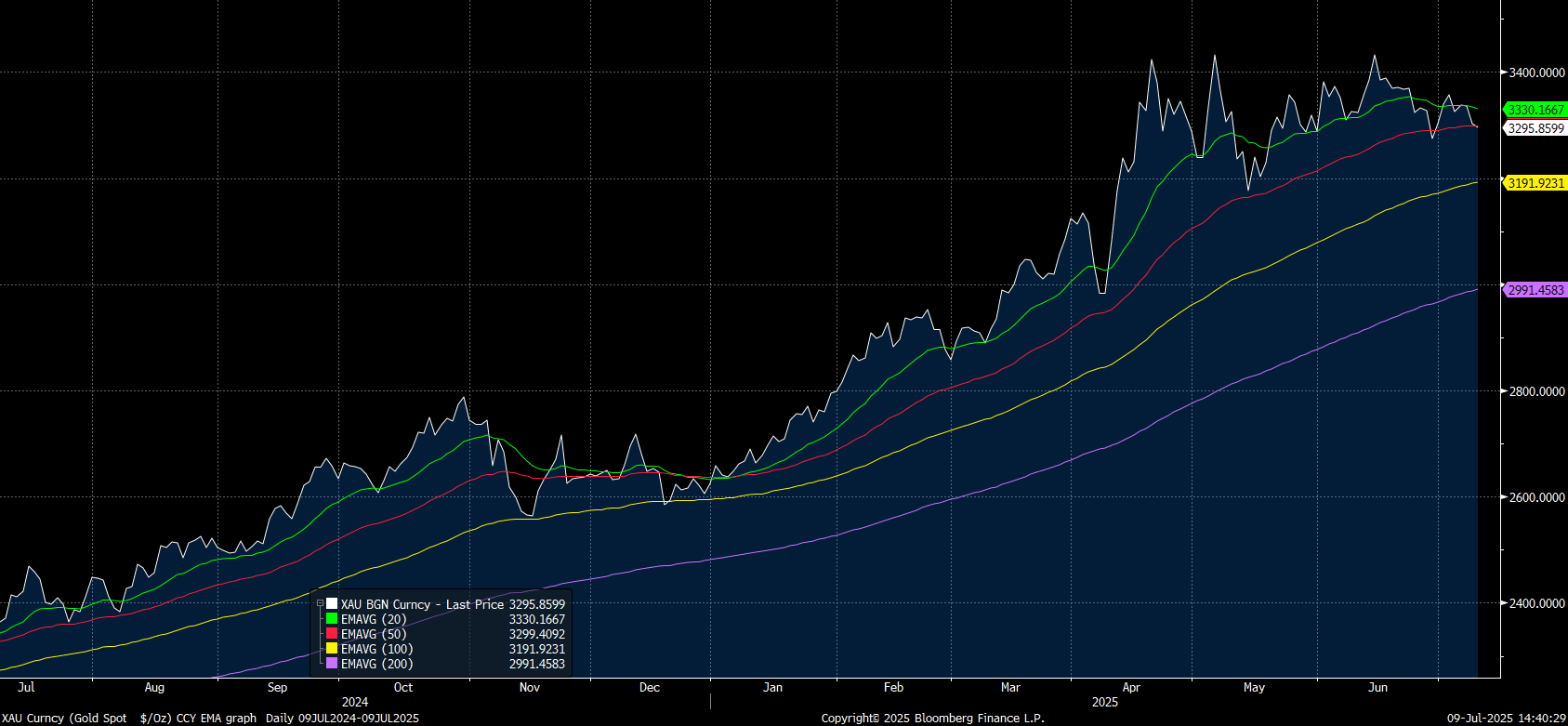

Gold Steadies, Looking for Next Catalyst

- After strong falls overnight, Gold has steadied in the Asia trading day modestly lower.

- Gold opened the day at US$3,302.51 and is down -0.20% at $3,295.36.

- Last night's falls saw gold trend below major moving averages and today's weakness sees gold below the 50-day EMA of $3,299.39.

source: Bloomberg Finance LP / MNI

- Below is the 100-day EMA of $3,191.92.

- Brazil's exchange B3 SA is launching a new gold futures contract that will begin trading on July 21 amid a more than 25% year-to-date increase in the commodity that led it to a record high on April.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 09/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/07/2025 | 0930/1030 | BOE Financial Stability Report | ||

| 09/07/2025 | 1000/1100 | BOE FSR Press Conference | ||

| 09/07/2025 | 1045/1245 | ECB Lane At House of the Euro | ||

| 09/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/07/2025 | 1100/1300 | EC De Guindos Closing Remarks At Conference | ||

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/07/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/07/2025 | 1800/1400 | *** | FOMC Minutes | |

| 10/07/2025 | 0600/0800 | *** | CPI Norway | |

| 10/07/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/07/2025 | 0600/0800 | *** | HICP (f) | |

| 10/07/2025 | 0700/0900 | ECB Cipollone Digital Euro Lecture | ||

| 10/07/2025 | 0800/1000 | * | Industrial Production | |

| 10/07/2025 | - | *** | Money Supply | |

| 10/07/2025 | - | *** | New Loans | |

| 10/07/2025 | - | *** | Social Financing | |

| 10/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export |