CNH: USD/CNH - Trades Heavy, Targeting 6.97-7.00

The overnight range was 7.0654 - 7.0703, Asia is currently trading around 7.0660. The pair continues to trade heavy with bounces very shallow. The market is building momentum lower after breaking below the support around 7.0800, the target looks to be towards the 6.97-7.00 area. The pair has found some demand around the 7.0650 the last couple of days it will have to work through this support to extend lower again. On the day look for sellers to reemerge towards 7.0800-7.0900 as the market looks to build momentum lower.

- Jack Farley interviewed Michael Pettis about the Chinese economy, where he emphasised that China has one of the lowest consumption rates in the world. Therefore the growth in production and manufacturing has to lead to trade surpluses.” https://x.com/JackFarley96/status/1995959667248562445?s=20

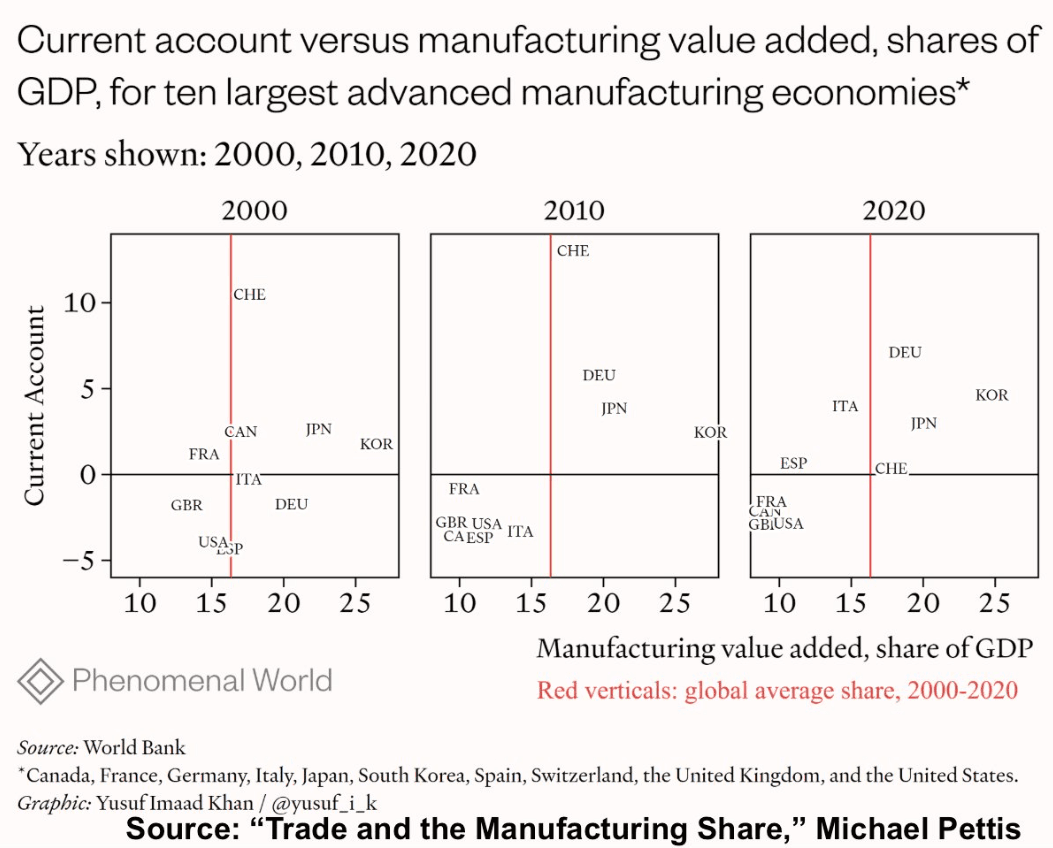

- Michael Pettis Writes, "As the graph shows, advanced economies with current account surpluses mostly have manufacturing shares of GDP that are above the global average, and advanced economies with current account deficits mostly have manufacturing shares of GDP that are below the global average." https://www.phenomenalworld.org/analysis/trade-and-the-manufacturing-share/ See Graph Below

- The USD/CNH Average True Range for the last 10 Trading days: 113 Points

- Data/Event : RatingDog China PMI Services/Composite

Fig 1 : Current account Vs Manufacturing Value Added To GDP

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Cautious On Uncertain Fed Outlook & Changed US-China Trade Relations

Gold prices were moderately lower on Friday but finished above $4000/oz. They fell to a low of $3972.71 but finished at $4002.92 to be down 0.5% on the day, as the US dollar strengthened (BBDXY +0.2%), and 2.7% on the week. Bullion returned to trade above $4000 following the meeting between presidents Trump and Xi on Thursday. While Trump sounded very positive, the one-year pause created scepticism that trade relations will return to where they were, which has supported gold prices.

- Gold approached the 50-day EMA at $3853.2 on Friday after breaking through support at $3886.6. If it clears the 50-day EMA, then the short-term bear theme would be strengthened.

- China has removed its retail gold tax break which is likely to reduce demand.

- Bloomberg observes that there were outflows from gold ETFs for six straight days until Thursday. Westpac believes that this is contributing to gold’s correction and that prices could fall to around $3750.

- Hawkish comments from Fed Chair Powell that a rate cut in December is not a given also pressured non-yield bearing bullion. The OIS market now has around 17bp priced in for the 10 December decision and it was close to 25bp before the 29 October meeting.

- Silver was down 0.5% to $48.689 on Friday to be flat on the week and up 4.4% in October. It reached a high of $49.370 early in the European session and then sold off to $48.384, holding above the 50-day EMA at $45.852.

- Equities were mixed with the S&P up 0.3% but Euro stoxx down 0.7%. Oil prices were slightly higher with Brent +0.5% to $64.58/bbl. Copper rose 0.2%.

US TSYS: Bond Yields Still Lower for October, Despite Last Week's Moves

Bond futures finished lower last week with TYZ5 ending at 112-21+, down from 113-13 the week prior. There is no trading today as Japan is closed. TYZ5 sits atop the 50-day EMA of 115-15 which it hasn't trade below since mid-August.

To an extent, the move higher in yields last week may have overlooked a broadly positive week for bonds, with yields in key maturities all finishing 5-8bps lower.

- The US 2-Yr finished October at 3.57%, -5bps for the month

- The US 5-Yr finished at 3.689%, -5bps for the month.

- The US 10-Yr finished at 4.07%, -8bps for the month.

- The US 30-Yr finished at 4.65%, -5bps for the month.

With data releases in the US still uncertain, the bond market continues to focus on issuance. Issuance tonight will not be market moving with 13 and 26 week bill issuance the key auctions.

BONDS: NZGBS: Little Changed, Wed's Q3 Labour Mkt Data In Focus

In local morning trade, NZGBs are unchanged after US tsys finished Friday with modest gains across the curve (flat to 3bps richer).

- US equities ended the month on a positive note. Earnings season remains in focus for investors. The vast majority of the 60% of S&P firms that have reported results so far have exceeded analyst estimates, according to Bloomberg.

- Kansas Federal Reserve President Schmid said he voted against the decision to reduce rates by 25bp last week due to concerns about inflation.

- NZ home-building approvals rose 7.2% m/m in September versus revised +6.1% in August.

- The key event in NZ this week is the Q3 labour market and wages data released on Wednesday. Filled jobs for the quarter signal a stabilization, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ’s August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for November, with a cumulative 30bps by February 2026.