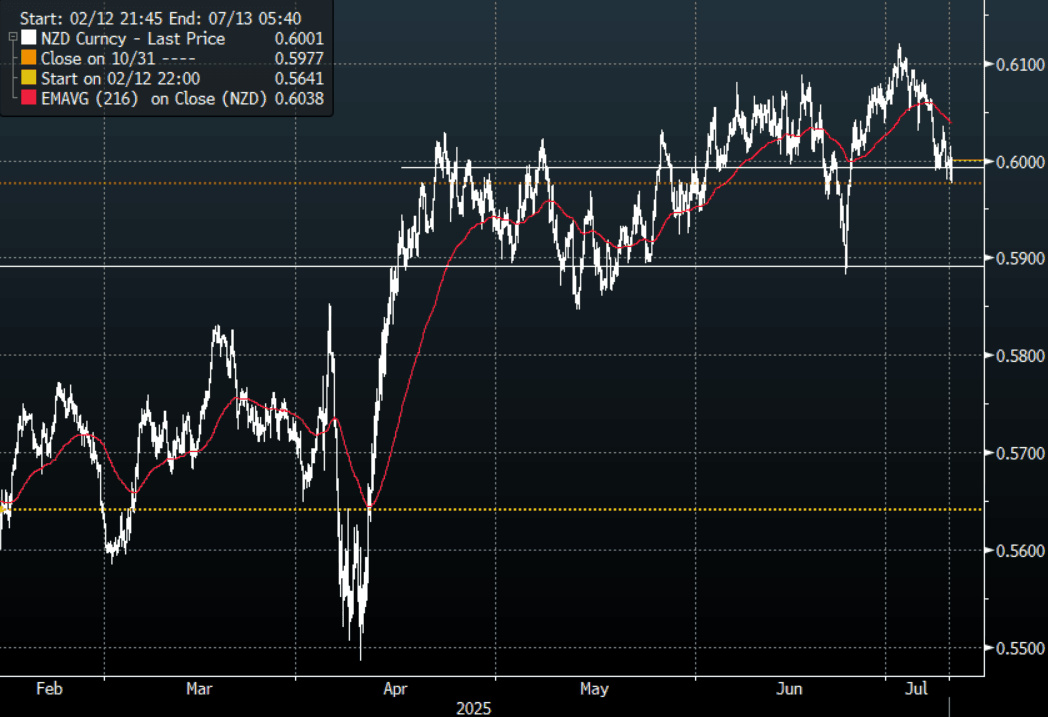

NZD: Asia Wrap - NZD/USD Tests Below 0.6000 Finds Bids As RBNZ Considered A Cut

The NZD/USD had a range of 0.5976 - 0.6014 in the Asia-Pac session, going into the London open trading around 0.6000, +0.03%. The pair was muted after the RBNZ left the benchmark rate unchanged, it initially tested higher but when the RBNZ said it had considered a cut the NZD dropped quickly in response. If there is a deeper correction in risk and the USD can squeeze higher then the risk to the NZD is a move back towards the 0.5850/0.5900 area, the bulls will be hoping the support just below 0.6000 continues to hold.

- RBNZ On Hold, Considered Cutting Rates By 25bps, Awaiting More Information : As widely expected, the RBNZ held the policy rate steady at 3.25%. This was in line with the sell-side consensus (although some forecasters saw risks of a 25bps cut), while market pricing only gave a very small chance to a cut today.

- The RBNZ considered two options at this meeting, to cut by 25bps or hold policy steady. The case to ease largely reflected concerns around faltering economic momentum. The case to hold won out, amid high uncertainty: The RBNZ noted: "Some members emphasized that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6075(NZD519m). Upcoming Close Strikes : 0.6000(NZD407m July 10), 0.6025(NZD373m July10).

- CFTC Data shows Asset Managers have reduced their newly built longs in NZD +8515, the Leveraged community reduced their short last week -8424.

- AUD/NZD range for the session has been 1.0868 - 1.0900, currently trading 1.0895. The cross has broken out of its recent range and focus will now turn to the more pivotal 1.0900/50 area.

