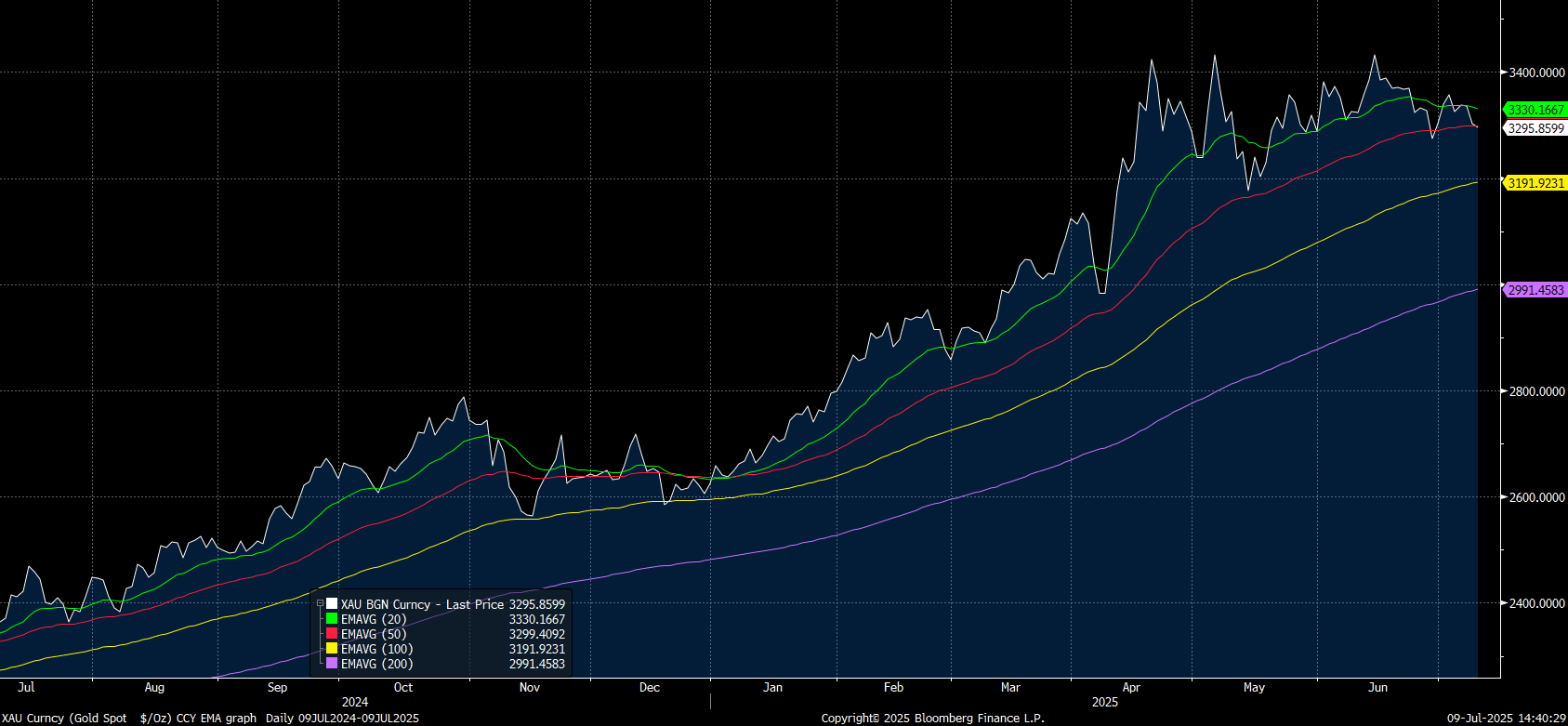

GOLD: Gold Steadies, Looking for Next Catalyst

- After strong falls overnight, Gold has steadied in the Asia trading day modestly lower.

- Gold opened the day at US$3,302.51 and is down -0.20% at $3,295.36.

- Last night's falls saw gold trend below major moving averages and today's weakness sees gold below the 50-day EMA of $3,299.39.

source: Bloomberg Finance LP / MNI

- Below is the 100-day EMA of $3,191.92.

