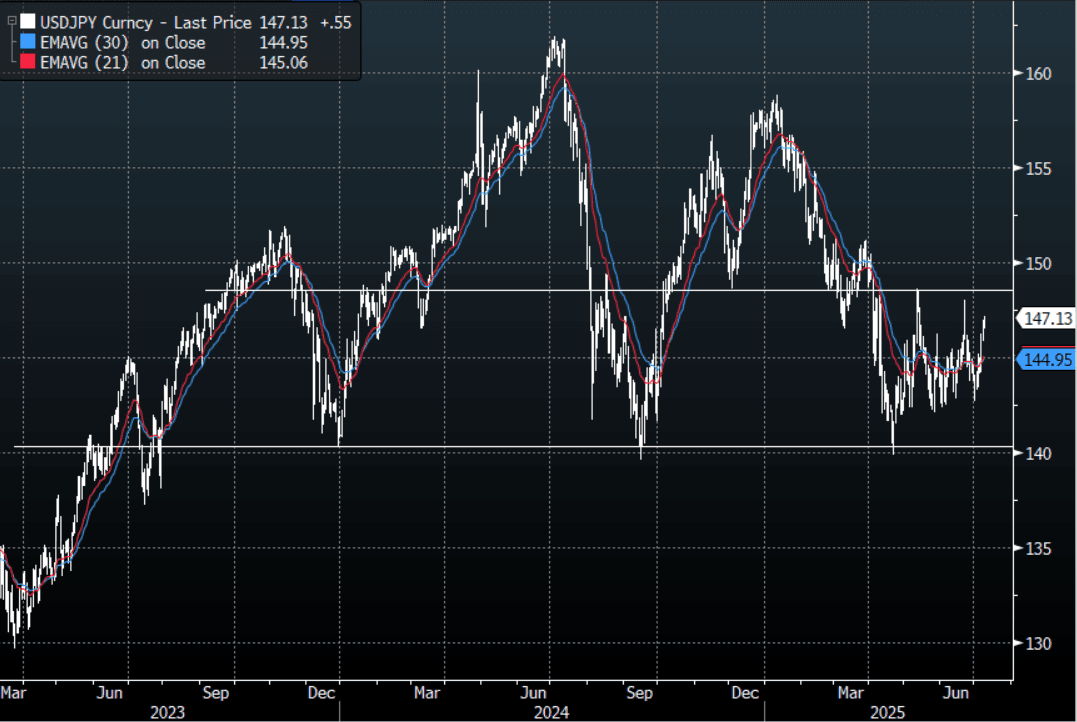

JPY: Asia Wrap - USD/JPY Continues To Challenge JPY Longs

The Asia-Pac USD/JPY range has been 146.53 - 147.18, Asia is currently trading around 147.10, +0.35% having found decent demand and staying better bid throughout our session. USD/JPY price action is telling as it marches relentlessly higher, challenging a market positioned the wrong way. Price is now pushing towards the upper boundary of its 142.00 - 148.00 range, the pair will probably continue to take its cue from the US rates market which is also approaching some key pivot areas.

- (Bloomberg) - As the dollar recovers from an extended slump, its Japanese counterpart is falling out of favor among traders. One-week dollar-yen risk reversals -- which gauge the premium traders are willing to pay for call versus put options -- now trade at some 37 basis points in favor of Japan’s currency. That’s the least bullish level since October, and reflects growing jitters over Japan’s spending outlook ahead of the key upper house election later this month.”

- (Bloomberg) - “Junko Koeda, one of the BOJ’s newest board members, signaled a possible upward revision to the central bank’s inflation view this month. Such a move would keep open the possibility of another rate hike this year.”

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to continue to correct higher the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.50($860m).Upcoming Close Strikes : none.