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Little Changed Today, Significant Risks Persist Though

Gold prices are currently slightly higher during today’s APAC session and off the intraday low of $3293.64/oz. They are up to $3311.4, just below support at $3313.2, 20-day EMA. Better risk appetite is pressuring gold, while the softer US dollar (USD BBDXY -0.2%) and lower US yields are supporting it.

- Bullion will be monitoring progress closely when the US and China meet later today in London to discuss trade. Any sign that the two sides are unlikely to agree would likely increase safe-haven flows into the yellow metal.

- Data showing that the US jobs market was resilient in May to the increased trade tensions weighed on gold prices on Friday.

- US fiscal developments are also important. Thus, Thursday’s US Treasury bond auction and news on the likelihood of President Trump’s tax cut bill passing the senate will be watched closely. Increased fiscal risks have also driven safe haven flows.

- Silver has range traded and is currently up 0.2% to $36.05. It has moved between $35.92 and $36.09, also between initial support and resistance.

- Equities are stronger with the Nikkei up 1.0% and Hang Seng +1.0% but S&P e-mini down 0.2%. Oil prices are slightly lower with WTI -0.1% to $64.52/bbl. Copper is flat and iron ore is back below $95/t.

- Later US April wholesale data and May NY Fed 1-yr inflation expectations print. The ECB’s Elderson speaks. The focus will be on Wednesday’s May US CPI and Friday’s Uni of Michigan June survey.

JGBS: Futures Edge Up, Cash JGB Yields Firm, Back End Leads

JGB futures sit slightly above end Friday Friday levels from last week. The June future last 139.20, -.15 versus settlement levels. Outside of a modest rise at the start of the session, we have traded fairly tight ranges so far in Monday trade. A modest rebound in US Tsy 10yr futures has likely seen some positive spill over.

- The local data calendar saw positive Q1 GDP revisions, but these didn't impact JGB sentiment. Consumption was revised slightly higher, while inventories contributed more to growth than the initial estimate. Business spending remained positive but was revised down. Overall q/q growth was flat (from an initial estimate of -0.2%).

- For cash JGB yields, the bias is higher, but we sit away from best levels for the 10yr. We were last near 1.48% (session highs rest at 1.491%). It has been a similar backdrop across other parts of the curve. The 30yr has seen some slight outperformance in yield terms, up close to 4bps, last around 2.92%.

- Focus remains on how government issuance may chance, and/or BOJ bond buying shifts as well. We haven't seen any fresh developments on this front today though.

- PM Ishiba has been on the news wires stating that public and financial market trust in Japan's finances must be maintained (via RTRS).

THAILAND: VIEW: JP Morgan Sees 2025 CPI Below BoT Target Driving 75bp More Cuts

May Thai inflation was stronger than expected with headline down 0.6% y/y but still a deterioration from April’s -0.2% y/y, while core rose 1.1% y/y up from 1.0% due to prepared food and housing. JP Morgan expects deflation to continue in Thailand through Q3 2025 resulting in only 0.2% inflation in 2025 below the Bank of Thailand’s 1-3% target corridor. Thus it continues to “pencil in three more 25bp rate cuts” in June, August and October bringing the terminal rate to 1.0%.

- JP Morgan notes that “on a sequential basis, headline and core CPI rose 0.3%m/m, sa and 0.2%m/m, sa respectively, while the underlying trend continued to downshift.”

- “The stronger-than-expected print was largely driven by higher core (0.3%pt. contribution to the monthly increase of 0.26%m/m, sa;) and energy prices (0.03%pt.) with a partial offset from raw food prices (-0.07%pt.). Within core CPI, prepared food (0.14%pt.) and housing (0.08%pt.) prices posted sharp gains.”

- “The outsized increase in prepared food prices last month (0.14%pt. vs. 2018-24 average: 0.03%pt.) was driven primarily by the fast food/delivery sub-component. We are inclined to think that it reflects ad-hoc/seasonal re-pricing by service providers at this point, given the lack of input cost pressures (e.g., labor, fuel, raw food).”

- “Indeed, supply-demand dynamics in the agricultural sector have improved significantly this year, leading to downward pressures on both wholesale and retail raw food prices.”

- “Stripping out prepared food, our so-called core-core CPI gauge fell into deflation territory and continues to show weak demand-pull price pressures.”

- “The outlook for energy CPI remains benign on low and stable global crude oil prices.”