- Brazil's exchange B3 SA is launching a new gold futures contract that will begin trading on July 21 amid a more than 25% year-to-date increase in the commodity that led it to a record high on April.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

THAILAND: VIEW: JP Morgan Sees 2025 CPI Below BoT Target Driving 75bp More Cuts

May Thai inflation was stronger than expected with headline down 0.6% y/y but still a deterioration from April’s -0.2% y/y, while core rose 1.1% y/y up from 1.0% due to prepared food and housing. JP Morgan expects deflation to continue in Thailand through Q3 2025 resulting in only 0.2% inflation in 2025 below the Bank of Thailand’s 1-3% target corridor. Thus it continues to “pencil in three more 25bp rate cuts” in June, August and October bringing the terminal rate to 1.0%.

- JP Morgan notes that “on a sequential basis, headline and core CPI rose 0.3%m/m, sa and 0.2%m/m, sa respectively, while the underlying trend continued to downshift.”

- “The stronger-than-expected print was largely driven by higher core (0.3%pt. contribution to the monthly increase of 0.26%m/m, sa;) and energy prices (0.03%pt.) with a partial offset from raw food prices (-0.07%pt.). Within core CPI, prepared food (0.14%pt.) and housing (0.08%pt.) prices posted sharp gains.”

- “The outsized increase in prepared food prices last month (0.14%pt. vs. 2018-24 average: 0.03%pt.) was driven primarily by the fast food/delivery sub-component. We are inclined to think that it reflects ad-hoc/seasonal re-pricing by service providers at this point, given the lack of input cost pressures (e.g., labor, fuel, raw food).”

- “Indeed, supply-demand dynamics in the agricultural sector have improved significantly this year, leading to downward pressures on both wholesale and retail raw food prices.”

- “Stripping out prepared food, our so-called core-core CPI gauge fell into deflation territory and continues to show weak demand-pull price pressures.”

- “The outlook for energy CPI remains benign on low and stable global crude oil prices.”

ASIA STOCKS: Major Asia Pac Markets Firmer, Kospi Continues To Outperform

Asian equity markets are mostly trading with a positive footing in the first part of Monday trade. The Nikkei 225 is up around 1%, likewise for the Hang Seng in Hong Kong. The Kospi continues to be an outperformer, up over 1.6%.

- We had a positive lead from US markets on Friday, the SPX up a little over 1%. US data beats, particularly on the wages may have helped. Also, today in London we have US-China trade talks resuming. Positive themes around exports of rare earths resuming to the US and the EU is another positive ahead of these talks.

- Fallout from protests in major US cities (with Trump calling in the National Guard for Los Angeles) is not impacting US equity sentiment greatly at this stage.

- Still, China's CSI 300 is up only modestly, last +0.18% at the lunchtime break, putting the index near 3881. Earlier China data showed CPI remain in deflation, while PPI deflation worsened further. This underscores on-going policy support needs in 2025. On the trade front, export and imports where both below forecasts, with trade to the US continuing to fall.

- The HSI is up +1% at the break, with the tech sub index up +2.3% at this stage.

- The Kospi continues to outperform, up over 1.6%. This puts the index within striking distance of July 2024 highs around 2900. Offshore investors have bought $348mn of local shares today. Optimism around the domestic outlook continue to buoy sentiment.

- In South East Asia, gains are more modest, mostly under 0.50%. Australian and Indonesian markets are closed today.

US TSYS: Tsys Firmer, Led By Front End, 2yr Struggles Near 4.05% Again

The first part of Monday US Tsy trade has seen outperformance, led by the front end. For the 2-5yr tenor yields are off around 3bps. The 10yr Tsy yield is back under 4.49%.

- The 10yr Sep Tsy future has crept higher throughout the session, last at 110-02+, +05+, versus end Friday levels. A direct catalyst for the move haven't been obvious, although we have only given back a modest part of Friday's sell-off.

- For the 2yr Tsy yield, we have struggled once we approach the 4.05% region, going back to mid March. Despite Friday's data beats in the US, there still may be a sense of more downside risks to growth lie ahead, which in turn could be capping upside yield momentum.

- The 10yr, just under 4.49%, remains fairly close to the mid-point of recent ranges.

- Looking ahead, we have wholesale inventories tonight, then tomorrow NFIP small business sentiment and NY Fed inflation expectations. The main focus will be on Wednesday's CPI print though.