- CFTC data shows Asset managers increased their JPY longs slightly +94753, while leveraged funds maintained their longs they have tried to rebuild +15798.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

THAILAND: VIEW: JP Morgan Sees 2025 CPI Below BoT Target Driving 75bp More Cuts

May Thai inflation was stronger than expected with headline down 0.6% y/y but still a deterioration from April’s -0.2% y/y, while core rose 1.1% y/y up from 1.0% due to prepared food and housing. JP Morgan expects deflation to continue in Thailand through Q3 2025 resulting in only 0.2% inflation in 2025 below the Bank of Thailand’s 1-3% target corridor. Thus it continues to “pencil in three more 25bp rate cuts” in June, August and October bringing the terminal rate to 1.0%.

- JP Morgan notes that “on a sequential basis, headline and core CPI rose 0.3%m/m, sa and 0.2%m/m, sa respectively, while the underlying trend continued to downshift.”

- “The stronger-than-expected print was largely driven by higher core (0.3%pt. contribution to the monthly increase of 0.26%m/m, sa;) and energy prices (0.03%pt.) with a partial offset from raw food prices (-0.07%pt.). Within core CPI, prepared food (0.14%pt.) and housing (0.08%pt.) prices posted sharp gains.”

- “The outsized increase in prepared food prices last month (0.14%pt. vs. 2018-24 average: 0.03%pt.) was driven primarily by the fast food/delivery sub-component. We are inclined to think that it reflects ad-hoc/seasonal re-pricing by service providers at this point, given the lack of input cost pressures (e.g., labor, fuel, raw food).”

- “Indeed, supply-demand dynamics in the agricultural sector have improved significantly this year, leading to downward pressures on both wholesale and retail raw food prices.”

- “Stripping out prepared food, our so-called core-core CPI gauge fell into deflation territory and continues to show weak demand-pull price pressures.”

- “The outlook for energy CPI remains benign on low and stable global crude oil prices.”

ASIA STOCKS: Major Asia Pac Markets Firmer, Kospi Continues To Outperform

Asian equity markets are mostly trading with a positive footing in the first part of Monday trade. The Nikkei 225 is up around 1%, likewise for the Hang Seng in Hong Kong. The Kospi continues to be an outperformer, up over 1.6%.

- We had a positive lead from US markets on Friday, the SPX up a little over 1%. US data beats, particularly on the wages may have helped. Also, today in London we have US-China trade talks resuming. Positive themes around exports of rare earths resuming to the US and the EU is another positive ahead of these talks.

- Fallout from protests in major US cities (with Trump calling in the National Guard for Los Angeles) is not impacting US equity sentiment greatly at this stage.

- Still, China's CSI 300 is up only modestly, last +0.18% at the lunchtime break, putting the index near 3881. Earlier China data showed CPI remain in deflation, while PPI deflation worsened further. This underscores on-going policy support needs in 2025. On the trade front, export and imports where both below forecasts, with trade to the US continuing to fall.

- The HSI is up +1% at the break, with the tech sub index up +2.3% at this stage.

- The Kospi continues to outperform, up over 1.6%. This puts the index within striking distance of July 2024 highs around 2900. Offshore investors have bought $348mn of local shares today. Optimism around the domestic outlook continue to buoy sentiment.

- In South East Asia, gains are more modest, mostly under 0.50%. Australian and Indonesian markets are closed today.

US TSYS: Tsys Firmer, Led By Front End, 2yr Struggles Near 4.05% Again

The first part of Monday US Tsy trade has seen outperformance, led by the front end. For the 2-5yr tenor yields are off around 3bps. The 10yr Tsy yield is back under 4.49%.

- The 10yr Sep Tsy future has crept higher throughout the session, last at 110-02+, +05+, versus end Friday levels. A direct catalyst for the move haven't been obvious, although we have only given back a modest part of Friday's sell-off.

- For the 2yr Tsy yield, we have struggled once we approach the 4.05% region, going back to mid March. Despite Friday's data beats in the US, there still may be a sense of more downside risks to growth lie ahead, which in turn could be capping upside yield momentum.

- The 10yr, just under 4.49%, remains fairly close to the mid-point of recent ranges.

- Looking ahead, we have wholesale inventories tonight, then tomorrow NFIP small business sentiment and NY Fed inflation expectations. The main focus will be on Wednesday's CPI print though.